SMM April 1 News: On the afternoon of March 28, a 7.9-magnitude earthquake occurred in Sagaing, Myanmar, approximately 294 kilometers from the Chinese border. Parts of China subsequently experienced tremors and aftershocks. As a result, some crystal pulling bases in Yunnan and Sichuan were affected by line breaks, furnace sealing, and even furnace explosions, with Yunnan being particularly severely impacted.

SMM learned from the market that almost all bases in Yunnan suffered certain losses, including several first-tier and second-tier crystal pulling enterprises. The impact in Yibin and Leshan, Sichuan, was relatively mild, and production had basically resumed by the time of reporting. Although occasional line breaks occurred in other individual areas, the impact was almost negligible.

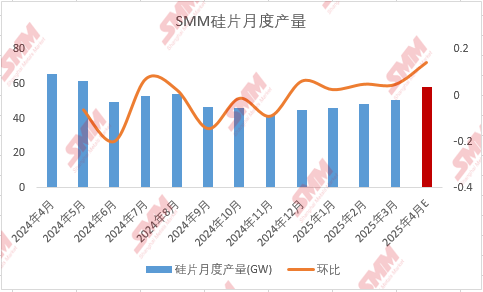

Since the earthquake occurred at the end of March, SMM's summary indicates that the earthquake affected crystal pulling production by approximately 1.8GW-2.2GW in March, with the wafer production schedule slightly lower than before. The neutral estimate for the impact on April's wafer production schedule is around 3-3.4GW, and the April wafer production schedule has dropped from over 60GW to below 60GW.

From local production insights, although the maintenance time cost for sealed and exploded furnaces is high (usually requiring 10 days or even more than half a month), many bases have ample idle equipment. As the recent period is the final shipping window before May 31, multiple bases with sufficient auxiliary materials and idle furnaces chose to repair damaged equipment while restarting new furnaces, achieving "capacity replacement" to minimize losses. However, some bases reported that a 4.4-magnitude aftershock occurred in Yunnan on March 30, and due to concerns about potential secondary damage from further aftershocks, they opted to delay resuming production for a few days. Considering the above factors, the estimated reduction in April's production schedule is around 3-3.4GW, and polysilicon demand is also expected to decrease.

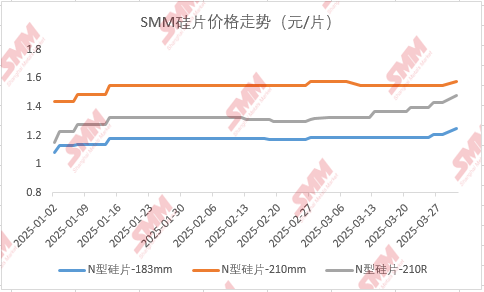

Affected by this event and the previously tight wafer supply, some top-tier enterprises in China raised wafer prices again on March 31, with prices for 183mm, 210R, and 210mm reaching 1.23 yuan, 1.55 yuan, and 1.6 yuan, respectively.

Regarding the future market, SMM believes that there is still some opportunity in the early to mid-April market, but the space is relatively small. Compared to module scheduled production, cells and wafers still have a destocking trend to support prices. However, as the window period is about to end, the market sentiment is gradually shifting from stopping rising to bearish, with weak demand expected in the latter half of May and Q3. Many enterprises reported a significant decline in orders, and prices are likely to fall.

》View SMM PV Industry Chain Database

![[SMM PV News] Armenia Hits 1.1 GW Solar Capacity,](https://imgqn.smm.cn/usercenter/qQwIB20251217171741.jpg)

![Spot Market and Domestic Inventory Brief Review (February 5, 2026) [SMM Silver Market Weekly Review]](https://imgqn.smm.cn/usercenter/tSwaX20251217171735.jpg)