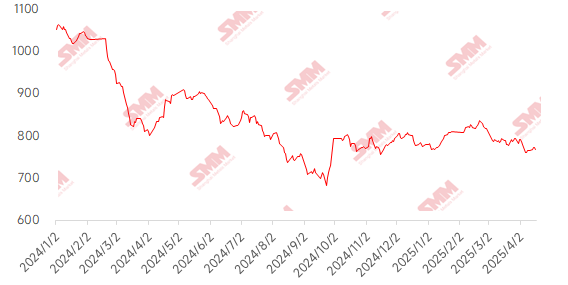

Iron ore prices fluctuated upward this week. The tariff war between China and the US has temporarily come to an end, and market sentiment has improved. The actual impact remains to be seen. The fundamentals of iron ore this week were supportive, with a strong supply and demand pattern overall. In terms of supply, overseas shipments increased slightly, but port arrivals surged by over 13%, remaining at a high level. Daily pig iron production continued to grow by 4,500 mt, higher than the same period last year. Iron ore demand remained high, and port inventory dropped significantly for two consecutive weeks. Additionally, industry data performed well, with the apparent demand for rebar expanding this week, and the decline in inventory of the five major steel products widening. Overall, the supply and demand fundamentals of the steel industry remain healthy. In the spot market, the price of PB fines at Shandong ports rose by 10 yuan/mt MoM.

Chart: SMM 62% Imported Ore MMi Index

Data source: SMM

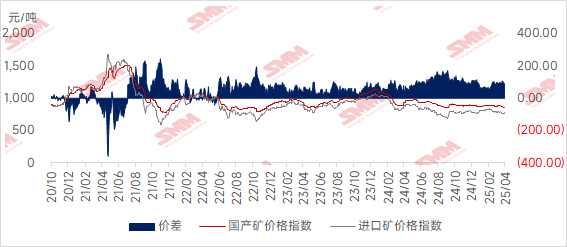

Domestic ore prices dropped slightly this week, and domestic ore prices are expected to remain in the doldrums next week. Prices in Tangshan, Qian'an, and Qianxi in Hebei rose by 5-10 yuan/mt, while prices in west Liaoning, Chaoyang, Beipiao, and Jianping fell by 1-5 yuan/mt. Prices in east China dropped by 30-40 yuan/mt.

The iron ore concentrate market in Tangshan remained stable in many areas, with the delivery-to-factory price of 66-grade dry basis tax-included at 930-940 yuan/mt. Beneficiation plants operated at low levels, and inventory reduction at material yards slowed, resulting in a relatively quiet market overall. Steel mills remain profitable, and the willingness for blast furnace maintenance is weak in the short term, keeping pig iron production at a high level, which provides some support for iron ore concentrate demand. However, steel mills are cautious in purchasing, mainly purchasing as needed, and demand-driven support is not significant.

The price of iron ore concentrate in west Liaoning dropped significantly, with the ex-factory price of 66-grade wet basis tax-excluded falling by 30-40 yuan/mt, currently at 710-720 yuan/mt. Production enthusiasm at mines and beneficiation plants remains moderate, but the wait-and-see sentiment is strong. In-plant inventory at steel mills remains low, and purchasing is mainly as needed, resulting in a relatively quiet market overall. With the end of the heating season, steel mills are expected to undergo maintenance gradually, leading to weakened demand and reduced support for iron ore prices. However, considering the recent weakening of tariff impacts, market pessimism has eased.

Mines and beneficiation plants in east China are operating normally, producing and selling without significant inventory pressure. A large mine in Linyi, Shandong partially resumed production this week, with a daily increase in iron ore concentrate of around 3,000 mt, alleviating the tight supply in the local area.

Looking ahead to next week

For imported ore: The iron ore market is expected to maintain a strong and fluctuating pattern. On the demand side, daily pig iron production is expected to increase significantly by nearly 20,000 mt, approaching the annual peak, supporting ore demand. On the supply side, although shipments may drop slightly due to stormy weather in Australia, the overall disruption is limited. Although the impact of the China-US tariff war has weakened marginally, its ongoing suppression effect remains. Coupled with rising market expectations for policies from the late April Politburo meeting, bullish and bearish factors are intertwined. Iron ore prices are expected to continue fluctuating upward, but the upside may be relatively limited due to policy uncertainty and high prices.

For domestic ore: Overall, domestic ore prices are adjusting, with some purchasing steel mills raising prices while others remain stable. The wait-and-see sentiment persists, and without policy guidance, sustained upward momentum is lacking. However, considering the tight resources, the bottom support remains strong, and domestic ore prices are expected to remain in the doldrums next week.

Click to view the SMM Metal Industry Chain Database

![Before the holiday, the black chain is unlikely to see a trend-driven market [SMM Steel Industry Chain Weekly Report].](https://imgqn.smm.cn/usercenter/zUFfM20251217171748.jpg)

![[SMM Chromium Daily Review] Inquiries and Transactions Weakened, Chromium Market Showed Mediocre Performance Before the Holiday](https://imgqn.smm.cn/usercenter/ENDOs20251217171718.jpg)