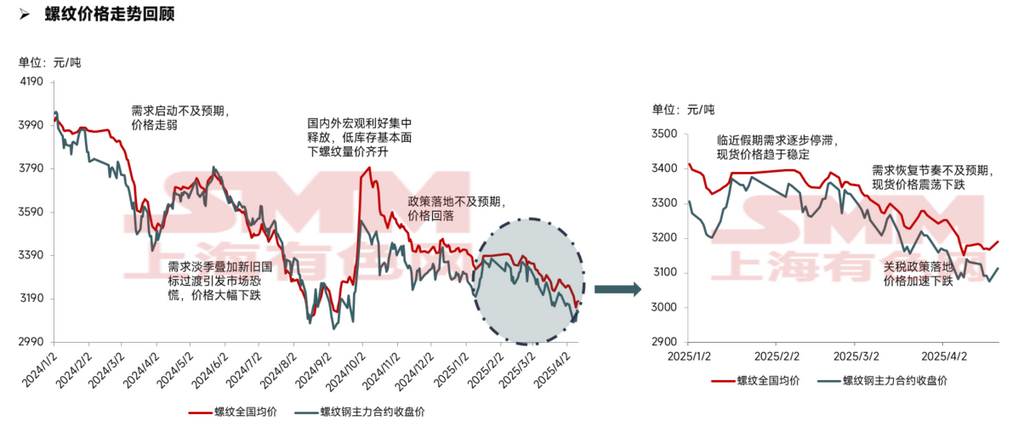

Rebar spot prices first fell and then stabilized in April, with the price center continuing to decline compared to 2024.

The annual average price of rebar spot in 2024 was 3,575 yuan/mt, while the average price from January to April 2025 was 3,310 yuan/mt, with the price center down by 265 yuan/mt.

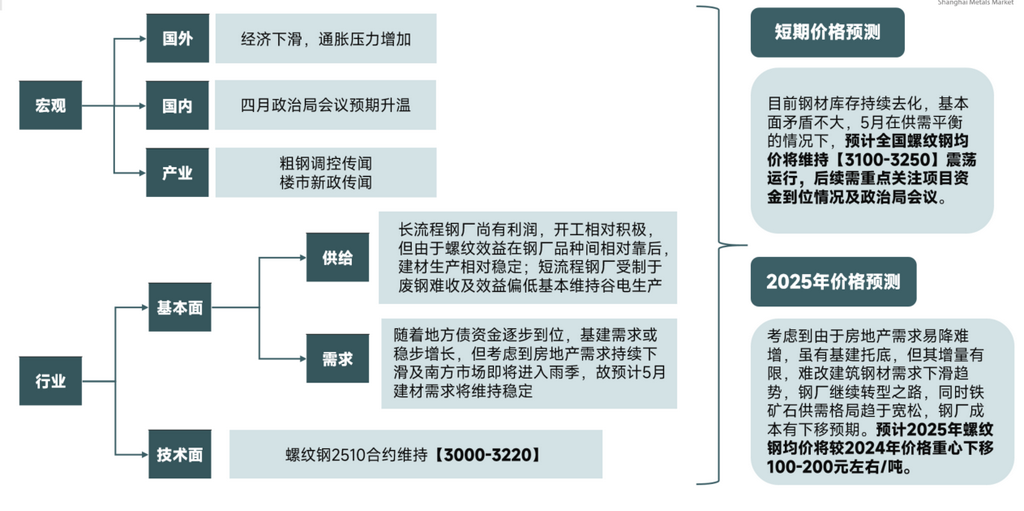

Tariff disputes and heightened macroeconomic uncertainties warrant close attention to the statements from the April Politburo meeting.

