April 24, the CCIE-2025SMM (20th) Copper Industry Conference and Copper Industry Expo, hosted by SMM Information & Technology Co., Ltd., SMM Metal Trading Center, and Shandong Aisi Information Technology Co., Ltd., with Jiangxi Copper Corporation and Yingtan Luhang Holding Co., Ltd. as the main sponsors, and Shandong Humon Smelting Co., Ltd. as a special co-organizer, and Xinhuang Group and Zhongtiaoshan Nonferrous Metals Group Co., Ltd. as co-organizers, successfully concluded in Nanchang, Jiangxi! This conference included multiple forums such as the Wulatezhong Banner Investment Promotion Conference, Electrical Power Transmission and Distribution Industry Forum, Copper Pipe and Rod Processing Industry Development Forum, Copper Industry Financial Innovation Forum, Main Forum, Guixi City Investment Promotion Conference, Copper Industry Low-Carbon Energy Transition Forum, Secondary Copper Industry Green Development Forum, and High-Quality Development of Copper-Based New Materials Forum, comprehensively analyzing the entire copper industry chain ecosystem from upstream copper ore mining, to midstream smelting and processing, to downstream end-use applications and market demand. The conference gathered government officials, copper industry leaders, academic elites, and representatives of industry organizations from around the world. Guests discussed hot topics in the copper industry chain, including 76 years of hard work and progress in China's copper industry, development trends of copper-based materials for motor and transformer windings, reflections on the development of China's wire and cable industry, development trends of copper alloy materials for connectors, global macroeconomic changes and outlook for commodity allocation, practical innovations and pain points in the copper industry's financial integration, analysis of the consumption status of secondary copper in China, the impact of the current state of the photovoltaic industry on the photovoltaic cable market, building a service ecosystem for the copper industry to address industry needs, trading strategies for the current landscape of China's copper industry, 2025 copper price trends and outlook, opportunities and challenges for copper alloy materials in HVAC, plumbing, and refrigeration industries, the current situation and high-quality development trends of China's copper processing industry, the current situation and trends of new energy vehicles, how to better promote the quality development of the secondary copper industry—supply and consumption, scrap-produced copper anode becoming a key supplement to copper smelting raw materials under the backdrop of copper ore shortage, and the green and low-carbon breakthroughs in the non-ferrous metals industry driven by PV ESS.

Wang Jianlong, Deputy Director of Metallurgy Department One at China ENFI Engineering & Technology Co., Ltd., pointed out when discussing the global copper smelting landscape and intelligent development: The world's proven copper reserves are about 1 billion mt, and based on copper mine production, the static assurance period is approximately 45 years. The top five countries in terms of copper resource reserves are Chile, Peru, Australia, Russia, and DRC, accounting for about 57% of the total. As the world's largest consumer and producer of refined copper, China does not have a significant advantage in copper ore resources and needs to import large amounts of copper concentrates. In 2024, China's imports of copper concentrates will reach 28.11 million mt. To address the current state of the copper smelting industry, relevant national departments are promoting the healthy and orderly development of the copper smelting industry through industrial policies, environmental protection policies, and other measures; overall, they are deepening supply-side structural reforms, strictly controlling the disorderly expansion of copper smelting capacity, and accelerating intelligent and green transformations on the supply side, while guiding enterprises to accelerate technological progress, overcome the shortcomings of copper-based new materials, and fully tap into the application potential of copper in new infrastructure and construction projects on the consumption side.

Zhou Mingliang, Executive Director of the Advanced Basic Materials Application Research Center at the Shenzhen Connector Industry Association, stated: The rapid development of digital infrastructure such as 5G communications and data centers has significantly increased the demand for connectors, especially those that can meet the requirements of high-speed data transmission and strict signal integrity. It is expected that the global connector market size will reach $100 billion by 2025, with digital infrastructure being one of the main application areas, accounting for about 30%. In his forecast of the application of copper alloys in connectors, he said: Automotive sector: By 2025, the application of copper alloy materials in the automotive sector in China is expected to reach about 500,000 mt, and with the expansion of the NEV market, the application of copper alloy materials will continue to grow; Digital infrastructure: The application of copper alloy materials in the digital infrastructure sector is expected to reach about 1 million mt, and the application of copper alloy materials in this sector will continue to expand; Consumer electronics: The application of copper alloy materials in the consumer electronics industry is expected to remain stable at about 600,000 mt, and copper alloy materials will continue to play a crucial role in this sector.

Long Huachen, Senior Copper Analyst at SMM, mentioned in the analysis of the 2025 copper wire rod market: From 2019-2025, China's refined copper rod capacity increased from 11.5 million mt to 17.67 million mt, with an average annual compound growth rate of 6.41%; production increased from 7.18 million mt to 10.3 million mt, with an average annual compound growth rate of 4.66%. With the commissioning of new refined copper rod capacities, the continuous release of new capacities, and the more pronounced overcapacity in the industry. By the end of 2025, the capacity is expected to reach 17.67 million mt/year, and there are still plans for further additions. In the outlook for 2025, he stated: The acceleration of power grid investment and the steady growth in the use of copper rods in the new energy industry. Electrolytic copper rod exports need to find a way out, and attention should be paid to whether the high growth in copper rod exports in 2024 can be sustained after the cancellation of export tax rebates. With tight supplies of copper concentrates and increased demand for anode plates, it is expected that more secondary copper rod enterprises will shift to producing anode plates.

Zhang Junbing, Minister of Secondary Copper Operations at Zhejiang Hailiang, spoke about the future challenges and opportunities for secondary copper, stating: Growth is led by new energy and high-end manufacturing, but resource constraints and capacity bottlenecks still exist; it is estimated that the global apparent consumption of refined copper in 2025 will be 28.5 million mt, and the global copper deficit in 2025 is expected to be 180,000-500,000 mt, with a global copper supply deficit of 10 million mt over the next decade. The future development of secondary copper will face challenges such as geopolitical and trade policies, the penetration rate of alternative technologies (advancements in aluminum as a substitute for copper), and technical bottlenecks in recycling technology. Enterprises can adopt strategies such as a diversified supply system of "mining + secondary + overseas," focusing on high-value-added products and low-carbon transformation, using policy hedging and financial tools, and driving both emerging fields and regional markets.

Yu Shaohua, Senior Manager of SMM Research, expects: The growth rate of global lithium battery copper foil production will slow down significantly. With the continuous development of NEVs, ESS, and portable electronic devices, the scale of lithium battery copper foil will still grow, and the capacity utilization rate will continue to increase. When introducing the development trends of global electronic circuit copper foil from 2025-2030, she noted: With the continuous development and technological advancements in the communication, automotive, and AI industries, the global CCL sales market has certain growth potential. In the future, high-value-added products will grow faster, such as the upgrade of AI servers and switches, which will drive the demand for high-speed CCL, and the rise of AIPC and AI phones will also promote the development of special substrate CCL. By 2030, driven by IDC construction, data communication, consumer electronics, and NEVs, the global electronic circuit copper foil production is expected to reach 950,000 mt. In the future, the pace of domestic substitution for high-end electronic circuit copper foils is accelerating. SMM expects that after 2027, the global surplus of electronic circuit copper foils will slow down significantly. The Chinese market, supported by strong policies, will maintain a stable recovery, and emerging markets such as Southeast Asia have significant growth potential.

Click to replay the live video of this summit

Click to view the photo live stream of this summit

Click to view the special report of this summit

Opening Remarks

Xia Hanjun, Deputy General Manager of Jiangxi Copper Corporation

Click to view the details of the remarks

Li Haidong, Member of the Standing Committee of Guixi Municipal Party Committee, Director of Guixi Economic and Technological Development Zone

Click to view the details of the remarks

Zhang Ming, Deputy General Manager of Shanghai Futures Exchange

Click to view the details of the remarks

Liang Zhuge, CEO of SMM

Click to view the details of the remarks

Awards

2024 Outstanding Service Providers for Green Transformation in the Non-Ferrous Metals Industry

Click to view the award details

Top 10 Outstanding Suppliers of SMM Copper Rod Processing Enterprises in 2025

Click to view the award details

Top 10 Outstanding Suppliers of SMM Copper Busbar Processing Enterprises in 2025

Click to view the award details

Guest Speakers

April 22

Electrical Power Transmission and Distribution Industry Forum

Topic: Development Trends of Copper-Based Materials for Motor and Transformer Windings

Speaker: Liang Dong, Chief Representative, Beijing Office of the International Copper Association, Head of the Low-Carbon Drive Project, Senior Engineer

Introduction to Copper Applications in Electric Motors and Transformers

Classification and Application Areas of Wire and Cable Products

Application Areas of Winding Wires

Research Trends of Copper Alloy Winding Wires

High-Performance Conductors: Low-Oxygen Content Conductors, High Flexibility, High Strength, and High Conductivity

Copper Applications in Electric Motors and Transformers

He cited examples of copper applications in electric motors and transformers.

