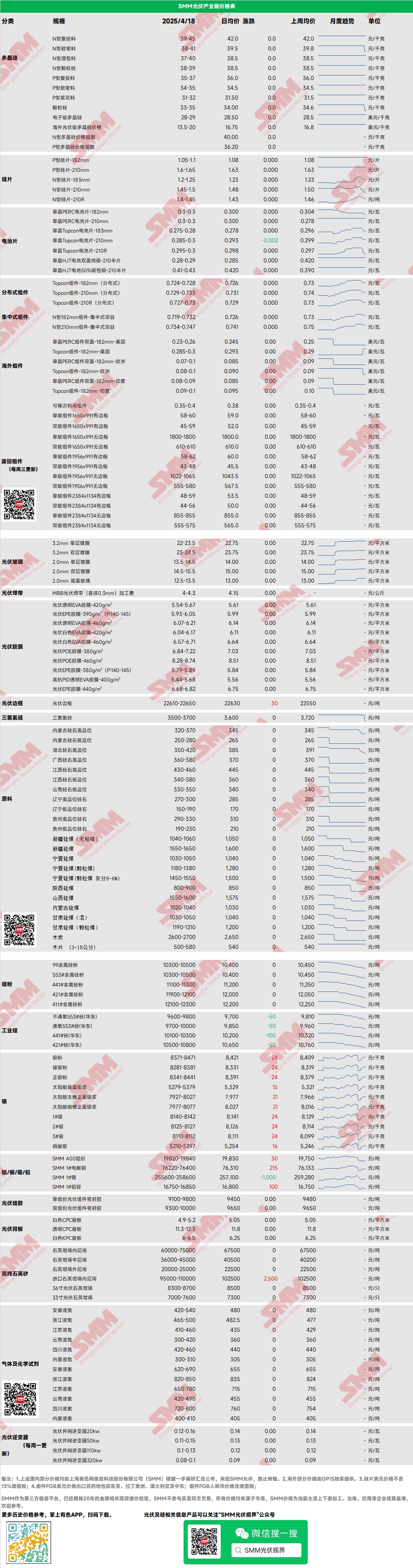

Polysilicon: This week, the mainstream transaction prices for N-type recharging polysilicon ranged from 39-45 yuan/kg, and for N-type dense polysilicon, the prices ranged from 37-41 yuan/kg. Polysilicon prices fell this week, as downstream market prices significantly dropped, affecting upstream sentiment, coupled with increased willingness of some top-tier polysilicon enterprises to sell externally, leading to a decline in polysilicon prices. This week, it was reported that a top-tier enterprise concluded a large order with a downstream crystal pulling plant at 37 yuan/kg, but the market debunked this, and no actual transaction occurred. Futures prices significantly deviated from previous industry expectations, and some polysilicon enterprises began to show intentions to stand firm on quotes today. As the installation rush season nears its end, from a demand perspective, the downstream PV industry chain is expected to be pessimistic.

Wafer: This week, domestic N-type 18Xmm wafers were priced at 1.2-1.25 yuan/piece, N-type 210R at 1.4-1.45 yuan/piece, and N-type 210mm wafers at 1.5-1.55 yuan/piece. Wafer prices continued to pull back this week, with all sizes declining, though 183 prices remained relatively firm, while 210R market prices dropped significantly. Affected by frequent price drops, solar cell manufacturers have lower price expectations for wafers, leading to some price competition between small wafer factories and top-tier large factories. There is a certain divergence in the intended transactions between wafer enterprises and downstream, resulting in price negotiations.

Cell: The decline in solar cell prices has begun, with market conditions diverging in sub-markets. Affected by oversupply from upstream and downstream, cost and demand support weakened, leading to a general decline in cell prices. In the mainstream Topcon cell market, 183N and 210RN are temporarily in a downward trend, with average prices dropping from 0.298 yuan/W to 0.293 yuan/W and from 0.295 yuan/W to 0.285 yuan/W, respectively; 210N remained stable around 0.298 yuan/W.

Module: This week, module price declines expanded, with distributed N-type 182 modules currently priced around 0.724-0.728 yuan/W, with an average price decrease of 0.022 yuan/W from last Friday, and distributed N-type 210 modules currently priced around 0.729-0.733 yuan/W, with an average price decrease of 0.022 yuan/W. Distributed N-type 210R modules are currently priced around 0.727-0.73 yuan/W, with an average price decrease of 0.026 yuan/W from last Friday. Centralized N-type 182 modules are currently priced around 0.719-0.732 yuan/W, with an average price decrease of 0.008 yuan/W from last Friday, and centralized N-type 210 modules are currently priced around 0.734-0.747 yuan/W, with an average price decrease of 0.008 yuan/W from last Friday. This week, module prices declined relatively significantly. In the centralized market, the 5.31 electricity reform policy document has not been finalized, preventing end-users from assessing and adjusting IRR revenue models, leading to a general weakening of domestic demand expectations. The termination of the 51GW centralized procurement by China Power Construction also indirectly confirmed this fact. In the distributed market, as top-tier enterprises lowered prices to gain market share, the average transaction price continued to decline, with the top five enterprises' transaction prices beginning to converge, and some second and third-tier enterprises have already seen distributed orders below 0.7 yuan/W.

