Futures market: LME copper opened at $9,133/mt overnight, hitting a high of $9,279.5/mt and a low of $9,111/mt, and closed at $9,253/mt (previous close: $9,190.2/mt, up 0.68%). The overall trend showed initial fluctuations followed by a significant rise. Open interest stood at 282,849 lots. SHFE copper 2506 contract opened at 75,800 yuan/mt overnight, reaching a high of 76,250 yuan/mt and a low of 75,550 yuan/mt, with the latest price at 76,070 yuan/mt (up 230 yuan/mt, or 0.30%, from the previous close). The overall trend exhibited initial downward fluctuations followed by a significant rise. Trading volume was 46,735 lots, open interest was 159,208 lots, and daily open interest decreased by 2,901 lots (down 1.79%).

[SMM Copper Morning Meeting Summary] News: (1) The latest developments in tariffs between the EU, Japan, and the US have impacted the market, with US President Trump and Treasury Secretary Besant making statements, causing fluctuations in US stocks and the foreign exchange market, and a surge in oil prices.

(2) Italian Prime Minister Meloni arrived at the White House to meet with US President Trump. Trump stated that he is "100%" confident of reaching a trade agreement with the EU before the end of the 90-day tariff suspension period.

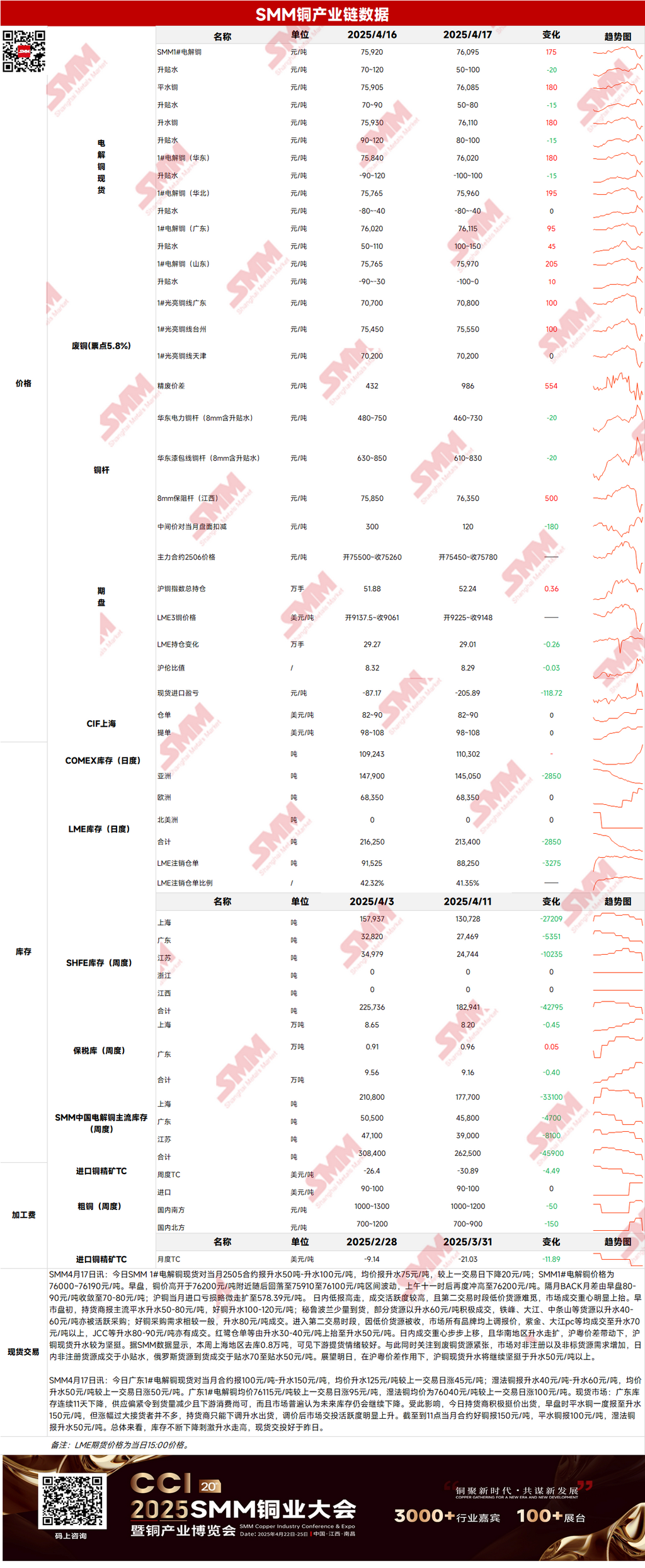

Spot market: (1) Shanghai: On April 17, SMM #1 copper cathode spot prices against the front-month 2505 contract were at a premium of 50-100 yuan/mt, with an average premium of 75 yuan/mt, down 20 yuan/mt from the previous day. According to SMM data, Shanghai destocked 8,000 mt this week, indicating strong downstream cargo pick-up sentiment. Meanwhile, tight supply of copper scrap has been noted, with increased demand for non-registered and non-standard sources. Non-registered sources traded at a small discount, while Russian sources traded at a discount of 70-50 yuan/mt. Looking ahead, under the influence of the Shanghai-Guangdong price spread, Shanghai spot copper premiums are expected to remain firm above 50 yuan/mt.

(2) Guangdong: On April 17, Guangdong #1 copper cathode spot prices against the front-month contract were at a premium of 100-150 yuan/mt, with an average premium of 125 yuan/mt, up 45 yuan/mt from the previous day. Overall, declining inventories have driven premiums higher, and spot trades were better than the previous day.

(3) Imported copper: On April 17, warrant prices were at $82-90/mt, QP May, with the average price unchanged from the previous day; B/L prices were at $98-108/mt, QP May, with the average price unchanged from the previous day. EQ copper (CIF B/L) was at $55-65/mt, QP May, with the average price unchanged from the previous day, referencing cargoes arriving in mid-to-late April. Overall, the market remained consistent with the previous period, and sellers are optimistic about a widening SHFE/LME price ratio in the future.