Development Trends of Electric Motors and Transformers

Global Low-Carbon Development Trends

• EU: Reduce greenhouse gas emissions by 55% compared to 1990 levels by 2030, achieve carbon neutrality by 2050

• Japan: Achieve carbon neutrality by 2050

• UK: Achieve net-zero emissions by 2045, carbon neutrality by 2050

• Canada: Achieve carbon neutrality by 2050

• China: Peak carbon emissions by 2030, achieve carbon neutrality by 2060

• As of September 2023, more than 150 countries have committed to carbon neutrality, covering over 80% of global CO2 emissions, GDP, and population.

The process of peaking carbon emissions and achieving carbon neutrality is a process of electrification and re-electrification across society

Re-electrification requires further improvement in energy efficiency on the demand side

The process of peaking carbon emissions and achieving carbon neutrality is a process of electrification and re-electrification across society; electrification refers to the transition of equipment or systems driven by traditional energy sources (such as coal, oil) to electricity-driven; re-electrification further optimizes this, such as using renewable energy for power generation or improving the efficiency of the power system.

Efficiency of Different Drive Systems

The estimated thermal efficiency of steam engines in 1840 was about 3%, and later condensing steam engines reached 8%, with the highest thermal efficiency of steam engines not exceeding 20%.

⇒

The thermal efficiency of gasoline engines in passenger cars is generally below 40%, while diesel engines can reach 40-46%.

Electric drive systems have the highest efficiency, generally above 90%, and can exceed 95%.

Expert Sharing: Development Trends of Copper-Based Materials for Motor and Transformer Windings [SMM Copper Industry Conference]

Topic: Outlook for the Development of New Power Systems in 2025

Speaker: Expert and Director in the Field of New Energy and Dual Carbon at Jilin Electric Power Research Institute Co., Ltd.

Topic: Reflections on the Development of China's Wire and Cable Industry

Speaker: Wu Changshun, Vice President and Secretary-General of the Wire and Cable Branch of the China Inspection and Testing Society

Topic: Green Upgrading of the Electromagnetic Wire Industry in the Context of the New Energy Market

Speaker: Lin Xiyun, Chief Engineer of Xiadeng Gaoke Electrical Co., Ltd.

Topic: Impact of the Current State of the Photovoltaic Industry on the Photovoltaic Cable Market

Speaker: Chang Wenping, Dean of the Cable Engineering College at Henan Institute of Technology

Topic: Building a Service Ecosystem for the Copper Industry to Address Industry Needs

Speaker: Dong Junhao, General Manager of the Market Development Department at Jiangxi Tongdu Digital Services Co., Ltd.

1.2 Pain Points in the Secondary Copper Industry

Large Price Fluctuations: Price risk, supply-demand mismatch, diverse demand, tariffs, trade wars;

Capital-Intensive: High value, high demand, difficult financing, high costs;

Direct Hedging Tools: Default risk, hedging needs, buying spot, regular futures;

Third-Party Platforms: Public-like attributes, credit endorsement, fund supervision, risk control systems.Solutions - Digitalization is the Trend! Commodity Trading Platforms are the Cure!

Building a Copper Industry Service Ecosystem

2.1 Building a Copper Industry Service Ecosystem

Thinking about it, there are problems; doing it, there are solutions! — Establishing a global copper industry digital and intelligent service platform with significant influence by building a world copper capital recycled copper trading service center in Guixi and creating a copper industry service ecosystem.

2.2 Building a Copper Industry Service Ecosystem

2.3 Copper Industry Service Ecosystem

►Copper Industry Service Ecosystem

1. Trading Services: Capacity pre-sales, listed trading, bidding trading models, etc.

2. Supply Chain Financial Services: Relying on the trading platform, upstream and downstream of the industry, domestic and international warehouses, and financial institutions to build a commodity trading ecosystem, providing supply chain financial services.

3. Matchmaking Trading: The trading platform connects upstream and downstream enterprises' supply and demand, leveraging regional, team, and platform advantages to establish efficient and extensive buying and selling information matching and matchmaking. At the same time, it provides services in supply chain finance, overseas warehousing, and customs clearance.

4. Business Services: Providing agency registration, bookkeeping, and tax rebate services for companies needing to register in Hainan.

5. Technology Output: Providing platform technology and operational support for local governments and enterprises.

III. Introduction to the Copper Industry Service Ecosystem Business

3.1 Business Introduction - Capacity Pre-Sales

●Traders certified by Haishang Exchange actively list prices and quantities to sell or buy future delivery spot or contracts through the trading platform; other trading members can choose to buy or sell commodities, with options for early agreement delivery, contract transfer at any time, and delivery upon expiration.

●Broadening sales and procurement channels for enterprises; deposit transactions reduce credit default risks; flexible delivery, with both spot and forward-month transactions; supply chain finance empowerment.

3.1-1 Business Introduction - Capacity Pre-Sales

►Thirteen Delivery Brands

Based on the characteristics of the industry and the convenience of delivery brands being close to upstream and downstream clusters, brass billet varieties are mainly in Zhejiang, with six delivery enterprises; low-oxygen copper rod delivery enterprises total seven, covering North China, Southwest, East China, and Central South, which are the main copper rod processing areas.

》Building a Copper Industry Service Ecosystem to Address Industry Pain Points - Introduction to the World Copper Capital Recycled Copper Trading Service Center

Presentation Topic: 2025 Copper Rod Market Analysis and Outlook

Guest Speaker: SMM Senior Copper Analyst Li Huachen

Chapter 1: 2025 Electrolytic Copper Rod Market Analysis

1.1 SMM Electrolytic Copper Rod Equipment Capacity Distribution Map

SMM Forecast: In 2025, China's electrolytic copper rod equipment capacity will be approximately 17.67 million mt.

East China and South China are both major consumption and production areas, with East China accounting for 50.8% of national copper rod capacity, and Jiangsu region alone accounting for 28% of the national capacity.

1.2 New and Expanded Capacities Continuously Released from 2023 to 2025, Electrolytic Copper Rod Production Growth Slows

►SMM Analysis:

•From 2019 to 2025, China's electrolytic copper rod capacity increased from 11.5 million mt to 17.67 million mt, with an annual compound growth rate of 6.41%; production increased from 7.18 million mt to 10.3 million mt, with an annual compound growth rate of 4.66%.

•With the commissioning of new electrolytic copper rod capacities, the continuous release of additional capacities has made the overcapacity situation more pronounced. By the end of 2025, the capacity is expected to reach 17.67 million mt/year, with further expansion plans still in place.

1.3 Overcapacity Puts Pressure on Copper Rod Processing Fees & Weak Consumption, Electrolytic Copper Rod Operating Rates Often Fall Short of Expectations

►SMM Analysis:

•The long-term overcapacity in the copper rod industry has put pressure on processing fees. In 2024, as copper prices surged, processing fees were significantly impacted, even turning negative under the pressure of premiums and discounts. After copper prices pulled back from highs, they gradually returned to normal levels.

Chapter 2: 2025 Recycled Copper Rod Market Analysis

2.1 SMM Recycled Copper Rod Equipment Capacity Distribution Map

SMM Forecast: In 2025, China's recycled copper rod equipment capacity will be approximately 6.77 million mt, down from 8.07 million mt in 2024, with effective capacity at 4.89 million mt, down from 5.54 million mt in 2024.

》2025 Copper Rod Market Analysis and Outlook [SMM Copper Conference]

Copper Pipe and Bar Processing Industry Development Forum

Presentation Topic: Development Trends of Copper Alloy Materials for Connectors

Guest Speaker: Zhou Mingliang, Executive Director of the Advanced Basic Materials Application Research Center, Shenzhen Connector Industry Association

Main Applications of Connectors in Various Terminals

Explosive Growth in AI Computing Power Demand

Continuous Expansion of AI Application Scenarios: As AI technology advances, more fields such as autonomous driving, medical imaging, and smart manufacturing are adopting AI, all of which require strong AI computing power.

Increased Complexity of AI Models: To improve the accuracy and performance of AI models, more complex models need to be trained, leading to a significant increase in AI computing power demand.

Surge in Data Volume: AI applications require handling large amounts of data, and as data volume increases, so does the demand for computing power.

