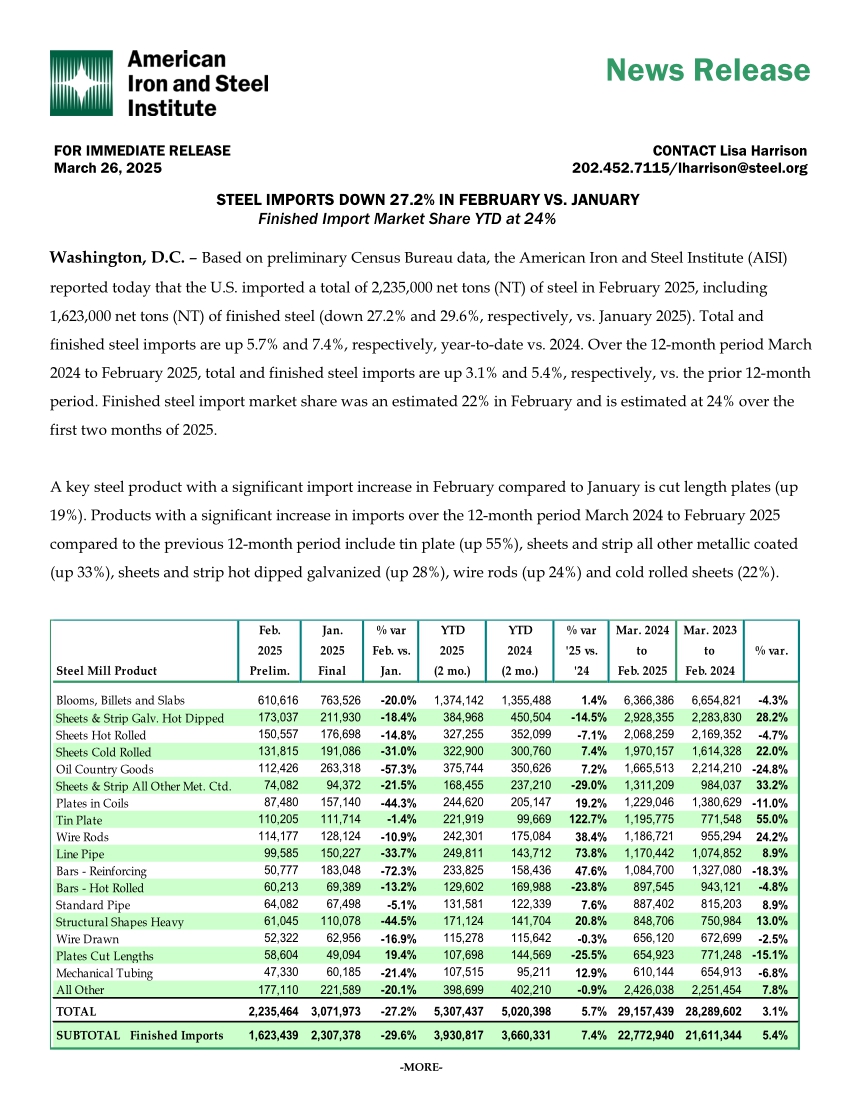

Aftermath of US Tariff Blast: 27% of Steel Imports Evaporated in February!

