SMM April 24 News,

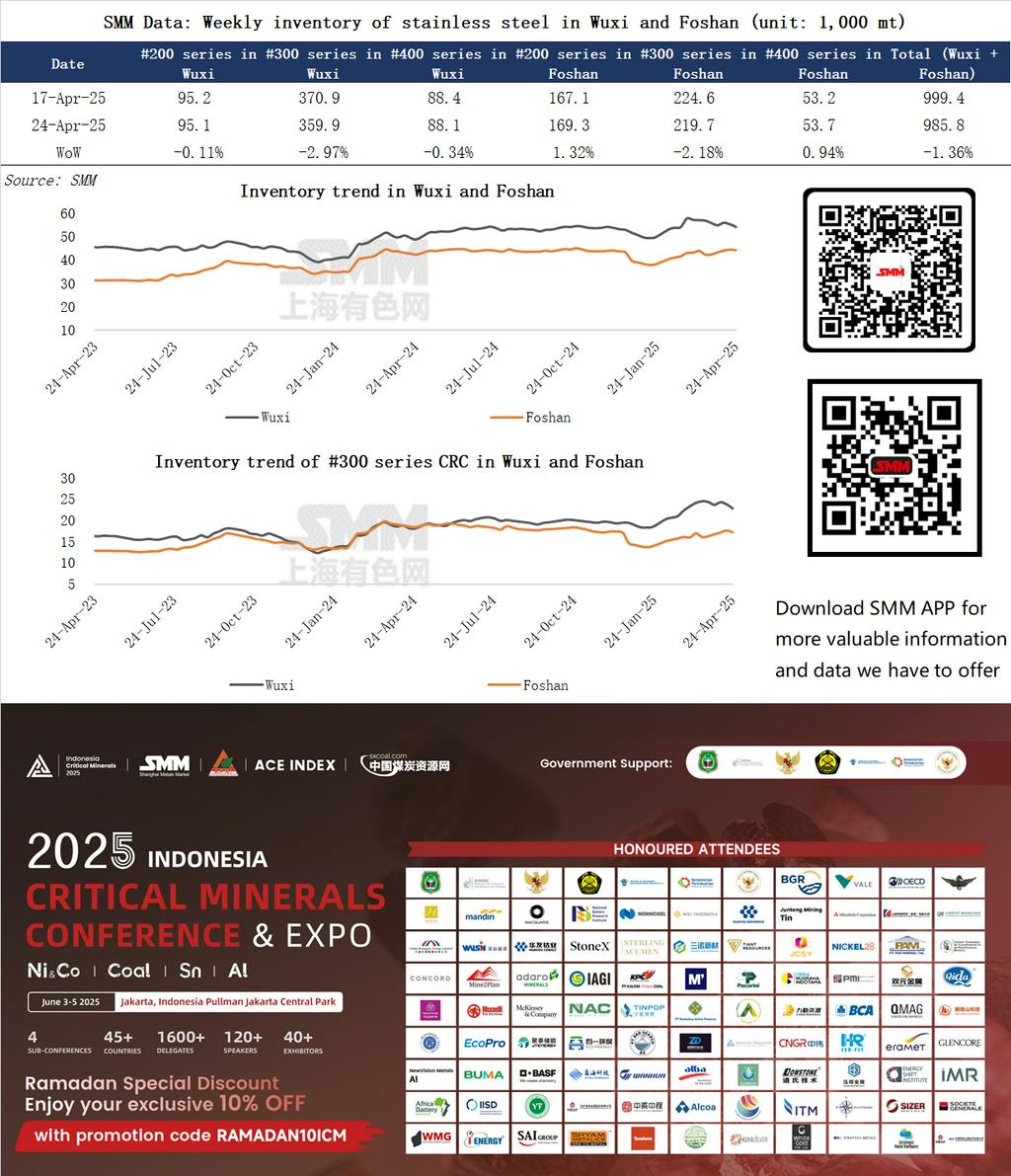

This week (April 18-24, 2025), the total stainless steel inventory in the two major markets of Wuxi and Foshan showed a destocking trend, decreasing from 999,400 mt on April 17, 2025 to 985,800 mt on April 24, down 1.36% WoW. Demand side: The market demand remained relatively stable, with downstream enterprises maintaining a certain cargo pick-up pace.

Supply side: Stainless steel mills actively urged agents and traders to pick up goods, but due to high inventory levels previously maintained by agents and traders, they faced significant warehousing and financial turnover pressures, leading to low enthusiasm for picking up goods, which kept arrivals at normal levels. Stainless steel mills hoped to accelerate shipments, while agents and traders were cautious about picking up goods due to their own business conditions.

In Wuxi, all grades saw a destocking trend, with 300-series inventory notably decreasing by 2.97%, mainly because large de-stocking volumes of nearly 20,000 mt occurred at delivery warehouses such as CMST and Minmetals, related to concentrated cargo pick-ups or delivery demands from some enterprises. 400-series inventory also slightly decreased, down 0.34% WoW; 200-series inventory changes were relatively small, down 0.11% WoW, basically maintaining a relative supply-demand balance.

In Foshan, 200-series and 400-series inventories increased 0.94% and 1.32% WoW, respectively, due to increased arrivals and slow cargo pick-ups by downstream entities; 300-series inventory, however, decreased by 2.18%, with significant de-stocking at delivery warehouses. The increase in 200-series and 400-series inventories was mainly due to recent increases in arrivals, while downstream cargo pick-ups were slow. On one hand, some steel mills increased shipments to the Foshan market, hoping to expand market share; on the other hand, some small and medium-sized enterprises downstream, facing financial constraints and concerns about future market price trends, adopted a conservative procurement strategy, picking up goods as needed, leading to inventory accumulation. The 300-series inventory decreased by 2.18%, with significant de-stocking at delivery warehouses, possibly due to local large processing enterprises meeting order demands by concentrating on picking up goods from delivery warehouses.

SMM analysis suggests that the current market inventory is in a destocking state, which to some extent accelerates the capital recovery of traders. However, due to intense competition in the stainless steel market and frequent price fluctuations, the profit margin for traders is limited. With the Labour Day holiday approaching, some downstream enterprises may moderately restock to meet production needs during the holiday. However, exports of downstream and end-use products face uncertainties in overseas market demand and trade barriers, and domestic demand is affected by macroeconomic conditions and the real estate market, making the situation still not optimistic. Additionally, as May approaches, the industry will enter the off-season, potentially reducing overall market activity, all of which will impact the subsequent destocking speed.

It is expected that next week, stainless steel inventories in the Wuxi and Foshan markets will remain stable with minor fluctuations. On the demand side, pre-holiday restocking demand may see some release, but it is unlikely to experience explosive growth; on the supply side, stainless steel mills may adjust shipment pace and production based on current market inventory and demand, ensuring that inventory does not change significantly.

If you have any questions regarding stainless steel inventory, please feel free to contact us: Chaoxing Yang at 13585549799 (WeChat ID is the same).

》Click to View SMM Stainless Steel Spot Historical Prices