High-Speed, High-Frequency

High-Speed, High-Frequency Becomes the New Trend: With the continuous improvement of data transmission rates, high-speed and high-frequency connectors will become the trend, especially in 5G communications, data centers, and high-speed computing.

Significant Increase in Market Demand: The demand for high-speed, high-frequency connectors is significant, driven by the pursuit of extreme data transmission and stringent signal integrity requirements, making them a key force in digital transformation.

Innovation Drives Development: Innovations in materials science and precision engineering inject strong momentum into high-speed, high-frequency connectors, leading the data transmission era to new heights.

Continued Expansion of Application Fields: From high-tech electronics to healthcare, from smart manufacturing to smart cities, high-speed, high-frequency connectors play a crucial role, deeply integrating and promoting industrial upgrades and transformations.

Technological Innovation Directions in the Server Industry

High-Performance Computing Technology: High-performance computing technology can enhance server computing performance, meet AI computing power demands, and reduce energy consumption, making it a critical technological development direction for the server industry.

Customization and Modular Design: To meet the diverse needs of different sectors, customization and modular design will become important trends in the server industry, enhancing flexibility and scalability.

Enhanced Security and Reliability: With the widespread adoption of cloud computing and big data, the security and reliability of servers have become increasingly prominent, and the server industry will focus more on improving these aspects.

Digital Infrastructure

5G Communications and Data Centers: The rapid development of 5G communications and data centers, as part of digital infrastructure, has significantly increased the demand for connectors, especially those that can meet the requirements of high-speed data transmission and strict signal integrity.

Connector Market Demand: The global connector market size is expected to reach $100 billion in 2025, with digital infrastructure being one of the main application areas, accounting for around 30%.

High-Performance Requirements: As digital infrastructure becomes more complex, connectors face higher demands for high-speed data transmission and signal integrity, requiring low loss, high stability, and good signal integrity to ensure accurate and reliable data transmission.

》Explosive Growth in AI Computing Power Demand, Copper Alloy Usage Predictions in Automotive and Digital Infrastructure [SMM Copper Conference]

Presentation Topic: Opportunities and Challenges of Copper Alloy Materials in HVAC, Sanitary, and Refrigeration Industries

Guest Speaker: Zhang Guodong, Sales General Manager, Jiangxi Oudi Copper Co., Ltd.

I. Current Application Status

Household HVAC systems, dual-supply systems,

(1) Water Heating and Sanitary Industry

(2) Refrigeration Industry

1. Key Role in Air Conditioning: Mainly used in air conditioner evaporators, condensers, compressor coils, piping, functional valves, and accessories.

2. Wide Application in Refrigerators: Mainly used in evaporators, condensers, compressor coils, piping, and fittings.

3. Relatively Stable Market Demand: For example, in 2024, the global production of household air conditioners will be 200 million units, with a very large ownership base. The replacement cycle for air conditioners is generally 10-15 years, continuously cycling.

II. Application Development Trends

(1) Technological Innovation Promotes Performance Improvement

Optimization of Alloy Composition and Process: By optimizing alloy composition and processing techniques.

Breakthroughs in Nanotechnology Application: Applying nanocoatings on copper material surfaces to enhance the strength, antibacterial, and self-cleaning properties of sanitary products, meeting consumer health needs.

Technological Innovation Boosts Industry Upgrading: Technological innovation drives continuous upgrading of copper and copper alloy material producers, enhancing their market competitiveness.

(2) Health and Green Environmental Protection Become Development Directions

1. Optimization of Production Processes

Enterprises continuously optimize production processes, reducing energy consumption and pollutant emissions, improving quality and efficiency.

2. Enhancing Internal and External Circulation Utilization

Enterprises internally recycle water, residual heat, and waste materials, improving secondary recycling technology for secondary copper, effectively reducing costs.

3. Health and Green Development Drive Industry Transformation

Health is the most important, and energy conservation and emission reduction are the directions.

(3) Customization Needs Promote Product Diversification

Customization in the Sanitary Industry: With the continuous improvement of living standards and production processes, personalized, intelligent, and modular customized products are becoming a trend.

Customization in the Refrigeration Industry: For different usage scenarios and customer needs, various customized non-standard products have emerged in the refrigeration industry, meeting requirements, reducing waste, and saving energy.

Customization Drives Market Expansion: Customized products meet the diverse needs of consumers and customers, helping enterprises expand market share and increase product market share.

III. Development Trends of Substitute Materials

(1) Rise of Plastic Materials in the Sanitary Industry

It elaborates from the perspectives of cost and processing advantages, performance gaps and application limitations, competitive landscape, and market impact.

(2) Competition of Aluminum Alloy Materials in the Refrigeration Industry

01 Cost and Weight Advantages: Low price and light weight.

02 Insufficient Performance and Application Limitations: Much lower thermal conductivity than copper, limiting its application scenarios.

03 Competitive Landscape and Industry Impact: With rising copper prices, the use of aluminum continues to expand.

(3) Competition of Stainless Steel Materials in the Refrigeration Industry (I)

》Opportunities and Challenges of Copper Alloy Materials in Sanitary and Refrigeration Industries [SMM Copper Conference]

Presentation Topic: Current Status and Improvement Directions of Copper Alloy Tube Production Technology

Guest Speaker: Mo Xingde, General Manager, Guilin Lijia Metal Co., Ltd.

Current Status of Copper Alloy Tube Production Technology

1.1 Copper Alloy Tube Production and Major Application Areas

Alloy tubes, with their high strength, wear resistance, corrosion resistance, good thermal conductivity, and excellent machinability, are used in thermal power, nuclear power, petrochemical, shipbuilding, seawater desalination, and other fields. Brass and white copper cold/heat exchange tubes are used in HVAC, water supply, and other applications. Alloy tubes are also used in decorative items, electrical appliances, mechanical manufacturing, musical instrument manufacturing, and new application areas such as new energy.1.2 Major Producers of Copper Alloy Tubes

It introduced the main producers of copper alloy tubes.

1.3 Production Processes for Copper Alloy Tubes

► Melting and Casting Processes

The main melting processes include medium frequency core induction melting, coreless induction melting, and vacuum induction furnace melting.

The casting processes mainly include vertical semi-continuous casting, vertical continuous casting, horizontal continuous casting, and upward continuous casting.

► Processing Techniques

Production methods include extrusion, planetary rolling, cold rolling, straight drawing, and coil drawing.

1.4 Main Production Equipment for Copper Alloy Tubes

Vertical semi-continuous casting units, horizontal extruders, hydraulic drawing machines, and tube rolling mills.

1.5 Major Challenges in Copper Alloy Tube Production Technology

1. Long production process and low automation; 2. No breakthrough progress in the process flow over the past 20 years; 3. Facing substitution by products such as stainless steel tubes.

Directions for Improving Copper Alloy Tube Production Technology

2.1 Material Innovation and High Performance: With the development of China's aerospace, electronics, communications, new energy, and high-speed rail industries, coupled with the need for domestic material substitution, the demand for copper alloy tubes is continuously growing. This also places higher performance requirements on the materials, accelerating innovation towards high strength, high conductivity, high wear resistance, high corrosion resistance, and environmentally friendly types. Typical representatives include copper-chromium-zirconium, dispersion-strengthened copper alloys, copper-nickel-tin, copper-titanium, copper-iron alloys, bismuth brass, and silicon brass.

2.2 Improvement and Advancement of Short Process Technologies: The "upward continuous casting-cold rolling" and "horizontal continuous casting-planetary rolling" processes without extrusion have their own limitations in alloy tube production. Currently, they are being further improved, perfected, and innovated to be applicable to more grades, representing the development direction for precision copper alloy tube production.

》Current Status and Directions for Improvement in Copper Alloy Tube Production Technology [SMM Copper Industry Conference]

Presentation Topic: Development Trends in the Faucet Industry

Guest Speaker: Lin Jin, Senior Advisor, Bathroom Branch, China Building Sanitation Ceramics Association

As an important part of the manufacturing industry, China's hardware industry has shown new development trends in both domestic and foreign trade in recent years.

Domestic Trade Development Trends

I. Consumption Upgrade Drives Product Structure Optimization

1. Growth in High-End Demand: As domestic manufacturing upgrades and consumer levels rise, the market demand for high-precision tools, smart hardware (such as smart locks, power tools), and eco-friendly materials has significantly increased.

2. Customization and Scenario-Based Solutions: The home hardware sector (such as cabinet hardware, bathroom accessories) is transitioning towards personalized and scenario-based solutions, with leading enterprises capturing the mid-to-high-end market through design innovation.