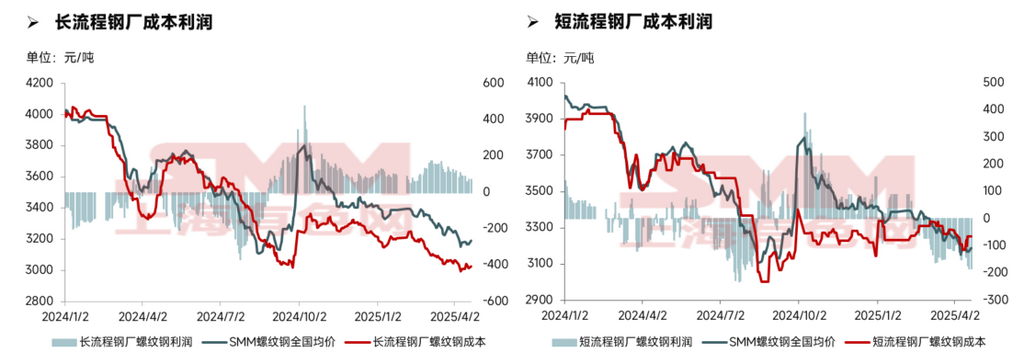

Steel mill profits narrowed, with raw material prices providing cost support.

In April, the average cost of blast furnace steel mills was 3,029 yuan/mt, down 47 yuan/mt MoM from March, with a smaller decline than the monthly average price of rebar, leading to a slight narrowing of steel mill profits. Looking ahead, pre-holiday restocking demand for iron ore provides solid support, and the first round of coke price increases has been implemented, with expectations of a second round, offering some cost support for rebar.

In April, the average cost of EAF steel mills was 3,231 yuan/mt, down 72 yuan/mt MoM from March, with steel mills continuing to incur losses. Going forward, EAF steel mills face difficulties in sourcing steel scrap, making costs more likely to rise than fall, and the extent of losses for EAF steel mills may further expand.

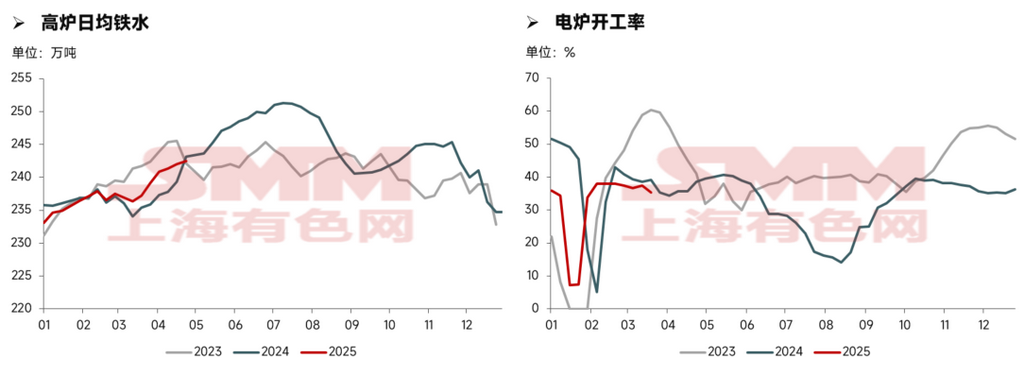

Driven by profitability, the operating rates of BF and EAF steel mills diverged significantly, with subsequent production likely to remain stable.

BF steel mills saw a slight decline in profitability but still maintained profits of 60-100 yuan/mt. Driven by profit motives, steel mills have little intention to cut production, and as previously idled blast furnaces gradually resume production as planned, pig iron production still has room for a slight increase.

EAF steel mills are mostly at break-even, with some mills incurring losses of 50-100 yuan/mt, leading to reduced operating hours. However, looking ahead, EAF steel mills, considering factors such as protecting market share, have no expectations of further production cuts or shutdowns, so EAF operating rates are expected to remain stable.