(4) Secondary copper: On April 17, secondary copper raw material prices rose 100 yuan/mt MoM. Guangdong bare bright copper prices were at 70,700-70,900 yuan/mt, up 100 yuan/mt from the previous day. The price difference between copper cathode and copper scrap was 986 yuan/mt, up 554 yuan/mt MoM. The price difference between copper cathode rod and secondary copper rod was 475 yuan/mt. According to the SMM survey, secondary copper rod enterprises had limited raw material procurement this week, leading to a significant decline in production. As the delivery dates for pending orders approach, some secondary copper rod enterprises have been forced to purchase copper cathode to produce secondary copper rods to fulfill orders.

(5) Inventories: On April 17, LME copper inventories decreased by 2,850 mt to 213,400 mt; on April 17, SHFE warrant inventories decreased by 24,220 mt to 77,124 mt.

Prices: On the macro front, the European Central Bank cut interest rates by 25 basis points as expected, marking the seventh rate cut in the past year, with the decision unanimously approved, and the US dollar index stabilized. Trump expressed confidence in reaching a trade agreement with the EU but is in no rush to finalize it; if negotiations fail, the EU is reportedly considering export restrictions against the US. The US Treasury Secretary also stated that negotiations with Japan are progressing very satisfactorily, and the advancement of trade agreements pushed up copper prices overnight. On the fundamental side, overall market trading activity was strong, and with premiums expanding in South China, driven by the Shanghai-Guangdong price spread, Shanghai spot copper premiums remained firm, with tight supply of low-priced sources. As of Thursday, April 17, SMM copper inventories in mainstream regions across China decreased by 17,100 mt from Monday to 233,400 mt, down 33,800 mt from the previous Thursday, marking the seventh consecutive week of destocking. Inventories have now fallen by 143,600 mt from the year's high and are 170,100 mt lower than the 403,500 mt recorded YoY. Overall, copper prices are expected to stabilize today as trade concerns ease.

》Click to view the SMM Metals Database

[The above information is based on market collection and comprehensive evaluation by the SMM research team. The information provided in this article is for reference only. This article does not constitute direct advice for investment research decisions. Clients should make decisions cautiously and not use this as a substitute for independent judgment. Any decisions made by clients are unrelated to SMM.]