II. Policy and Infrastructure Boost Demand

1. New Infrastructure and Urbanization: Urban renewal, old community renovation, and 5G base station construction drive the demand for building hardware and engineering tools; the new energy vehicle and PV industries boost the growth of industrial hardware components.

2. "Dual Circulation" Policy Support: National policies encourage expanding domestic demand, and hardware companies are accelerating their layout in lower-tier markets (third- and fourth-tier cities and rural areas) through e-commerce channels.

3. Relevant Government Subsidies: Green manufacturing and energy-saving subsidies (green product certification, energy-saving technology transformation), technological innovation and industrial upgrading subsidies (high-tech enterprise recognition, specialized and innovative "little giant" enterprise support, intelligent manufacturing special subsidies).

III. Deepening Digital Transformation

1. Rise of Online Channels: Platforms like Tmall, JD.com, and Pinduoduo have become important sales channels, with live streaming e-commerce and community marketing helping brands reach consumers.

2. Intelligent Supply Chain: Leading enterprises use IoT and big data to optimize inventory management, achieving flexible production and quick response to market demands.

Foreign Trade Development Trends

I. Changes in Global Market Landscape

1. Tariff Impact: Tariffs have evolved from traditional trade protection tools to key means of major power competition, industrial upgrading, and rule competition. Their impact extends beyond commodity flow, deeply embedded in technology, climate, and geopolitics. Future global market outcomes may depend on how countries find a dynamic balance between openness and protection, efficiency and security, and competition and cooperation.

2. Potential of Emerging Markets: Robust infrastructure demand in Southeast Asia, the Middle East, and Africa has become a new growth point for Chinese hardware exports; the share of trade with countries along the Belt and Road continues to increase.

3. Increased Barriers in European and US Markets: Environmental standards (such as the EU REACH regulation) and anti-dumping investigations force companies to enhance compliance capabilities.

II. Upgrading Export Models

1. Acceleration of Cross-Border E-Commerce: Through platforms like Alibaba International, Amazon, TikTok, Temu, and Shein, Chinese companies connect with overseas B2B and B2C customers, enhancing market penetration.

2. Brand Globalization and Localization: Leading enterprises set up overseas warehouses and after-sales service centers, acquiring local brands or establishing joint ventures to increase market share.

III. Cost and Supply Chain Challenges

1. Pressure of Industrial Relocation: Some low-value-added capacities are shifting to Vietnam and India, pushing domestic companies to transform towards higher value-added segments.

2. Exchange Rate and Raw Material Fluctuations: RMB exchange rate fluctuations and unstable raw material prices, such as steel, test companies' cost control capabilities.

Competitive Strategies of Leading Enterprises

I. Technological Innovation and Green Transition

1. Increase R&D investment to develop intelligent and eco-friendly products (such as brushless motor tools, biodegradable coating hardware).

2. Implement ESG practices through photovoltaic roofs and scrap recycling to address international carbon tariffs (such as the EU CBAM).

II. Industry Chain Integration and Synergy

1. Vertically integrate upstream raw material (such as steel, alloys) supply and horizontally expand into hardware tool supporting services.

2. Collaborate with leading enterprises in home and electronics industries to provide one-stop solutions.

》Development Trends in the Faucet Industry [SMM Copper Industry Conference]

Presentation Topic: Influence of Metallurgical Quality of Brass Ingots and Rods on the Structure and Performance of Bathroom Products

Guest Speaker: Lao Xicai, General Manager, Guangdong Weiqiang Copper Technology Co., Ltd.

01 Influence of Metallurgical Quality on Microstructure

Influence on Microstructure

01 Grain Size and Shape

Grain size directly affects the strength and toughness of the material, while grain shape significantly influences fatigue life. The number and distribution of grain boundaries have a significant impact on material properties.

02 Microscopic Defect Analysis

Casting defects such as shrinkage porosity, gas holes, and inclusions significantly affect the mechanical, processing, and physical properties of the material. Comprehensive control is needed in raw material purity, alloy composition design, refining, and casting crystallization.

03 Uniformity Analysis

Uniform microstructure can improve overall material performance. Non-uniformity can lead to stress concentration and performance degradation, which is crucial for the corrosion resistance of bathroom products.

Grain Size and Shape

► Influence of Grain Size

Large grains have fewer total grain boundary areas, weaker intergranular bonding, and decreased strength and toughness, as well as reduced corrosion and welding performance. Smaller grains offer better mechanical, physical, and processing properties.

► Influence of Grain Shape

Equiaxed crystals: Good isotropy, suitable for deformation processing, achieved by adding modifiers to inhibit columnar crystal growth.

Columnar crystals: Arranged in specific directions, good axial strength but poor transverse plasticity and fatigue resistance, prone to shrinkage, cracks, and other defects.

Grain size and shape influence dislocation movement, grain boundary characteristics, and uniformity, directly determining mechanical, processing, and environmental resistance. Synergistic optimization of composition design (e.g., microalloying) and process control (e.g., rapid solidification, cold working rate, and heat treatment) can control grain structure, improving metallurgical quality.

Phase Composition and Distribution

a+β phase characteristics: α+β phases have good comprehensive properties; α phase, face-centered cubic structure, excellent plasticity, suitable for cold working; β phase, body-centered cubic structure, high hardness, low plasticity, suitable for hot working.

Pb phase characteristics: Pb phases distributed as small particles at grain or phase boundaries act as chip breakers and self-lubricants during machining, reducing tool wear and improving surface finish and efficiency.

Uniform phase composition and distribution significantly affect mechanical, processing, and surface treatment properties. Aggregation of β and Pb phases can cause local stress concentration, reducing strength, corrosion resistance, and fatigue resistance, and affecting the stability of plating adhesion, impacting aesthetics and long-term corrosion resistance.

02 Influence of Metallurgical Quality on Physical Properties

Influence of Brass Ingots and Rods on Bathroom Product Performance

► Influence on Brass Product Microstructure

Density and uniformity: During solidification, if the volume contraction of the high-temperature metal melt is not timely replenished, shrinkage cavities (porosity) will appear in the last solidified area. Inhomogeneous solidification results in coarse columnar or dendritic structures, often with porosity, gas holes, and inclusions, affecting forging, processing, and material properties.

》Influence of Metallurgical Quality of Brass Ingots and Rods on the Structure and Performance of Bathroom Products [SMM Copper Industry Conference]

Presentation Topic: Manufacturing Technology and Application of High-Performance Copper Alloy Rods

Guest Speaker: Xiao Zhu, General Manager, Hunan Gaoke Kewei New Materials Co., Ltd.

Dispersion-Strengthened Copper Alloy Rods

► Introduction to Dispersion-Strengthened Copper

Product Characteristics: High strength and hardness, high-temperature softening resistance up to 980°C, excellent electrical and thermal conductivity, non-magnetic, and anti-adhesion.

► Preparation Methods for Dispersion-Strengthened Copper

► Issues in Dispersion-Strengthened Copper Material Preparation

Excess free oxygen and large alumina particles at grain boundaries are the root causes of hydrogen embrittlement and cracking during cold working. If 100g of copper contains 100ppm of oxygen, it can produce 14cm³ of high-pressure steam at 800°C during hydrogen annealing, causing the copper to rupture.

► Core Technologies and Production Processes for Dispersion-Strengthened Copper

The company uses proprietary technology to effectively control ppm-level free oxygen content and achieve uniform distribution of nano-scale AI2O3 particles, optimizing the process, controlling microstructure, and enhancing overall performance.

► Main Applications of Dispersion-Strengthened Copper in Welding

Ideal material for next-generation electrodes: Nano AI2O3 particles reinforce the copper matrix, providing stable microstructure, high strength, high hardness, high electrical conductivity, and high-temperature softening resistance.Dispersion Copper Applications in Other Fields High-energy combustion chamber radiators, medical device CT machine ball valves, inertial guidance components, high-voltage DC relay contacts, aerospace radar components, high-energy physics experimental apparatus photon absorbers.