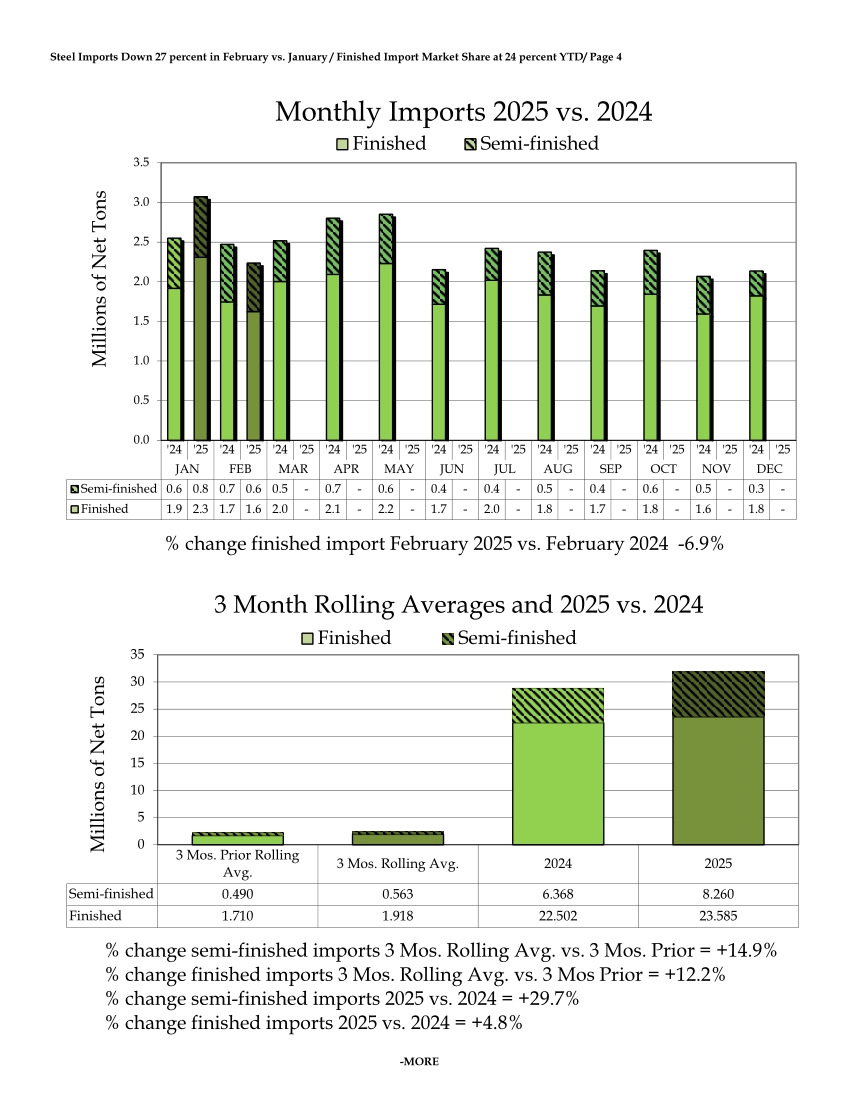

According to preliminary data from the US Census Bureau, the American Iron and Steel Institute (AISI) reported today thatthe total steel imports in the US in February 2025 reached 2.235 million net tons, with finished steel products accounting for 1.623 million net tons (a decrease of 27.2% and 29.6%, respectively, compared to January 2025).Year-to-date, total steel imports and finished steel imports increased by 5.7% and 7.4%, respectively, compared to the same period in 2024. Over the 12 months from March 2024 to February 2025, total steel imports and finished steel imports increased by 3.1% and 5.4%, respectively, compared to the previous 12 months.The estimated market share of finished steel imports in February was 22%, while the estimated share for the first two months of 2025 was 24%.

