》View SMM lead product quotes, data, and market analysis

》Order and view SMM metal spot historical prices

》Click to view the SMM database

SMM April 17th News:

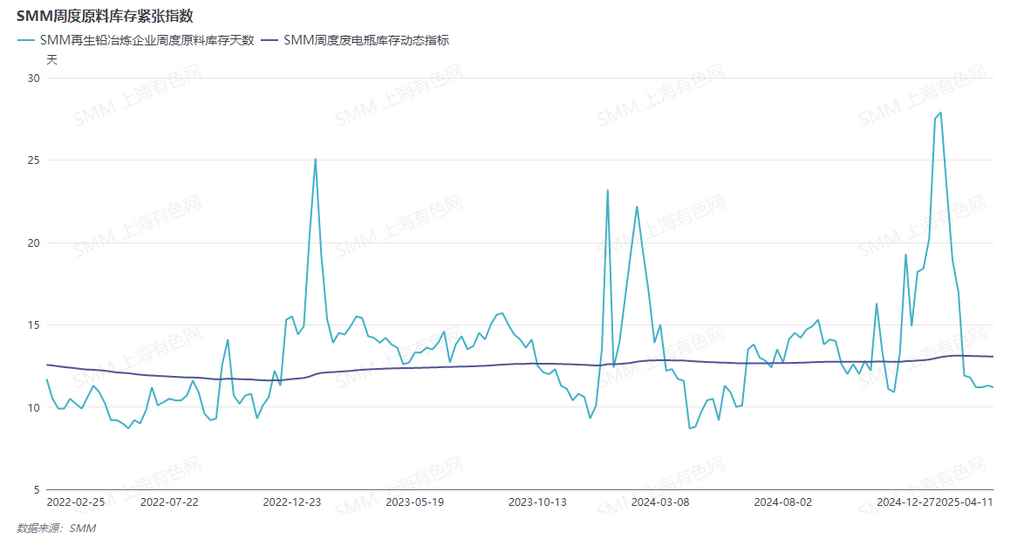

April remains the traditional consumption off-season for lead-acid batteries, while the scrap volume of waste lead-acid batteries is low, leading to tight market supply. A smelter in the main production area of secondary lead stated that the procurement price has been raised twice this week, but the arrivals were only two trucks. The SMM weekly raw material inventory tightness index shows that the days of raw material inventories for secondary lead smelters are about two days below the dynamic average.

However, secondary lead smelters have not shown a widespread willingness to actively cut production, with only individual smelters in Jiangxi, Anhui, Zhejiang, and Hebei experiencing a slight decline in production two weeks ago. Some companies indicated that production cuts would lead to increased production costs, while shutdowns would directly result in labor cost losses.

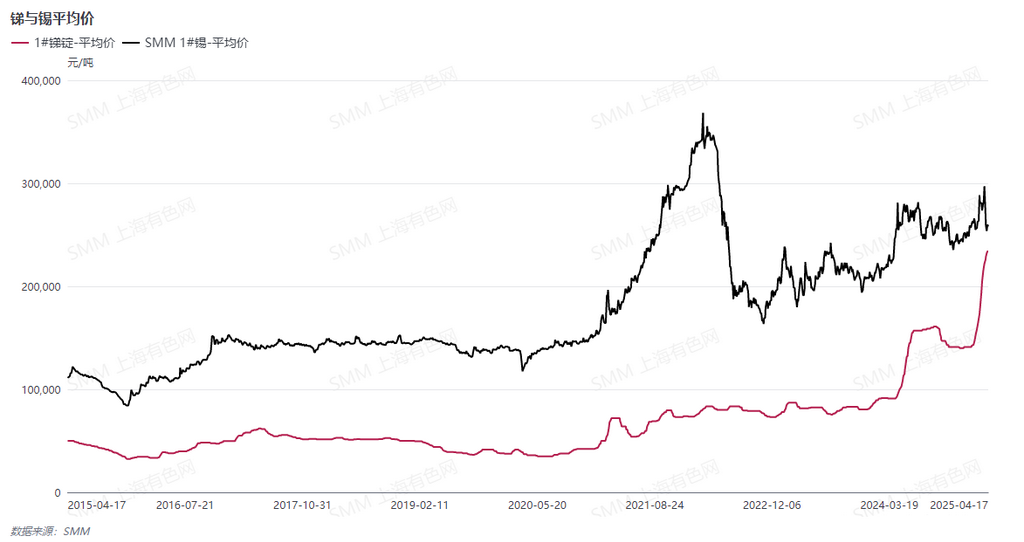

Additionally, the prices of metals such as antimony and tin have remained firm recently. Secondary lead smelters with comprehensive multi-metal recovery projects stated that the current by-product revenue can barely offset the pressure caused by losses in lead smelting. If lead prices continue to decline and the price of raw material scrap batteries rises further, leading to expanded losses, and by-product revenue can no longer cover the losses, they will consider production cuts or shutdowns for maintenance.

As the Labour Day holiday approaches, although downstream battery producers have expectations for pre-holiday stockpiling, the market is relatively pessimistic about their stockpiling efforts. In previous years, lead-acid battery producers generally took 2-3 days off during the Qingming Festival holiday, but this year, they commonly took 5-7 days off. Some companies that took holidays have not yet resumed normal production. SMM learned that many downstream lead-acid battery producers have expectations for production cuts during this Labour Day holiday. Smelters in South China, in particular, stated that some of their downstream customers will take at least 7 days off. If many downstream companies take holidays, it will inevitably affect the production enthusiasm of smelters.

In summary, although secondary lead smelters have not shown widespread active production cuts, the tight supply of raw materials, combined with the pressure of losses and the potential inventory buildup of finished products after downstream companies take holidays, may prompt secondary lead smelters to passively reduce production. As both supply and demand for lead ingots are expected to decline, short-term lead prices may remain under pressure, with little support from fundamentals for a significant rebound.