Copper-Nickel-Tin Alloy ►Introduction to Copper-Nickel-Tin Products Product characteristics: Amplitude decomposition strengthening type alloy, ultra-high strength and elasticity, excellent wear and corrosion resistance, beryllium-free, non-magnetic, environmentally friendly. ►Technical Challenges Using first-principles and molecular dynamics to optimize alloy composition, preparing ingots through powder metallurgy and continuous casting methods, solving the severe segregation of Sn elements during the alloy ingot preparation process, and breaking through key technologies for high-performance rod production. Key Technology 1: Large-Scale Homogenized Powder Metallurgy Ingot Manufacturing and Rod Control Forming Technology •Key large-size homogenized ingot preparation technology, solving the severe segregation of Sn elements in large-scale ingots; key high-performance rod radial forging and heat treatment technology, solving the problem of precise and efficient product formation. Key Technology 2: Large-Scale Melting and Casting Ingot Homogenization Manufacturing and Combined Deformation Heat Treatment Technology •Through component optimization, crystallizer design, and drawing process control to inhibit reverse segregation, significantly improving the dendritic structure of large-scale ingots, achieving homogenized ingot preparation; key combined deformation heat treatment technology for high-performance rods, achieving controlled forming and overall performance improvement. 》Technology Sharing: High-Performance Copper Alloy Rod Manufacturing Technology and Application [SMM Copper Industry Conference] Presentation Topic: 2025 Copper Billet Supply-Demand Pattern and Development Guest Speaker: SMM Senior Copper Analyst Yutong Huang 01 Insight into 2025: Copper Billet Market Supply Landscape SMM 2024 National Copper Billet Categories, Brass Billet Production Processes, and Representative Enterprises Analysis Brass billets dominate the national copper billet market, with continuous casting processes becoming mainstream in brass billet production in recent years. At the same time, many companies are actively laying out in the continuous casting and extrusion billet fields, highlighting the competitive market situation. ►SMM Analysis Brass billets account for as high as 80% of the national copper billet market, holding an absolute dominant position. Among them, ordinary brass billets (H62, etc.) account for more than 50% of the share, with good mechanical properties, easy processing, and corrosion resistance, widely used in valves, hardware, decorations, etc. Continuous casting billets, using a continuous casting process, have the advantages of high production efficiency and low cost. In 2024, continuous casting billets will account for about 75% of the copper billet market share. A large number of enterprises enter the continuous casting billet market, leading to severe overcapacity, intense competition among enterprises, and gradually decreasing processing fees. Large copper billet factories, with their quantity and technological advantages, occupy most of the market share. The remaining enterprises that produce extrusion billets almost do not produce continuous casting billets, focusing mainly on extrusion billet orders. SMM 2024 National Brass Billet Capacity Regional Distribution and Enterprise Scale Proportion Brass billet capacity is highly concentrated in Zhejiang, Jiangxi, Guangdong, and Anhui. Large enterprises dominate the capacity landscape, with prominent industrial cluster advantages. ►SMM Analysis Reason: Zhejiang and other regions, with their long-term accumulated solid industrial foundation, complete and mature upstream and downstream industry chain supporting systems, form industrial clusters, attracting investment and enterprises. Convenient transportation facilitates raw material procurement and product transportation and sales, being close to consumer markets and responding quickly to customer needs. Outlook: Under industrial upgrading, these regions may increase R&D investment in brass billet production processes and new material applications, moving towards high-end brass billets. They may also promote surrounding development through industrial relocation and regional cooperation. Composition of Brass Billet Raw Materials and Analysis of Secondary Copper Raw Material Imports 40% of secondary brass raw material imports: In 2024, 2.25 million mt of secondary copper (alloy) raw materials were imported, with 15.13% being secondary brass raw materials, totaling 340,400 mt. From January to February 2025, 382,500 mt of secondary copper (alloy) raw materials were cumulatively imported, up 12.86% YoY, with 49,700 mt of secondary brass raw materials imported. In 2025, trade and tariff impacts will change the US supply landscape. ►SMM Analysis In 2025, due to the tense Sino-US trade relations and tariff uncertainties, the US's position as the largest supplier of secondary copper raw materials continues to weaken. In January, the US exported 39,400 mt of copper scrap to China, down 10.32% MoM, accounting for 20.81% of China's total imports. In February, exports to China dropped to 31,400 mt, down 20.35% MoM, with its share declining to 16.22%. In March, exports to China plummeted to 22,500 mt, down 28.34% MoM, with its share significantly dropping to 11.85%, ranking second. From the pie chart of secondary brass raw material import sources, the US accounts for 45%, and its supply reduction will inevitably impact the overall import landscape. On the other hand, the European market, due to high brass return rates and rising prices, sees reduced purchasing willingness from enterprises, making it difficult to maintain stable import volumes. 》SMM Analysis: 2025 Copper Billet Supply-Demand Pattern and Development [SMM Copper Industry Conference] Copper Industry-Finance Innovation Forum Presentation Topic: OTC Derivatives Promote High-Quality Development in the Copper Industry Guest Speaker: Zhan Tu, Head of Marketing and Product Department, Derivatives Business Unit, Jinchuan Futures Co., Ltd. Roundtable Interview: Discussion on Copper Industry-Finance Innovation Practices and Pain Points Moderator: Changyun Fei, Senior Consulting Project Manager, SMM Interview Guests: Zuidie Weng, Party Secretary and Deputy General Manager, Shanghai Port Cloud Warehouse (Shanghai) Storage Management Co., Ltd. Li Zhou, Deputy General Manager, Jiangxi Copper Group Supply Chain Finance Co., Ltd. Gu Peng Niu, General Manager, Commodity Finance Business Division, Shenyang Bank Co., Ltd. Shanghai Branch Xiaolou Yang, Vice President and Director, Shanghai Nonferrous Metals Exchange Co., Ltd. Presentation Topic: Driving Spot and Futures Integration: Ronghang HMS Builds a New Ecosystem of Intelligent Risk Control and Efficient Trading Guest Speaker: Ziyi Wang, Marketing Director, Shanghai Ronghang Information Technology Co., Ltd. Presentation Topic: Shenyang Bank's Commodity Industry Chain Financial Solutions Guest Speaker: Jian Xu, Deputy General Manager, Commodity Finance Business Division, Shenyang Bank Co., Ltd. Shanghai Branch 2. Shenyang Bank's Products Shenyang Bank's commodity industry chain financial products are designed for the trading characteristics of the metal, energy, chemical, and agricultural product industries, creating a full-scenario financing product system. Shenyang Bank uses "cargo flow" as the entry point for risk control and product design, innovating and upgrading traditional trade finance products, and introducing third-party institutions such as futures, insurance, warehousing, and IoT technology service providers to provide professional services, mitigating product risks, lowering customer entry barriers, and enhancing product universality. Existing Product System - Implemented "Cargo Pledge" Financing Products Product Matrix Planning - Complete Industry Chain Financial Product System 3. Product Series - Cloud Warehouse Loan "Cloud Warehouse Loan" refers to short-term financing credit business where applicants use legally held or intended-to-purchase commodities stored in warehouses under the Shanghai International Port (Group) Logistics Co., Ltd. as collateral, and establish a sell hedging position of the same type and quantity at Jianxin Futures Co., Ltd. "Cloud Warehouse Loan" Introduction - Product Structure Product Definition: "Cloud Warehouse Loan" refers to short-term financing credit business where applicants use legally held or intended-to-purchase commodities stored in warehouses under the Shanghai International Port (Group) Logistics Co., Ltd. as collateral, and establish a sell hedging position of the same type and quantity at Jianxin Futures Co., Ltd. "Cloud Warehouse Loan" Introduction - Product Advantages 》Enhancing Financial Service Quality and Efficiency - Shenyang Bank's Commodity Industry Chain Financial Solutions [SMM Copper Industry Conference] Wulatezhong Banner Investment Promotion Conference April 23 Main Forum Presentation Topic: 76 Years of Striving Forward, Learning from the Past to Build a Stronger Nation - 76 Years of Development Achievements in China's Copper Industry Guest Speaker: Yi Kang, Former President, China Nonferrous Metals Industry Association Presentation Topic: Unpredictable Global Macroeconomics, Outlook for Commodity Allocation Guest Speaker: Zhenhai Hou, Chief Strategist, Straits Financial Group Part One: Trump 2.0's Impact on the World Although Trump has returned to the White House, he still faces intense political battles with the Democrats and the Republican conservatives. The rise of populism in the US is mainly because, although the US economy has grown significantly (nominal GDP grew nearly 40% over the past five years), most of the profits and wealth growth have been captured by large corporations and their shareholders, representing the wealthy class. Since 2020, non-financial corporate profits in the US have nearly doubled. However, most ordinary Americans have not seen an increase in their wealth, and some even feel that their living standards have declined due to the loss of manufacturing jobs, immigration, and rising prices. Data shows that the proportion of the US population dying from despair, drug addiction, and alcoholism has increased sharply over the past 20 years. This situation is particularly significant among white Americans and has not appeared in other developed countries like Europe, the UK, and Australia. Therefore, the core supporters of Trump are "anti-establishment." Three Ideological Foundations of Trump's Domestic and Foreign Policies 1. Mercantilist high-tariff import policy 2. Supply-side economic thinking focused on manufacturing "producers" 3. Traditional American conservative isolationist ideology Trump stated that his political idol is William McKinley, the 25th President of the United States (1,843-1,901). During McKinley's presidency, the main source of federal revenue was tariffs, and there was virtually no personal income tax. This is completely different from today, where about half of the US fiscal revenue comes from personal income tax, and tariffs account for a very small percentage. The reason is that the current US economic structure and world economic model are vastly different from 130 years ago. Today, manufacturing accounts for only 10.2% of the US GDP, compared to 23.2% in 1900. The US is now an economy dominated by services and innovation, and it cannot achieve self-sufficiency in the short term through significantly increasing tariffs or import substitution. The US's dependence on imported non-energy products remains stable at 50-55%. A substantial and comprehensive increase in tariffs, without a sufficient domestic industrial supply chain, would lead to price increases. This is entirely different from the situation in 1900 when the US, as the world's largest industrial nation, had established a complete self-sufficient industrial supply chain. Moreover, over the past four years, wage increases in the US manufacturing sector have actually been greater than in the service sector, but the number of manufacturing jobs continues to decline. This may be because, from 1992 to 2015, US manufacturing wages did not increase in absolute terms for over 20 years. Although wage growth has accelerated in recent years, it still lags behind the overall wage growth in the service sector, making young Americans reluctant to work in manufacturing.But this also means that the overall wage growth in US manufacturing is likely to outpace other countries, making it difficult to support the return of manufacturing. The current state of US industry is still far from encouraging significant capital expenditure. In fact, since 2023, the capacity utilisation rates for semi-finished and finished industrial products in the US have been declining. This is mainly due to the continuous appreciation of the US dollar, the rapid rise in US labor costs, and the persistent decline in domestic prices for finished industrial products. In Q4 2024, the total amount of private sector equipment investment in the US (inflation-adjusted) was $1.33 trillion, compared to $1.21 trillion in Q4 2019, with a cumulative increase of about 10% over five years. Even if Trump introduces policies to encourage domestic manufacturing investment, such as tax cuts, it will be very challenging to significantly reduce the dependence on imports for domestic goods consumption within 2-3 years.