- By product category,

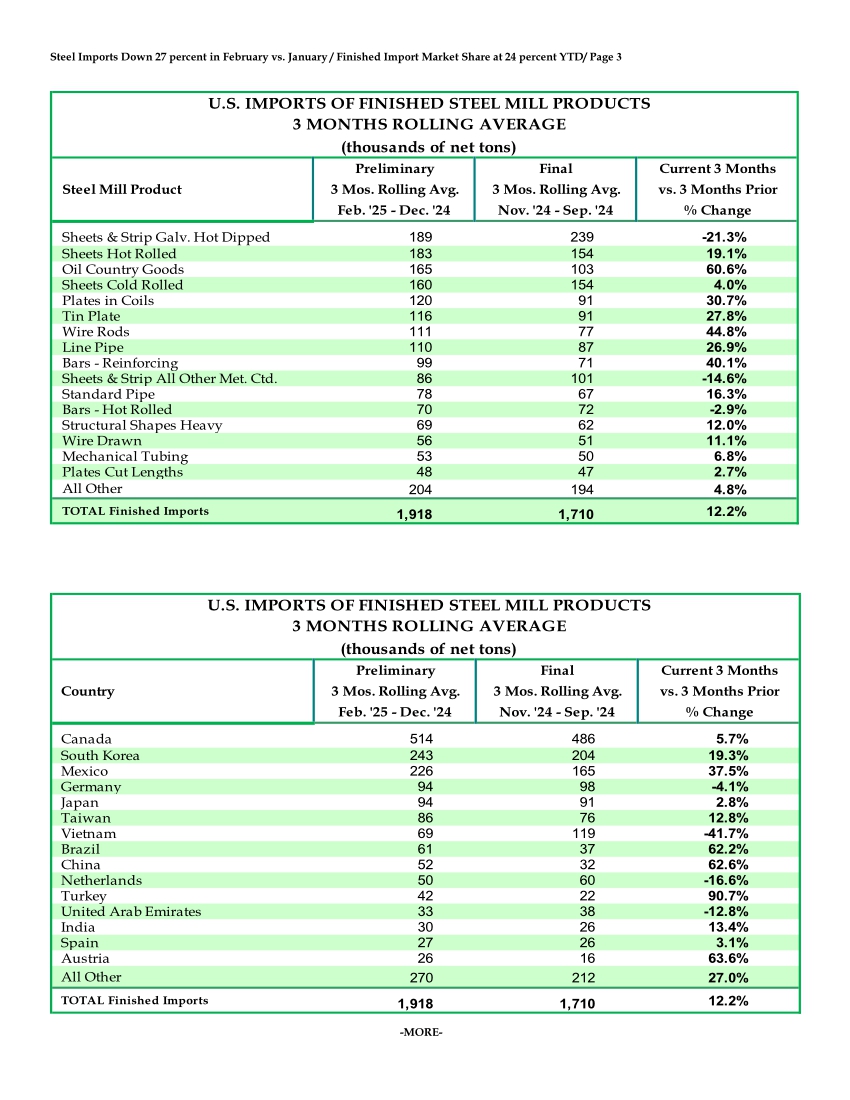

compared to January, steel products with significant import growth in February included cut-to-length plates (up 19%). From March 2024 to February 2025, products with significant import growth compared to the previous 12 months included tinplate (up 55%), other metallic coated sheets and strips (up 33%), hot-dip galvanized sheets and strips (up 28%), wire rods (up 24%), and cold-rolled sheets (up 22%).

