According to the SMM survey, the profit per ton of coke this week was 49.4 yuan/mt, with the first round of price increases implemented, and the profitability of most coke enterprises improved.

From a price perspective, the first round of coke price increases was implemented this week, positively impacting the profit per ton of coke for coke enterprises. From a cost perspective, most coal mines maintained normal production, and recent coking coal price adjustments led to cautious purchasing by downstream buyers, mainly purchasing as needed. Coal mine shipments were moderate, with online auctions showing mixed performance. Some coal types had higher starting prices, and there were still instances of failed auctions. Coking costs remained stable.

Next week, coke prices are expected to see a second round of increases, potentially further improving the profitability of coke enterprises. Meanwhile, online auctions for coking coal showed mixed performance, and coking costs remained stable. Therefore, it is expected that most coke enterprises will further expand their profits.

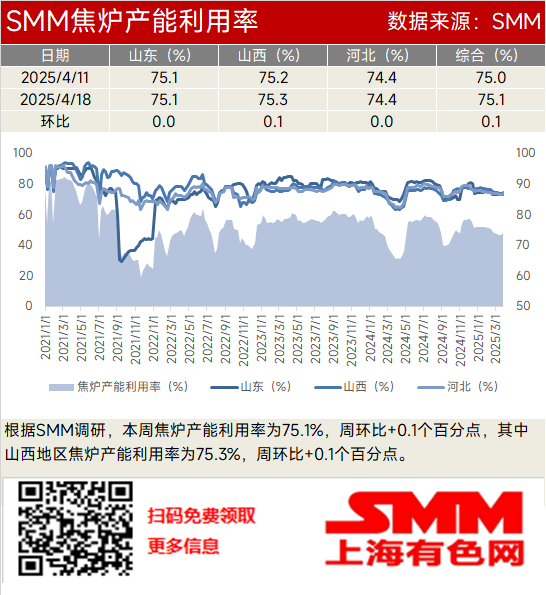

2. According to the SMM survey, the coke oven capacity utilization rate this week was 75.1%, up 0.1 percentage points WoW, with the rate in Shanxi at 75.3%, also up 0.1 percentage points WoW.

From a profitability perspective, most coke enterprises were profitable this week, and production enthusiasm was moderate. From an inventory perspective, coke enterprise shipments were good, and overall coke inventory continued to decline, positively impacting production.

Subsequently, the profitability of most coke enterprises is expected to increase, and with their coke inventory at low levels, production enthusiasm is good. At the same time, apparent steel demand exceeded market expectations, and with moderate profit per ton of steel, pig iron production at steel mills remained high, creating rigid demand for coke. In summary, the coke market is in a tight balance, and with the profitability of coke enterprises being moderate, the coke oven capacity utilization rate may increase slightly next week.

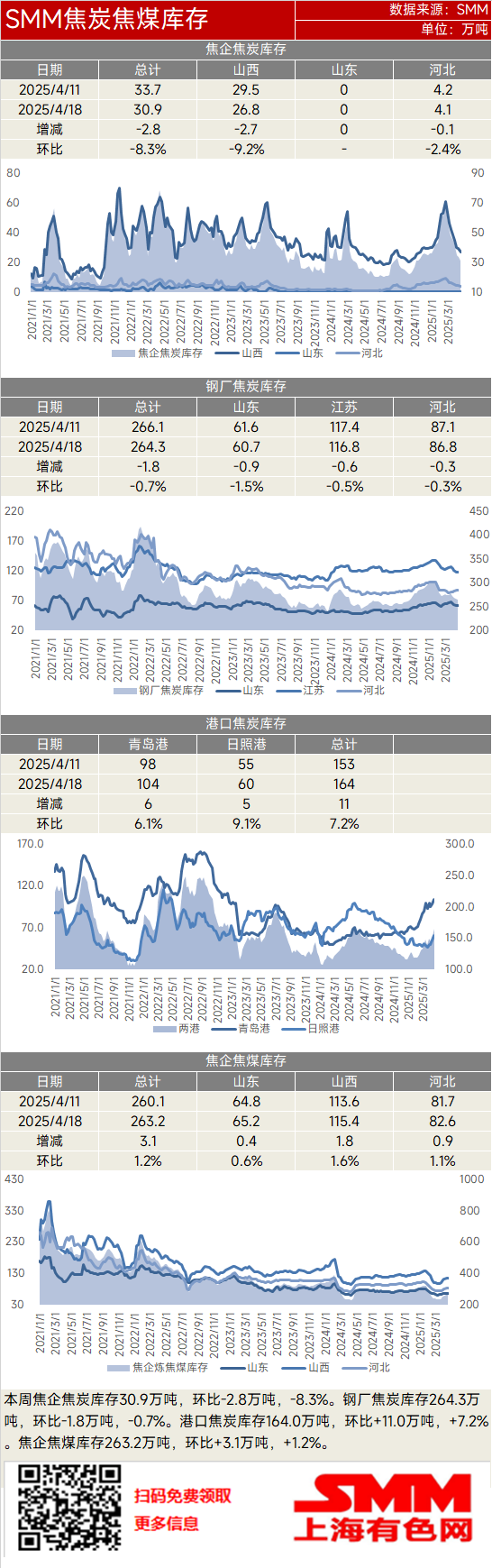

3. This week, coke inventory at coke enterprises was 309,000 mt, down 28,000 mt WoW, a decrease of 8.3%. Coke inventory at steel mills was 2.643 million mt, down 18,000 mt WoW, a decrease of 0.7%. Coke inventory at ports was 1.64 million mt, up 110,000 mt WoW, an increase of 7.2%. Coking coal inventory at coke enterprises was 2.632 million mt, up 31,000 mt WoW, an increase of 1.2%.

This week, coke inventory at coke enterprises continued to decline, while coke inventory at steel mills decreased slightly. Overall production enthusiasm at coke enterprises was moderate, and coke supply increased slightly. At the same time, pig iron production at steel mills remained high, creating rigid demand for coke. Some steel mills with low coke inventory restocked, leading to a decline in coke inventory at coke enterprises. This week, steel market transactions exceeded market expectations, and pig iron production at steel mills remained high, resulting in significant coke consumption. Even with some steel mills restocking, it was difficult to offset daily consumption.

Subsequently, coke supply is expected to increase slightly, and with pig iron production at steel mills remaining high, there will be continued consumption of coke, with restocking as needed. It is expected that coke inventory at coke enterprises will remain low next week, while coke inventory at steel mills will barely stabilize.

This week, coke supply increased slightly, and steel mills restocked as needed. The first round of coke price increases was implemented, but with the recent delivery period, spot cargo continued to gather at ports. It is expected that coke inventory at ports will increase next week.

This week, coking coal inventory at coke enterprises increased, and sales were good, leading to increased demand for coking coal. Coking coal prices are already at reasonable levels, and some coke enterprises with low coking coal inventory began restocking. Subsequently, the upward trend in coking coal prices was hindered, and online auctions for coking coal showed mixed performance. However, coal mines also had a strong sentiment to stand firm on quotes, and some coke enterprises and steel mills have rigid demand. Therefore, it is expected that coking coal inventory at coke enterprises will stabilize next week.

![Before the holiday, the black chain is unlikely to see a trend-driven market [SMM Steel Industry Chain Weekly Report].](https://imgqn.smm.cn/usercenter/zUFfM20251217171748.jpg)

![[SMM Chromium Daily Review] Inquiries and Transactions Weakened, Chromium Market Showed Mediocre Performance Before the Holiday](https://imgqn.smm.cn/usercenter/ENDOs20251217171718.jpg)