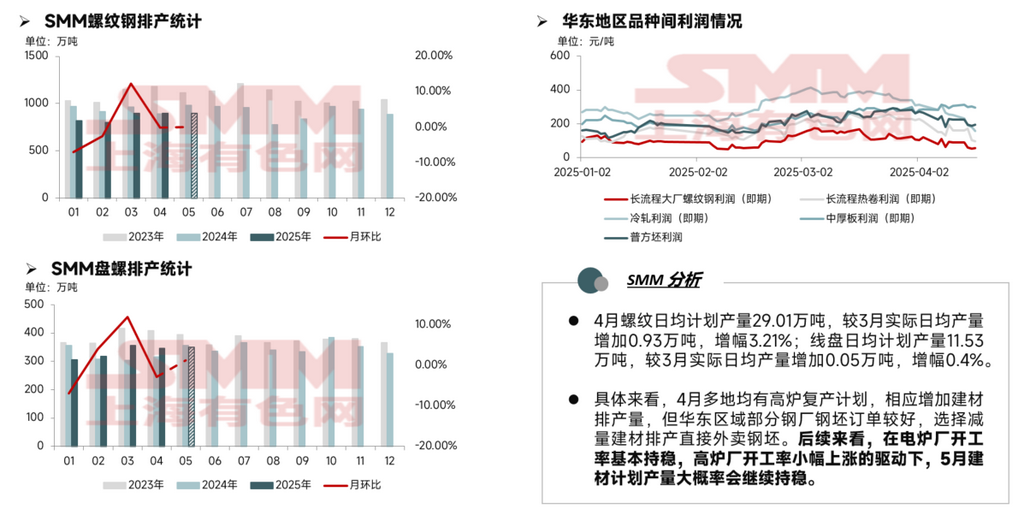

Daily planned production of construction steel increased slightly in April and is likely to remain stable in May.

In April, the daily planned production of rebar was 290,100 mt, up 9,300 mt or 3.21% from the actual daily production in March; the daily planned production of wire rod was 115,300 mt, up 500 mt or 0.4% from the actual daily production in March.

Specifically, many regions had plans to resume blast furnace operations in April, increasing construction steel production. However, some steel mills in east China had strong billet orders and chose to reduce construction steel production and sell billets directly. Looking ahead, with EAF operating rates basically stable and BF operating rates slightly increasing, construction steel production in May is likely to remain stable.

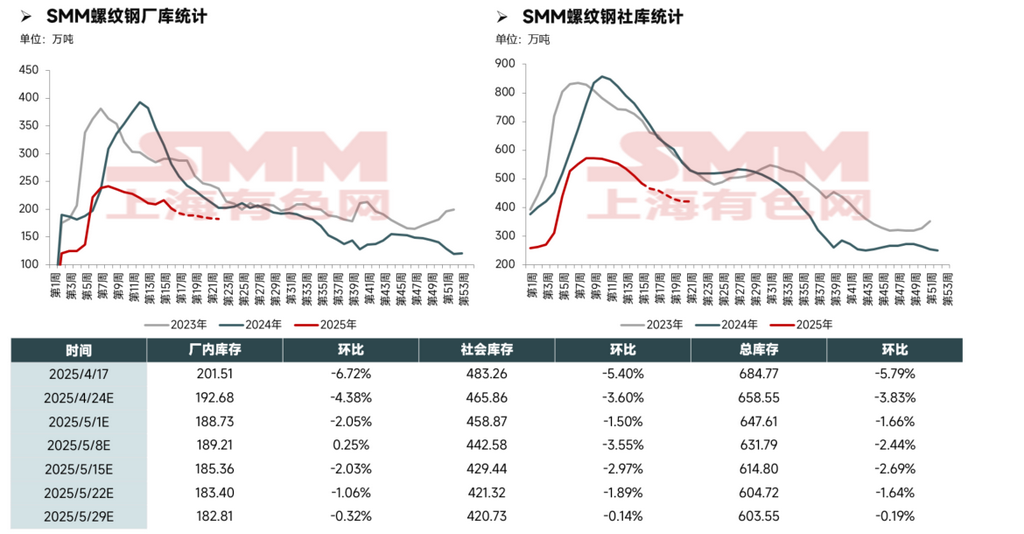

Inventories are at historically low levels, with destocking performance relatively healthy.