Hou Zhenhai: The global macroeconomic situation is unpredictable, and the outlook for commodity allocation is complex [SMM Copper Conference]

Presentation Topic: Global Copper Market Analysis in 2025

Guest Speaker: Ben Knoefler, Chairman of the Board, KCI Group

Presentation Topic: Current Status and Trends of New Energy Vehicles

Guest Speaker: Liang Yuancong, Rotating Chairman, Yangtze River Delta Automotive Technology Innovation Alliance

Panel Discussion: Future Development Trends of the Global Copper Industry

Moderator: Liu Yang, Head of Greater China Business Development, LME

Panelists: Xiao Qianjun, Vice President of Trading Division, Jiangxi Copper Corporation

Dong Qiaolong, Vice President, Western Mining Co., Ltd.

Eric Medel, Market Intelligence and Strategy Expert, Codelco

Angela Bi, Head of Research and Analysis, Asia Metals and Resources Team, Mercuria

Click to view the panel discussion details

Presentation Topic: Copper Price Trends and Outlook in 2025

Guest Speaker: Ye Jianhua, Director of Big Data, SMM

He analyzed and forecasted the copper price trends in 2025 from the perspectives of macro policy fluctuations due to the uncertainty of US tariffs, the pattern of copper mine resources, import and export data, changes in downstream demand for copper, and the strong resilience of domestic copper consumption.

Presentation Topic: Development of Global Copper Smelting Technology and Digitalization

Guest Speaker: He Feng, Deputy General Manager, China Nerin Engineering Co., Ltd.

Presentation Topic: Current Status and High-Quality Development Trends of China's Copper Processing Industry

Guest Speaker: Tong Qingping, Chief Scientist and PhD, China Nonferrous Metal Mining (Group) Co., Ltd.

1. Copper and Copper Alloys

Properties of Copper

Copper has excellent electrical and thermal conductivity. By adding different elements, various copper alloys can be formed, each with unique properties. For example:

- Electrical (thermal) conductivity ← Pure copper; Strength ← Ni, Cr, Ti, Be; Corrosion resistance ← Ni, Al, Sn; Color ← Zn, Ni, Al; Machinability ← Pb, Bi, Te; Wear resistance ← Sn, Al, Ag; Antibacterial properties, etc.

- Heavy (high density), surface oxidation, high thermal expansion coefficient, and high cost.

Types of Copper Products: Copper pipe, copper billet/bar, copper wire/rod/powder, copper plate, copper strip, copper foil.

Applications of Copper and Copper Alloys

It lists applications in communication, rail transit, automotive, aerospace, shipbuilding, home appliances, robotics, new energy, machinery, and data centers.

Production of Copper Processed Materials

In 2024, China's production of copper processed materials was 21.25 million mt, up 1.9% YoY, with wire accounting for about 50%.

