View SMM Lead Product Quotes, Data, and Market Analysis

Order and View SMM Metal Spot Historical Prices

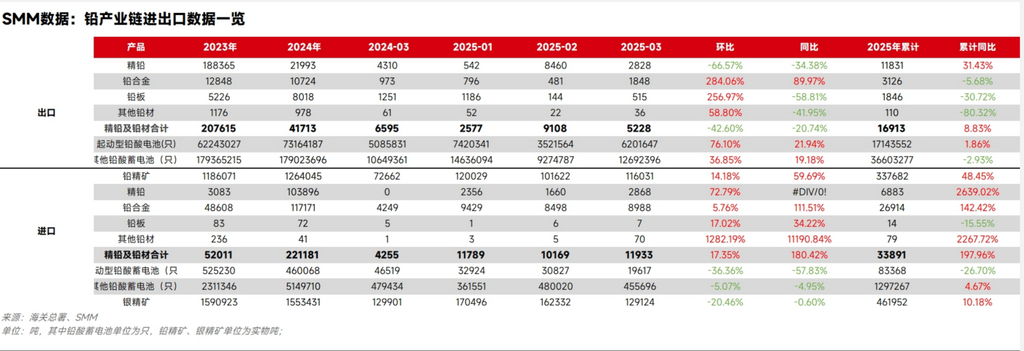

SMM April 22 News:

According to customs data, export details: In March 2025, refined lead exports were 2,828 mt, down 66.57% MoM and 34.38% YoY. The total exports of refined lead and lead products in March were 16,913 mt, up 8.83% cumulatively YoY. Import details: In March 2025, refined lead imports were 2,868 mt, lead alloy imports were 8,988 mt, and the total imports of refined lead and lead products in March were 33,981 mt, up 197.96% cumulatively YoY.

In March, with the Chinese New Year factor lifted, the lead market showed a pattern of both supply and demand increasing. Primary lead and secondary lead smelters resumed production intensively, coupled with the release of new capacity for secondary lead, the monthly increase in lead ingot supply exceeded 50%. As lead-acid battery enterprises resumed normal production, the procurement demand for lead ingots increased simultaneously. At the beginning of March, the Two Sessions were held in China, proposing many policies to boost the economy, easing market concerns about the US tariff hike. Non-ferrous metals in the Shanghai market generally returned to positive territory, and SHFE lead held up well, reaching a monthly high of 17,805 yuan/mt, the highest level in nearly three months. The import window briefly opened, with overseas lead ingots arriving at ports in mid-March. In late March, expectations of a US tariff hike were layered, and the traditional off-season expectation for the lead consumer market rose, leading to a pullback in lead prices, almost erasing all gains since March, and the import conditions no longer held.

April is the traditional consumption off-season for China's lead-acid battery market, mainly due to the weakening replacement demand for e-bike and automotive battery markets. According to SMM, some lead-acid battery enterprises reported a decline in new orders, and producers intended to cut production and reduce inventory to lower finished product inventories. In addition, some downstream battery producers stopped production for the Qingming Festival holiday, leading to a phased reduction in lead consumption. Moreover, in early April, due to a significant drop in LME lead, the SHFE/LME lead price ratio expanded, and the lead ingot import window was on the verge of opening. If the import source country is a zero-tariff agreement country, the refined lead import window has already opened; the actual import situation of lead ingots still needs to be monitored based on data released by Chinese customs.

Due to tight raw material supply and high prices, domestic lead costs are high, especially the firm prices of metals such as antimony and tin directly causing an upward trend in lead alloy prices. Recently, domestic lead ingot and lead product exports have been at a disadvantage.