- By import source,

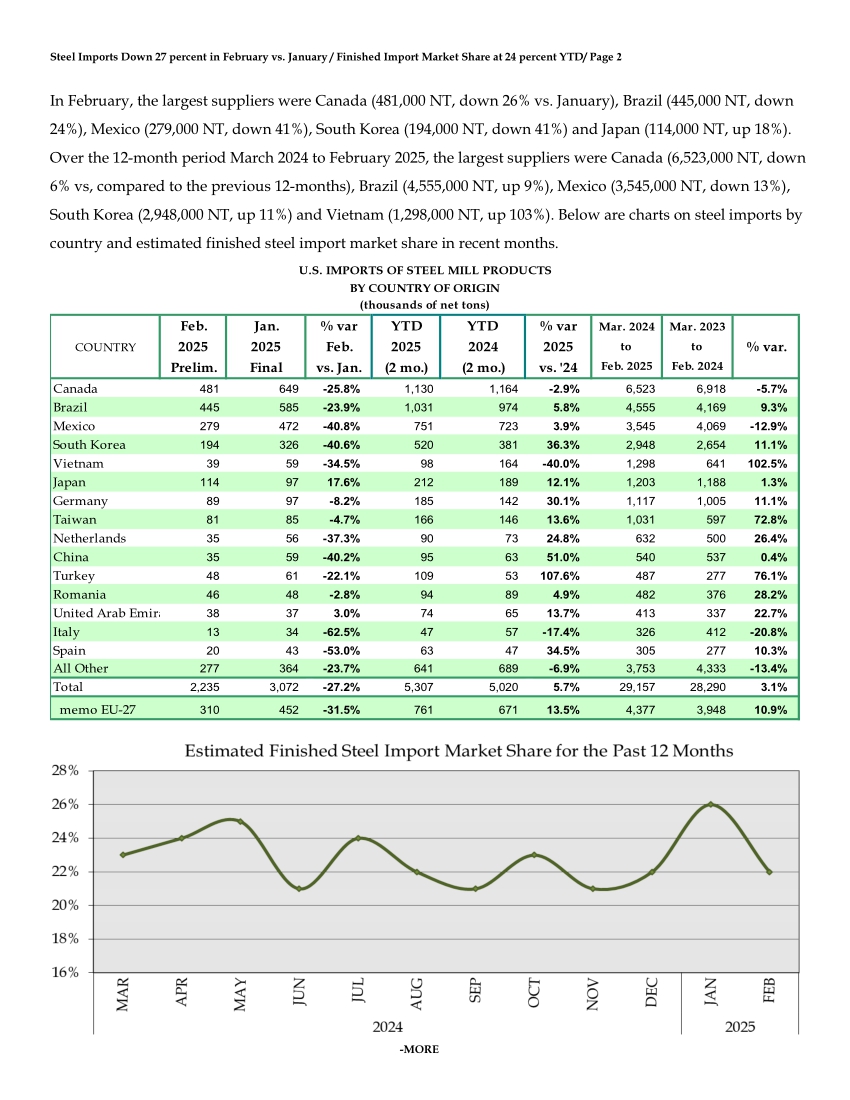

in February, the largest suppliers were Canada (481,000 net tons, down 26% from January), Brazil (445,000 net tons, down 24%), Mexico (279,000 net tons, down 41%), South Korea (194,000 net tons, down 41%), and Japan (114,000 net tons, up 18%).

Over the 12 months from March 2024 to February 2025, the largest suppliers were Canada (6,523,000 net tons, down 6% compared to the previous 12 months), Brazil (4,555,000 net tons, up 9%), Mexico (3,545,000 net tons, down 13%), South Korea (2,948,000 net tons, up 11%), and Vietnam (1,298,000 net tons, up 103%).

- Tariff Policy Marks a Turning Point for US Steel Imports in January-February

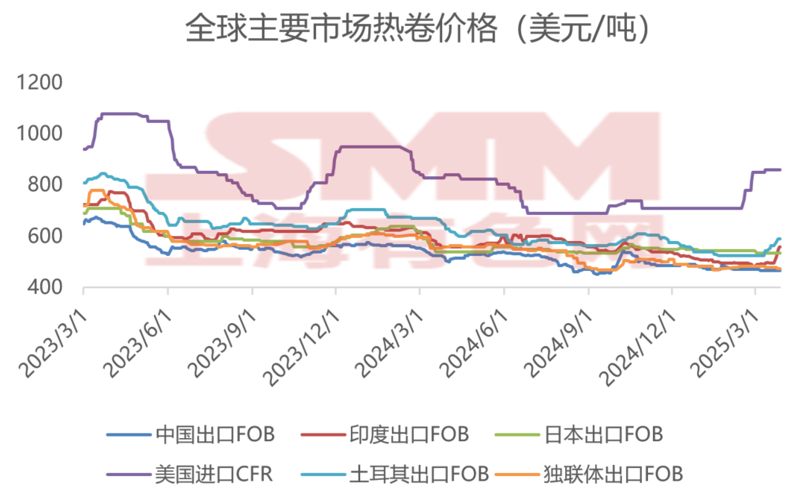

Since US President Trump announced on February 10 a 25% tariff on all steel and aluminum imports to the US, and the cancellation of tariff-free quotas and exemptions for some trading partners, effective from March 12, 2025, US steel import prices have continued to rise, with the current CFR price for HRC imports reaching as high as $860/mt. Although the cumulative steel imports in the US in January-February still showed YoY growth, the sharp decline in February steel imports indicates that the initial surge was largely due to countries rushing to export, significantly boosting steel imports. As more US tariff regulations are enacted, steel imports are expected to continue to pull back, with January imports likely to be the peak for 2025.

![The most-traded BC copper contract closed down 2.85%, as speculative fervor cooled, weighing on copper prices [SMM BC Copper Review]](https://imgqn.smm.cn/usercenter/CYktX20251217171711.jpg)

![The Black Industrial Chain Lacked Upward or Downward Momentum Before the Holiday [SMM Steel Industry Chain Weekly Report]](https://imgqn.smm.cn/usercenter/FRcmT20251217171746.jpg)

![The most-traded SHFE tin contract plummeted more than 8% in a single day, and tin prices are expected to remain in the doldrums in the short term [SMM Tin Futures Review]](https://imgqn.smm.cn/usercenter/LLUUJ20251217171751.jpeg)