Main Consumption Areas of Copper Processed Materials

It elaborates on the proportion and细分市场的需求。Coal power will gradually phase out, retaining only a small amount for emergency and peak shaving. The country is vigorously developing non-fossil energy to address climate change, ensure energy security, promote economic development, and improve environmental quality. Green energy transition makes significant contributions to global climate change mitigation. According to relevant calculations, China needs approximately 50 trillion yuan in investment to achieve carbon neutrality by 2060, with an average annual investment of 13 trillion yuan. Key point: favorable policies, long-term stability. Trillion-yuan PV market. Rostar Energy: Building Power Stations in My Homeland [SMM Copper Industry Conference] April 24. Forum on Green Development of the Secondary Copper Industry. Topic: Scrap-Produced Anode Copper Becomes a Critical Supplement to Copper Smelting Raw Materials Amid Copper Ore Shortage. Guest Speaker: SMM Analyst Jiang Shanyu. 1. Scrap Copper Smelting Process. Scrap Copper Smelting Process. ► SMM Analysis. Direct Utilization (to processing end): Some scrap does not require smelting and can be directly used as a substitute for electrolytic copper in copper semis production, mainly in the secondary copper rod and brass rod industries. Indirect Utilization (to smelting end): Some scrap must be used as a substitute for copper concentrates, requiring smelting into electrolytic copper before use, known as secondary smelting. Domestic scrap copper smelting mainly uses one-stage and two-stage methods. ► SMM Analysis. • One-Stage Method: This method involves directly adding sorted brass and red copper scrap into a reverberatory furnace for pyrometallurgy, producing anode copper in one step. The advantages are a short process, quick plant setup, and low investment, but it can only handle less complex scrap (copper content over 90%). Complex scrap is difficult to process, with long refining times, high labor intensity, and low metal recovery rates (only 80-85%), and high slag copper content (25-30%). Depending on the type of scrap, the produced anode copper is roughly divided into three categories: red copper anode, brass anode, and secondary blister copper anode. • Two-Stage Method: This method has two stages. In the first stage, scrap is fed into a blast furnace for reduction smelting or into a converter for blowing, producing crude copper. In the second stage, the crude copper is refined in a reverberatory furnace, producing anode copper. This method is called the two-stage method because it involves two processes. Crude copper from blast furnace smelting is black, also known as black copper. Crude copper from converter blowing is also black, often referred to as secondary crude copper to distinguish it from crude copper produced from copper ore. High-zinc brass and white scrap are suitable for blast furnace smelting and reverberatory furnace refining, while high-lead and high-tin scrap should first be blown in a converter, allowing lead and tin to enter the converter slag. The resulting secondary crude copper is then refined in a reverberatory furnace. With this method, copper recovery can reach over 96%, with slag copper content at 0.8-2%, and zinc recovery in flue dust can reach over 80%. The two-stage method is widely used in China. Compared to the one-stage method, the two-stage method increases copper recovery by about 5% and reduces energy consumption by about 100 kg of standard coal per ton of anode copper. • Three-Stage Method: Scrap is first smelted in a blast furnace to produce black copper, which is then blown in a converter to produce secondary crude copper, and finally refined in a reverberatory furnace to produce qualified anode plates. This method involves three processes, hence the name three-stage method. Blast furnace smelting aims to remove most of the zinc from the charge, producing impure black copper, which is then blown in a converter to remove lead and tin, producing secondary crude copper. The secondary crude copper is refined in a reverberatory furnace to produce qualified anode plates. Although the three-stage method has a longer process, more equipment, higher investment, and greater complexity, it can handle various complex scrap and has good comprehensive utilization, making it popular among many large-scale secondary copper plants. Anode Copper Smelting Process. 2. Rapid Growth in the Market Size of Scrap-Produced Anode Copper. The Chinese anode copper market is substantial. It was explained from the perspective of China's copper raw material supply-demand balance from 2020-2030E and China's refined copper production. Deteriorating spot TC for copper concentrates forces smelters to seek alternative raw materials. It discussed spot TC for copper concentrates, comparison of advantages of copper smelting raw materials, and SMM's forecast of global copper concentrate supply-demand balance (including supply and demand disruption rates) from 2021-2028E. The proportion of secondary copper flowing to the smelting end is gradually increasing. Distribution of Chinese Anode Copper Capacity. ► SMM Analysis. SMM statistics show that China's anode copper capacity (excluding self-use) is about 5.53 million mt, with a high proportion using secondary copper as raw material, mainly distributed in east China, but with low actual capacity utilization. Ore-Made and Scrap-Produced Anode Copper. Domestic anode copper pricing method: (the party with pricing rights selects futures prices - processing fee) × copper metal content. ► SMM Analysis. Ore-made anode copper is mainly concentrated in north China, primarily circulating through long-term contracts, with relatively stable operating rates and processing fees. Scrap-produced anode copper, influenced by policies, is mainly concentrated in south China, with relatively high fluctuations in operating rates and processing fees. Distribution of Supply and Demand in the Chinese Anode Copper Market. ► SMM Analysis. The east China market is large and growing rapidly, but China still relies on imported anode copper, with the largest gap in north-west China, showing a clear mismatch between supply and demand. In recent years, the production of scrap-produced anode copper has increased rapidly, accounting for a growing share. In recent years, anode copper imports have declined, while imports of secondary copper ingots have grown rapidly. SMM: It is expected that the proportion of scrap copper flowing to the smelting end will gradually increase, and the growth rate of anode copper demand may slow down [SMM Copper Industry Conference]. Topic: Application of Secondary Copper in Copper Foil Enterprises. Guest Speaker: Xie Houyuan, Purchasing Director, Shenzhen Longdian Huaxin Technology Co., Ltd. 1. Overview of Recycled Copper. Overview of Recycled Copper. Global/China Annual Recycled Copper Volume. Global Trend of Resource Recycling. Resource Conservation and Cost-Sensitive Scenarios: Shortage of primary copper resources, cost reduction and efficiency improvement needs. Environmental Protection and Sustainable Development Requirements: Low-carbon industries, energy-intensive sectors. Policy-Driven Scenarios: Mandatory recycling policies, international trade compliance. Specific Performance Requirements: Integrated circuit boards, communication cables; medical devices, aerospace, military. Forms of Recycled Copper. Physical Forms: Block/bar (copper pipe, copper plate, copper rod); wire/cable copper; copper shavings/powder. Chemical Forms: Pure copper (electrolytic copper), copper alloys; copper oxide/copper compounds, plated copper materials. Utilization Methods of Recycled Copper. Direct Reuse: Directly processed into new copper semis (such as copper rods, copper wires). Used for construction, power equipment repair or replacement. Advantages: no smelting required, low cost, and low energy consumption. Smelting and Regeneration: Smelted and cast into copper ingots (such as electrolytic copper anode plates). Used for producing copper wire, copper pipe, copper alloys, and other basic materials. High-Value Deep Processing: High-purity copper materials. Used for: 3D printing metal powders, electronic industry copper foil, copper clad laminate, NEV battery connectors, etc. Compound Extraction: Preparation of copper sulphate, copper oxide, and other chemical products. Used for agricultural fungicides, industrial catalysts. Current Status and Technical Challenges of Recycled Copper. Future Breakthrough Directions: • Intelligent Sorting - Improved utilization; green financial tool innovation - expanded breadth and depth of recycling; alignment with international standards - global collaboration and policy support. It is expected that the industry concentration will increase to over 60% by 2030. 2. Copper Foil Industry and Copper Foil Applications. High-Precision Electrolytic Copper Foil Products & Downstream Applications. ► Copper Foil Production Process. High-precision electrolytic copper foil refers to a product formed on the surface of a cathode roller through electrolysis, using a copper sulfate solution made from copper with a purity of over 99.9%. ► Copper Foil Applications. Divided into lithium-ion battery copper foil and electronic circuit copper foil, used for lithium-ion battery negative electrode current collectors and electronic circuit manufacturing. ► Impact on New Energy Development. The thickness and performance of lithium-ion battery copper foil directly affect the energy density and safety of lithium batteries. For example, ultra-thin copper foil can increase the energy density of lithium batteries by 5-11%, significantly impacting the driving range of NEVs. Application of Recycled Copper in Copper Foil Enterprises [SMM Copper Industry Conference]. Topic: Empowering Nonferrous Metal Industry Development Through National Land Port Logistics Hubs—A Case Study of Yingtang International Land Port. Guest Speaker: Sun Jingfeng, Director of Yingtang International Land Port Management Office. I. Overview of the Land Port. Total planned area: 13.4 square kilometers, constructed area: 1,164 mu, total investment: 2.2 billion yuan, core area: 554 mu. "Six-in-One" Development Model. Focusing mainly on the copper industry, the land port is built to shift port functions inland, enabling local customs clearance, sea-rail intermodal transport, and seamless connectivity. It aims to create an inland open platform for the Yingrao-Fuzhou-Changzhou copper-based new materials cluster, integrating import and export trade, processing, bonded warehousing, spot copper trading, and supply chain finance. Yingtang International Land Port Transportation and Storage Center. ► Customs Supervision Operation Site. Officially operational since May 8, 2023, it mainly handles inspection and other functions for import and export business at the land port. The project covers over 80,000 m², with a designed throughput of 20,000 TEUs/year and an inspection capacity of 10,000 TEUs/year. After its operation, it functions like a port and customs checkpoint, allowing companies to complete all customs procedures at their doorstep. Currently, the supervision operation site is fully operated by Yingtang Customs. ► Sea-Rail Intermodal Transport. Currently, there are sea-rail intermodal routes connecting Yingtang International Land Port with Ningbo Beilun, Fujian Xiamen, Fujian Fuzhou, Fujian Quanzhou, and Guangzhou Nansha, achieving seamless connections with coastal ports. Import and export goods include recycled copper, copper concentrates, electrolytic copper, aluminum ingots, fertilizers, copper products, and grains. Goods can be cleared at Xiamen Port within one and a half working days, and transported by rail to and from Ningbo Beilun Port within five days. To date, Yingtang International Land Port has partnered with several well-known international shipping companies, such as COSCO Shipping, Maersk, Mediterranean Shipping Company, ZIM, Wan Hai Lines, Evergreen Line, and Pacific International Lines, covering routes to Europe, Asia, Africa, and the Americas, achieving the initial goal of "buying globally." ► Bonded Warehouse. By 2024, 17,100 tons of goods had been stored, with a bonded value of 1.034 billion yuan, deferring VAT of 131 million yuan. In 2025, the bonded warehouse is expected to store 50,000 tons of goods, with a value of 3 billion yuan. The bonded warehouse is supported by renowned domestic and international warehousing and operations management companies, such as Shanghai National Reserve Logistics and PGS Group, providing top-notch technology and team support.Overseas Warehouses: Thailand Warehouse: Alibaba Group, PGS Warehouse: LME South Africa Warehouse, Ningbo Zhenhai Warehouse: Lingang Intelligent Warehousing (Ningbo) Co., Ltd.

Sea-Rail Intermodal: Currently, sea-rail intermodal routes have been opened from Ningbo Beilun, Xiamen, Fuzhou, Quanzhou in Fujian, and Nansha in Guangzhou to Yingtan International Land Port, achieving seamless connection with coastal ports. Import and export goods include secondary copper, copper concentrates, copper cathode, aluminum ingot, fertilizer, copper products, and grain, which can be cleared at Xiamen Port within one and a half working days, and transported by rail at Ningbo Beilun Port with a round trip of five days.

China-Europe Freight Train: On May 29, 2022, Yingtan International Land Port was officially opened and the China-Europe Freight Train officially began operation. In April 2023, it was listed as a scheduled station for the China-Europe Freight Train. In July 2023, Yingtan Land Port was included in the National Development and Reform Commission's list of national logistics hub construction for land ports.

