》View SMM Lead Product Quotes, Data, and Market Analysis

》Order and View SMM Metal Spot Historical Prices

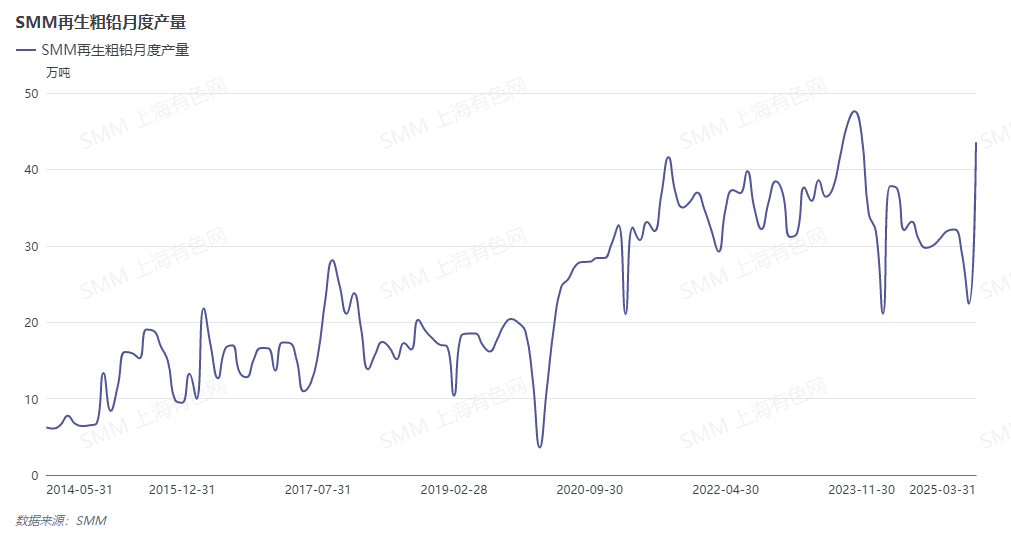

SMM March 31 News:

In March 2025, the production of secondary crude lead increased significantly, up 94.34% MoM and 15.21% YoY. The production of secondary refined lead rose 110.48% MoM and 11.24% YoY.

The price center of lead in March moved significantly higher compared to February, bringing spring-like profits to secondary lead smelters. Smelters showed high production enthusiasm during the month, with most increasing output compared to February. Additionally, new secondary lead capacity of approximately 500,000 mt/year was added in Jiangsu and Guizhou. The new smelter in Jiangsu started normal production in March, while Guizhou began small-scale feeding in March, with full production planned for early April. Large smelters in Zhejiang, Anhui, Hunan, and Ningxia, which had undergone maintenance earlier, resumed and stabilized production in March. Several medium and large smelters in Jiangxi, Hubei, Shanxi, and Inner Mongolia restarted production in late February and contributed significantly to output in March. A small number of smelters saw slight production declines due to environmental protection inspections, control measures, and tight raw material inventories. In summary, secondary lead production surged in March due to strong operating profits, new capacity additions, and the resumption and ramp-up of medium and large smelters, reaching a new high in nearly 1.5 years.

Entering April, new capacity still has plans to increase production. Although most secondary lead smelters expect tight raw material supply in April, they have not mentioned any active production cut plans. Data suggests that secondary lead production in April will be basically flat compared to March.

SMM experience reminds that April is the traditional consumption off-season for lead-acid batteries. If downstream battery producers show weak willingness to purchase lead ingots, and the scrap battery market sees low scrap volumes combined with high operating rates of secondary lead, leading to increased sentiment among recyclers to hold back cargoes, there may be expectations for passive production cuts by secondary lead smelters in mid to late April.