End-user: From April 7 to April 13, 2025, SMM statistics showed that domestic enterprises won 40 sections of PV module projects, with 22 projects disclosing installed capacity. This week's procurement finalized module models included N-type Topcon PV modules and lightweight flexible modules. The winning bid price distribution for conventional crystalline silicon modules was concentrated at 0.66-0.93 yuan/W, and the price for lightweight flexible modules was 1.18 yuan/W; the weekly weighted average price was 0.73 yuan/W, up 0.01 yuan/W from last week; the total procurement capacity of winning bids was 952.27MW, down 1,654.66 MW from last week. The total capacity of N-type modules explicitly marked for procurement in the statistical week was about 833.76MW, accounting for 87.56%.

EVA: This week, PV-grade EVA prices remained stable, with mainstream transaction prices maintained in the range of 11,550-11,950 yuan/mt, showing a high-level consolidation trend, while foam-grade and cable-grade EVA fell by 100 yuan/mt WoW. On the supply side, some petrochemical plants switched to producing PV-grade EVA, alleviating the tight spot supply to some extent. However, with the recent downward trend in PV module prices and the obvious weakening of the installation rush, coupled with the stable operation of new EVA film orders in April, the upward trend of PV-grade EVA prices is limited, and it is expected that EVA prices will show a high-level fluctuation trend in the near future.

Film: The mainstream price range for EVA film was 13,300-13,500 yuan/mt, and for EPE film, it was 15,200-15,500 yuan/mt, with prices remaining stable. On the demand side, recent module price adjustments have led to a slowdown in market demand. On the cost side, PV-grade EVA prices are consolidating at high levels, with both demand and cost sides slowing down. Film prices are expected to remain stable for the time being, but as future demand continues to weaken, new film orders in May may show a downward trend.

POE: Domestic delivery-to-factory prices for POE remained stable at 12,000-14,000 yuan/mt, with prices temporarily stable. Although some petrochemical enterprises are expected to undergo maintenance, with the weakening of the installation rush and gradually slowing demand, coupled with the release of new capacity in the later period, it is expected that PV-grade POE prices may show a downward trend.

PV Glass: This week, the quotation range for PV glass remained stable, with the quotation center moving downward. As of now, the mainstream quotation for domestic 2.0mm single-layer coating is 14.0 yuan/m², the mainstream transaction price is 13.8 yuan/m², the mainstream quotation for 3.2mm single-layer coating is 22.5 yuan/m², and the mainstream quotation for 2.0mm back glass is 13.0 yuan/m². This week, domestic glass trading volume was low, constrained by the decline in module prices and a slight weakening in module production schedule. The inventory days of glass enterprises increased by one day WoW, so module enterprises have recently focused on driving down prices in procurement. As glass enterprises still have profit margins, they slightly lowered their quotations.

High-Purity Quartz Sand: This week, the low price of domestic high-purity quartz sand mid-layer sand slightly increased, while other sand prices remained temporarily stable. Current market quotations are as follows: inner-layer sand at 65,000-75,000 yuan/mt, mid-layer sand at 36,000-45,000 yuan/mt, and outer-layer sand at 20,000-25,000 yuan/mt. Recently, import sand traders slightly increased their quotations, but as of now, the market trading volume is low, downstream enterprises' raw material inventories have not been consumed, and the next batch of import sand is about to arrive at the port, so there is no short-term supply risk. The market is mainly inquiring, with no procurement mentality. Recently, domestic sand prices followed import sand quotations to increase, but the mainstream transaction center of the market remained temporarily stable. Against the backdrop of continuously declining crucible demand, it is expected that the market trading volume will be limited in the future, and quartz sand prices will mainly be negotiated.

》View SMM PV Industry Chain Database

![[SMM PV News] Armenia Hits 1.1 GW Solar Capacity,](https://imgqn.smm.cn/usercenter/qQwIB20251217171741.jpg)

![Spot Market and Domestic Inventory Brief Review (February 5, 2026) [SMM Silver Market Weekly Review]](https://imgqn.smm.cn/usercenter/tSwaX20251217171735.jpg)