Central Region Nonferrous Metals Trading Center: A cluster of copper processing and resource recycling industry enterprises was formed, officially launched on May 9, 2023, with 268 enterprises currently introduced, including representative companies such as Xingqi Group, Yucheng Group, JCC Renewable Resources, and Changsheng Precious Metals.

Yingtan International Land Port: Building a first-class international inland port and creating a world copper raw material distribution center [SMM Copper Industry Conference].

Speech Topic: Analysis of Downstream Consumption Status of Secondary Copper in China. Guest Speaker: Junbing Zhang, Head of Secondary Copper Operations, Zhejiang Hailiang Co., Ltd.

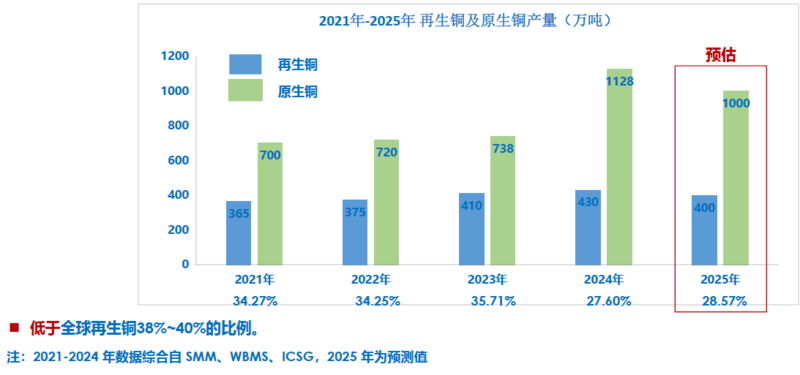

Secondary Copper Industry Chain: 1. Sources of Copper Scrap: Industrial Scrap (60%): Off-cuts from smelting/processing (e.g., copper chips, anode slime). Manufacturing Scrap (e.g., leftover materials from wire and cable production). Post-consumer Scrap (40%): Scrapped electronic devices (computers, mobile phones), automobiles (motors, wiring harnesses), construction waste (pipes). 2. Secondary Copper Production Process: Scrap Classification: High-grade scrap can be directly smelted; low-grade scrap needs to be dismantled and sorted. Dismantling and Pre-treatment: Mechanical crushing, magnetic separation (iron separation), eddy current separation (aluminum separation), manual sorting (plastic separation). Smelting and Refining: Reverberatory furnace/electric furnace smelting: Low-grade scrap, producing blister copper followed by electrorefining. Converter smelting: High-grade scrap, directly producing copper anode. 3. Distribution of Secondary Copper Industry: Raw Material Exporting Countries: US (15% of global exports), Germany (9%), Japan (6%), mainly exporting low-grade scrap copper. Processing and Consuming Countries: Domestic: 35% of global secondary copper consumption, with Ningbo, Zhejiang (imported scrap copper dismantling) and Yingtan, Jiangxi (scrap copper refining) as core bases. Southeast Asia: Malaysia and Thailand, relying on bonded zone policies, have become transit and processing centers for European and American scrap copper.

Secondary Copper - Significant Energy and Economic Advantages: It introduces the global and domestic upstream copper production situation over the past five years from the perspectives of mine copper production and refined copper production.

Domestic Secondary and Primary Copper Production: 02 Distribution of Secondary Copper Industry.

Global Secondary Copper Industry Distribution: Major Exporting Countries/Regions: North America: US: The world's largest secondary copper exporter; Canada: Relying on the North American automotive industry chain, mainly exporting to the US and East Asia. Europe: Germany: Europe's largest secondary copper exporter; UK and the Netherlands: Relying on port advantages, becoming hubs for European secondary copper trade. Japan: Asia's major exporter, mainly from home appliance and automobile dismantling; "Home Appliance Recycling Law": Mandatory recycling of scrapped appliances, forming an efficient recycling system. Major Importing Countries/Regions: Domestic: The world's largest importer and consumer, accounting for over 30% of global trade. Southeast Asia (Malaysia/Thailand/Indonesia): Proximity to China and relaxed policies (e.g., Malaysia allows non-metal processing in bonded zones) attract European and American secondary copper transit and local dismantling. Other Countries: South Korea and India: South Korea relies on electronic industry scrap, with a secondary copper self-sufficiency rate of 30%; India's scrap copper imports are growing year by year, mainly used for low-end copper product processing. Domestic Trade/Processing Concentrated Areas: Tongling, Anhui; Daye, Hubei: Combined with local primary copper smelting capacity, synergistically processing scrap copper; Yingtan, Jiangxi: Relying on JCC Group, forming a "scrap copper dismantling - smelting - refining" industry chain; Bohai Rim Economic Zone: Linyi, Shandong ("Copper Capital of the North"), Baoding, Hebei (scrap wire and cable dismantling); Yangtze River Delta: Ningbo, Zhejiang (main port for imported scrap copper), Zhangjiagang, Jiangsu; Pearl River Delta: Foshan, Guangdong (trade hub for scrap brass and copper alloys).

Global Secondary Copper Industry Chain Distribution Characteristics: Global Secondary Copper Industry Distribution: From 2021 to 2025, global secondary copper exports show a "US dominance, regional differentiation" feature, with Mexico, Saudi Arabia, and other countries rising due to geopolitical advantages, while traditional European exporting countries' shares gradually decline.

Zhejiang Hailiang: Detailed Explanation of Future Challenges and Opportunities in Secondary Copper and Main Corporate Strategies [SMM Copper Industry Conference].

Speech Topic: From Resource Recycling to a Low-Carbon Future, Building a Sustainable Recycling Industry Ecosystem. Guest Speaker: Chao Liu, Marketing Director, Tianjin Sinone Renewable Resource Co., Ltd.

Roundtable Discussion: How to Better Promote High-Quality Development of the Secondary Copper Industry - Supply and Consumption. Moderator: Shilong Li, Chairman, China Technology Innovation Strategic Alliance for Resources Recycling Industry (CIAR). Panelists: Zhanzhi Chen, Executive Vice Chairman/Chairman, Guangdong Xingqi Group/Jiangxi Zhongli Resources Holding Co., Ltd.; Jianqing Liu, Deputy General Manager, Jiangxi Yuexing Copper Co., Ltd.; Yifu Huang, Executive Deputy General Manager, Jiangxi Copper Renewable Resources Co., Ltd.; Chao Shen, Chairman & General Manager, Jiangxi Copper Capital Digital Service Co., Ltd.

Copper-Based New Materials High-Quality Development Forum. Speech Topic: 2025 Global Copper Foil Industry Landscape and Market Outlook. Guest Speaker: Shaoxue Yu, Senior Research Manager, SMM.

1. Current Development of Global Copper Foil Market: 2024 Global Copper Foil Capacity Distribution: By the end of 2024, global copper foil capacity is 2.4202 million mt, including 1.436 million mt of lithium battery copper foil and 985,000 mt of electronic circuit copper foil. China's copper foil capacity is 1.94 million mt, accounting for 80% of global total capacity. Jiangxi, Guangdong, and Taiwan in China are the world's major copper foil production areas.

2023-2025E Global Copper Foil Capacity and Production Analysis: Global electronic circuit copper foil and lithium battery copper foil capacity show a year-on-year growth pattern, with lithium battery copper foil capacity expanding rapidly. By the end of 2024, global lithium battery copper foil capacity is 1.44 million mt, production is 840,000 mt, up 25.4% YoY; global electronic circuit copper foil capacity is 980,000 mt, production is 590,000 mt, up 5% YoY.

SMM Analysis: In recent years, lithium battery copper foil capacity has accelerated expansion, with severe overcapacity leading to price wars, intensified market competition, and increased corporate operating pressure. Future capacity growth will significantly slow down. The electronic circuit copper foil industry is relatively stable, with slower market expansion, but lacks capacity for flexible PCB copper foil and high-frequency high-speed circuit copper foil, relying on imports.

2025Q2 Downstream Raw Material Inventory Shows Buildup Trend, Copper Foil Operating Rate Slows: SMM expects the overall operating rate of copper foil enterprises in April 2025 to be 72.77%, up 0.95 percentage points MoM and 1.86 percentage points YoY. The operating rate of lithium battery copper foil in April is expected to be 69.77%, up 0.39 percentage points MoM and 2.47 percentage points YoY. The operating rate of electronic circuit copper foil in April is expected to be 78.60%, up 2.04 percentage points MoM and 1.07 percentage points YoY.

Tariffs Will Affect Medium and Long-Term Downstream Consumption: In March 2025, SMM battery cell inventory was 216.0 GWh, up 1.6% MoM, and is expected to continue building in April.