April 1,

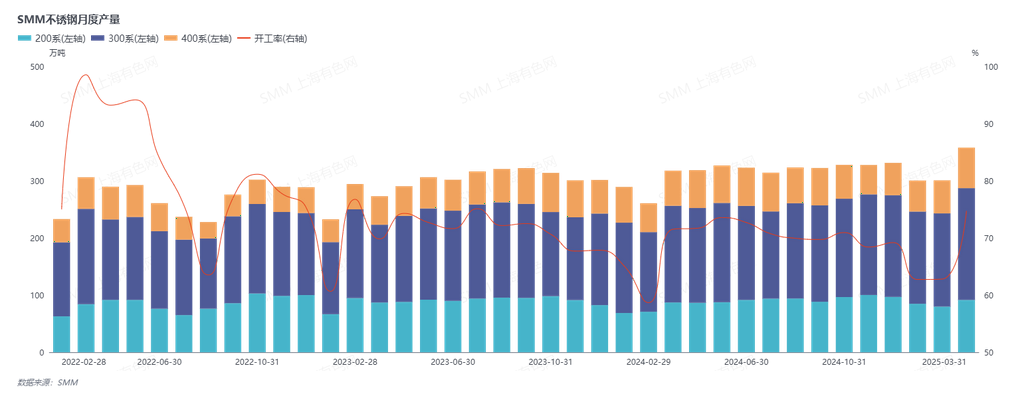

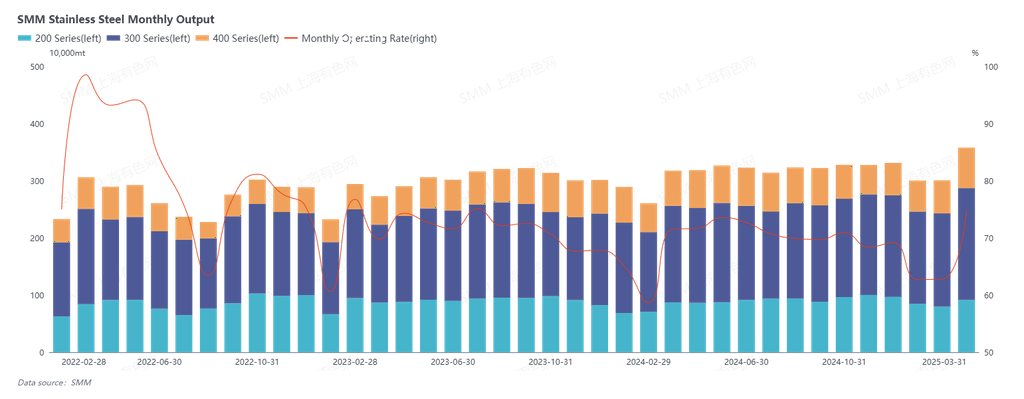

According to SMM data, domestic crude stainless steel production in March 2025 saw a significant increase, with total production up 19.02% MoM and a notable 12.67% YoY growth. By product series, the production of 200-series, 300-series, and 400-series stainless steel rose sharply by 14.64%, 19.89%, and 22.63% MoM, respectively.

The market supply was ample in March. On one hand, the industry had high expectations for the traditional peak demand season of "Golden March and Silver April," which greatly stimulated the production enthusiasm of stainless steel producers. On the other hand, raw material prices remained high for a long time, solidifying the production costs of stainless steel. Under these dual effects, steel mills and spot merchants raised prices, attempting to pass on cost pressures downstream. However, the reality was that downstream demand in March fell far short of expectations, with new orders being scarce. Downstream enterprises only maintained essential restocking operations, unable to drive prices significantly higher. Even though stainless steel prices rose slightly in March, the overall shipment pace remained slow, and inventories stayed high, making the market's oversupply characteristics increasingly evident.

Entering April, some stainless steel producers initiated equipment upgrades and maintenance due to environmental protection emission policy requirements, which affected production to some extent. However, as stainless steel prices continued to rise, the loss situation of enterprises was effectively alleviated, with some even achieving profitability, keeping production enthusiasm at a high level. Notably, as downstream inventories gradually deplete, the previously sluggish demand is expected to improve, and market demand may see growth opportunities in April.

Overall, stainless steel production in April is expected to show a slight decline, down 0.61% MoM, but still maintaining an 11.87% YoY growth. By product series, 200-series production will see a slight increase of 3.17% MoM, while 300-series and 400-series production will decline by 1.89% and 1.98% MoM, respectively.

SMM Analysis: In March 2025, domestic crude stainless steel production hit a new high. However, downstream market demand failed to interact well with the supply side, with new orders being scarce. Downstream enterprises only responded with essential restocking, leading to a lack of demand support for price increases, slow overall shipment speeds, and increasingly severe inventory accumulation. This indicates a prominent supply-demand imbalance in the stainless steel market in March. In April, environmental protection emission policies prompted some stainless steel producers to carry out equipment upgrades and maintenance, which to some extent suppressed production growth. Destocking and standing firm on quotes may be the themes of April.