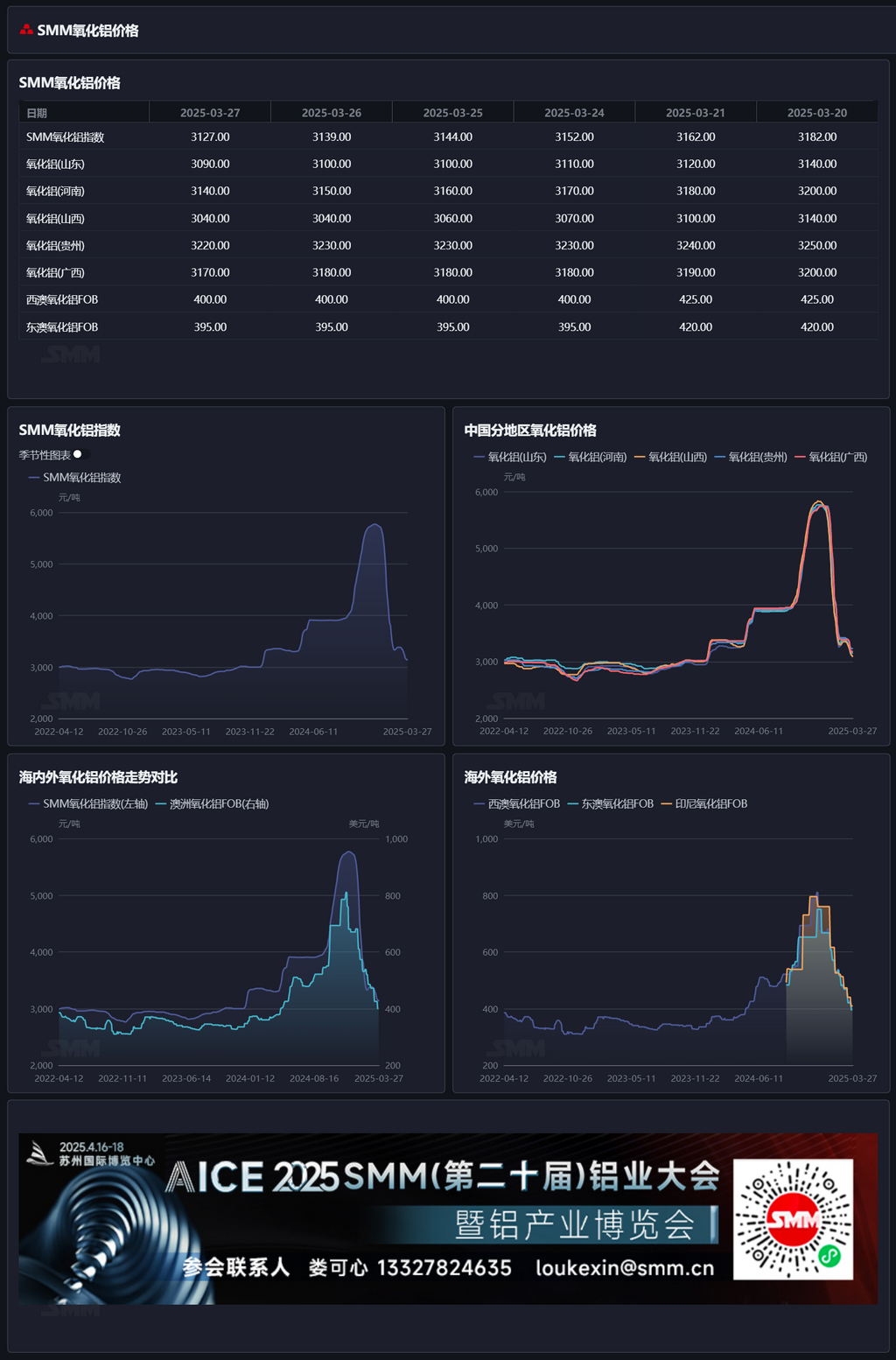

SMM Alumina Morning Comment 3.31

Futures market: In the night session, the most-traded alumina 2505 contract opened at 3,035 yuan/mt, with a high of 3,037 yuan/mt, a low of 2,992 yuan/mt, and closed at 2,997 yuan/mt, down 38 yuan/mt, a decrease of 1.25%, with an open interest of 205,000 lots.

Ore side: As of March 28, the SMM imported bauxite index stood at $93.1/mt, down $0.06/mt from the previous trading day, mainly due to the decline in caustic soda prices in Shandong. The SMM Guinea bauxite CIF average price was $91/mt, flat from the previous trading day. The SMM Australia low-temperature bauxite CIF average price was $87/mt, flat from the previous trading day. The SMM Australia high-temperature bauxite CIF average price was $81/mt, flat from the previous trading day.

