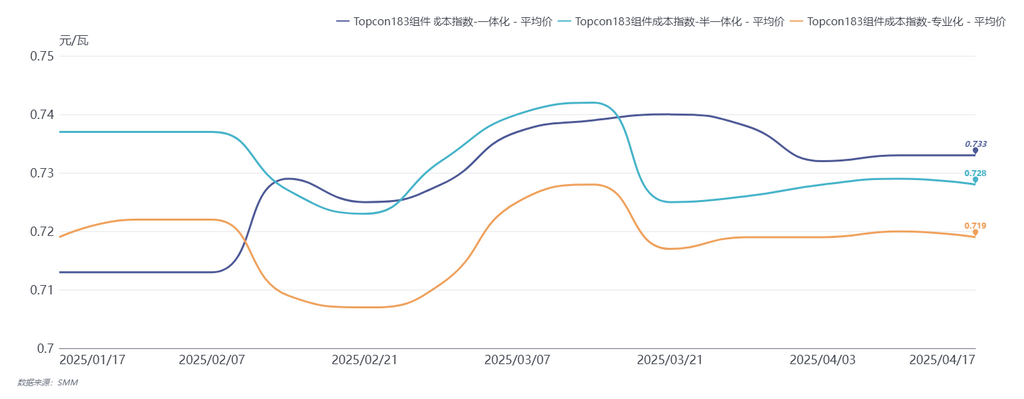

The full cost of integrated enterprises (wafer-cell-module) dropped to 0.733 yuan/W.

The full cost of semi-integrated enterprises (cell-module) rose to 0.728 yuan/W.

The full cost of specialized enterprises (module) rose to 0.719 yuan/W.

SMM data shows:

Auxiliary material segment: the price of 2.0mm double-layer coated glass increased by 0.25 yuan/m²; the price of 36-inch quartz crucibles decreased by 240 yuan/piece; the price of solar cell busbar front-side silver paste decreased by 313.8 yuan/kg; the price of solar cell rear-side silver paste decreased by 209.4 yuan/kg; the price of PV frames decreased by 1,182 yuan/mt.

Main material segment: the price of N-type wafer-183mm increased by 0.08 yuan/piece; the price of monocrystalline TOPCon cell-183mm increased by 0.007 yuan/W.

[Non-silicon cost reduction of 0.006 yuan/W helps module cost reduction]

The full cost of integrated module enterprises (wafer-cell-module) decreased, mainly due to the price reduction of most auxiliary materials except glass, resulting in a non-silicon cost reduction of 0.006 yuan/W. The main material cost remained largely unchanged as the average price of polysilicon was not adjusted. During the phased downward cycle of the PV industry chain, the phenomenon of cost inversion between specialized module enterprises and integrated enterprises continues, but the price spread shows a narrowing trend. This week, the spot selling price of modules (excluding freight) has approached the full cost, and some forward orders for May delivery have already fallen below the full cost. Some low-price orders have incurred losses of 0.01-0.02 yuan/W.

[After the inflation bubble bursts, auxiliary material prices usher in a cyclical reversal]

Looking ahead, after the inflation bubble bursts, commodities are expected to experience a cyclical reversal. Under the dual effects of continuously declining auxiliary material prices and the drag of the PV cycle downturn on main materials (polysilicon/wafer/cell), module costs are expected to further decrease. In addition, with the accelerated iteration of new technologies such as BC and HJT, as well as the release of scale effects and vertical integration advantages of integrated enterprises, the cost structure difference between specialized and integrated enterprises will gradually narrow, and even reverse.

View SMM PV industry chain database

![[SMM PV News] Armenia Hits 1.1 GW Solar Capacity,](https://imgqn.smm.cn/usercenter/qQwIB20251217171741.jpg)

![Spot Market and Domestic Inventory Brief Review (February 5, 2026) [SMM Silver Market Weekly Review]](https://imgqn.smm.cn/usercenter/tSwaX20251217171735.jpg)