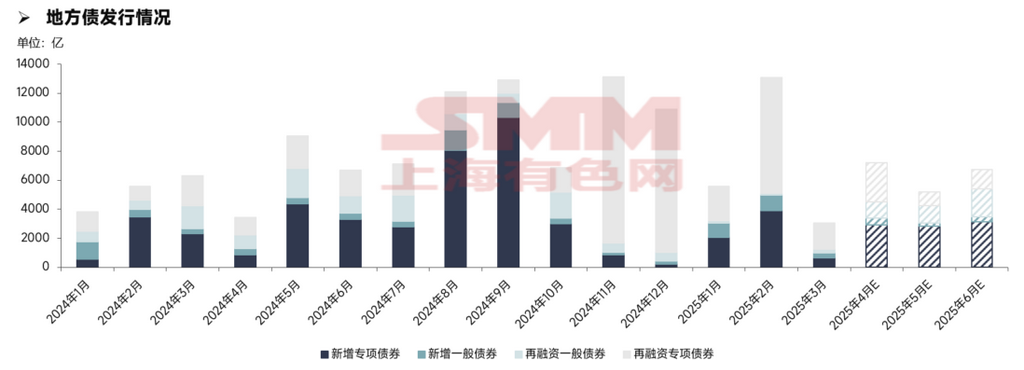

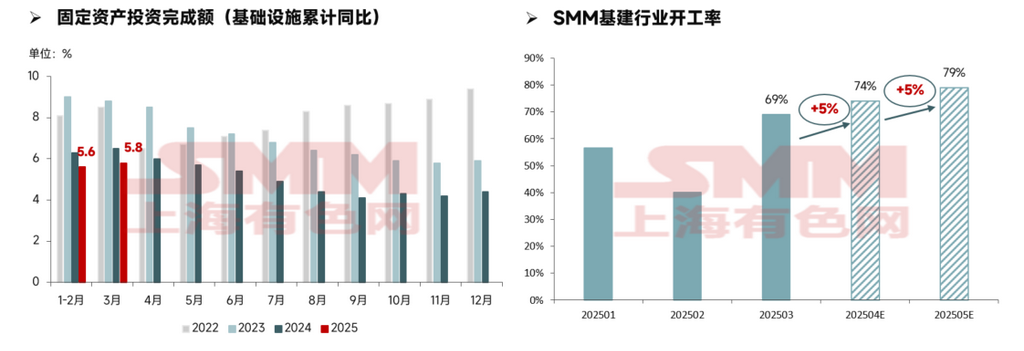

Infrastructure investment growth slowed, and industry operating rates may steadily rise after funding pressures ease.

Infrastructure investment growth has slowed significantly compared to previous years, partly due to the decline in the real estate market weakening land sales revenue and reducing local government financial support. Additionally, local governments face heavy debt pressures, with some provinces and cities being required to suspend new project starts. Overall, downstream operations are significantly constrained by funding conditions.

According to the SMM survey, the infrastructure industry operating rate was 68.9% in March 2025. As the operating conditions in northern inland provinces continue to improve, the industry operating rate has risen significantly. However, the industry still faces extended payment cycles and funding pressure, and subsequent attention should focus on the availability of special bond funds.

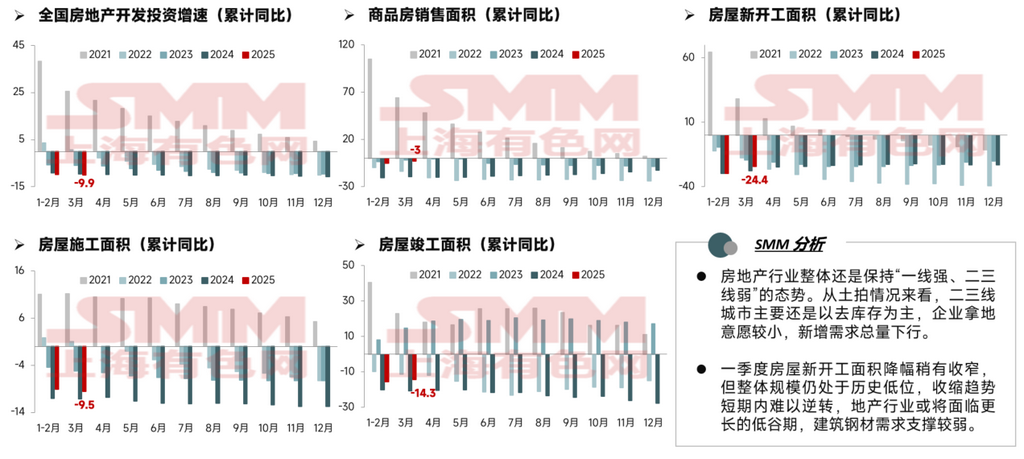

The decline in new housing starts narrowed but remains at an absolute low, and the industry downturn is difficult to reverse in the short term.