Industry news:

- On March 28, the Ministry of Industry and Information Technology and nine other departments issued the "Implementation Plan for High-Quality Development of the Aluminum Industry (2025-2027)". The plan mentioned accelerating the increase in domestic bauxite resource reserves and production. It promotes a new round of strategic actions for mineral exploration breakthroughs, adding a batch of exploitable bauxite resources, and encourages technological breakthroughs in the development and utilization of low-grade and high-sulfur bauxite. The plan also mentioned the need to cautiously construct alumina projects. New or expanded alumina projects must meet the advanced mandatory energy consumption limit standards and environmental performance level A. No new or expanded alumina production lines using diaspore as raw material will be built. In principle, new or expanded alumina projects (including those producing aluminum hydroxide from bauxite) must have bauxite production rights matching the capacity and a certain comprehensive utilization capacity of red mud.

- According to SMM data, in March 2025, the total bauxite raw material inventory of domestic alumina refineries was basically flat, up 0.1% MoM, but down 0.5% YoY. As of March 28, SMM statistics showed that the total bauxite inventory at nine ports was 16.06 million mt, with port bauxite inventory increasing by 1.5 million mt from the end of last month, mainly due to increased imported bauxite supply.

- Monthly alumina production dynamics: According to SMM data, in March 2025 (31 days), China's metallurgical-grade alumina production increased by 8.86% MoM and 11.32% YoY. By the end of March, China's metallurgical-grade alumina existing capacity was around 105.02 million mt, with actual operating capacity down 1.68% MoM, and the operating rate at 84.64%.

- According to SMM, the mainstream alumina refineries in Guangxi Province lowered their caustic soda procurement prices by 700 yuan/mt (converted to 100% concentration) in April compared to March, with the delivery-to-factory price of 50% ion-exchange membrane liquid caustic soda at around 3,600 yuan/mt (converted to 100% concentration), with slight differences in some regions due to varying transportation distances.

Basis daily report: According to SMM data, on March 28, the SMM alumina index was at a premium of 75 yuan/mt against the most-traded contract's latest transaction price at 11:30.

Warrant daily report: On March 28, the total registered alumina warrants increased by 15,626 mt from the previous trading day to 298,500 mt. The total registered alumina warrants in Shandong remained flat at 4,513 mt from the previous trading day. The total registered alumina warrants in Henan remained flat at 25,800 mt from the previous trading day. The total registered alumina warrants in Guangxi remained flat at 49,800 mt from the previous trading day. The total registered alumina warrants in Gansu remained flat at 22,500 mt from the previous trading day. The total registered alumina warrants in Xinjiang increased by 15,626 mt from the previous trading day to 195,800 mt.

Overseas market: As of March 28, 2025, the FOB alumina price in Western Australia was $377/mt, with an ocean freight rate of $21.40/mt, and the USD/CNY exchange rate selling price was around 7.28. This price translates to a selling price of around 3,358 yuan/mt at domestic mainstream ports, which is 247 yuan/mt higher than domestic alumina prices, keeping the alumina import window closed. Based on the latest FOB transaction price of $368/mt in Eastern Australia, the estimated selling price at domestic mainstream ports is around 3,300 yuan/mt, less than 200 yuan/mt higher than the SMM alumina price index. If overseas alumina prices further decrease and the rate of decrease exceeds that of domestic prices, the alumina import window may gradually open. On the export side, based on the latest spot transaction prices of alumina in Shandong, the domestic alumina export cost is around $450/mt, higher than overseas spot alumina prices, keeping the export window closed.

Summary: Last week, the weekly operating rate of alumina was lowered again, with the national total operating capacity of metallurgical alumina decreasing to 87.3 million mt/year, down 700,000 mt/year WoW, but the overall supply surplus in the alumina market has not yet reversed. According to SMM data, as of last Thursday, the total operating capacity of domestic aluminum was 43.88 million mt/year, translating to an alumina demand operating capacity of around 84.47 million mt/year, with theoretical demand increasing slightly but still below actual operating levels. On the supply side, domestic bauxite supply remains low, with limited increments; increased imported bauxite supply has driven the total domestic bauxite supply, potentially making the bauxite supply and demand fundamentals more relaxed than before, with bauxite prices likely to remain under pressure in the short term. Meanwhile, downstream aluminum plants reported that alumina procurement is mainly based on long-term contracts, and some plants that have stockpiled for winter are planning to actively reduce inventory. Last week, according to SMM statistics, alumina raw material inventory at aluminum plants decreased by 44,000 mt WoW. In the short term, alumina circulating supply is expected to remain relatively loose, and alumina prices may continue to operate under pressure. Subsequent attention should be paid to changes in alumina operating capacity.

[The information provided is for reference only. This article does not constitute direct advice for investment research decisions. Clients should make decisions cautiously and not use this as a substitute for independent judgment. Any decisions made by clients are unrelated to SMM.]

![East China Market Activity Declined, Central China Purchasing Sentiment Was Poor [SMM Spot Aluminum Midday Review]](https://imgqn.smm.cn/usercenter/XfCZS20251217171655.jpg)