The real estate industry overall maintains a trend of "strong in first-tier cities, weak in second- and third-tier cities." From land auctions, second- and third-tier cities are mainly focused on destocking, with companies showing little willingness to acquire land, leading to a decline in total new demand.

The decline in new housing starts narrowed slightly in Q1, but the overall scale remains at a historical low, and the contraction trend is difficult to reverse in the short term. The real estate industry may face a prolonged trough, with weak demand support for construction steel.

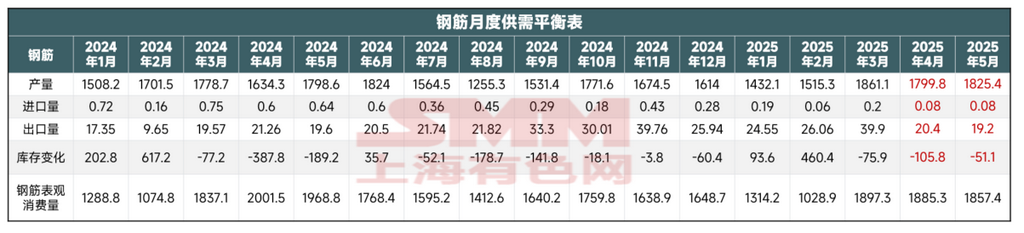

Supply-demand balance table: Weak supply-demand balance for the year.

Q1 2025: During the Chinese New Year, market demand gradually declined to a halt and restarted after the holiday. This year’s Chinese New Year was earlier than usual, and post-holiday weather in the north remained cold, leading to a relatively slow resumption of work and production. Overall demand release fell short of expectations, and steel mill production in Q1 remained relatively low. Additionally, winter stockpiling this year was limited, and inventories continued to decline in March.

Q2 2025: Steel mill production in April saw little change, demand continued to recover, and inventories continued to decline. Looking ahead, as local government bonds gradually become available, downstream funding pressures will ease, and infrastructure demand will see a slight increase. However, considering the continued decline in real estate demand and the upcoming rainy season in south China, rebar demand in May is expected to remain stable.

Price forecast: Supply-demand balance, with no prominent fundamental contradictions, and construction steel prices may maintain a sideways movement in May.

Currently, steel inventories continue to decline, and fundamental contradictions are not significant. In May, under a supply-demand balance, the nationwide average price of rebar is expected to fluctuate within the range of 3,100-3,250 yuan/mt. Subsequent attention should focus on project funding availability and the Politburo meeting.

With low inventories and improved market sentiment, the market will still face demand challenges under high pig iron production, and short-term steel prices are expected to fluctuate. As the weather gradually warms, demand recovery will accelerate, and April prices are expected to fluctuate around demand intensity. Subsequent attention should focus on project funding availability, with the SMM nationwide average price of rebar expected to fluctuate within the range of 3,150-3,450 yuan/mt in April.

With low inventories and improved market sentiment, the market will still face demand challenges under high pig iron production, and short-term steel prices are expected to fluctuate. As the weather gradually warms, demand recovery will accelerate, and April prices are expected to fluctuate around demand intensity. Subsequent attention should focus on project funding availability, with the SMM nationwide average price of rebar expected to fluctuate within the range of 3,150-3,450 yuan/mt in April.

![Before the holiday, the black chain is unlikely to see a trend-driven market [SMM Steel Industry Chain Weekly Report].](https://imgqn.smm.cn/usercenter/zUFfM20251217171748.jpg)

![[SMM Chromium Daily Review] Inquiries and Transactions Weakened, Chromium Market Showed Mediocre Performance Before the Holiday](https://imgqn.smm.cn/usercenter/ENDOs20251217171718.jpg)