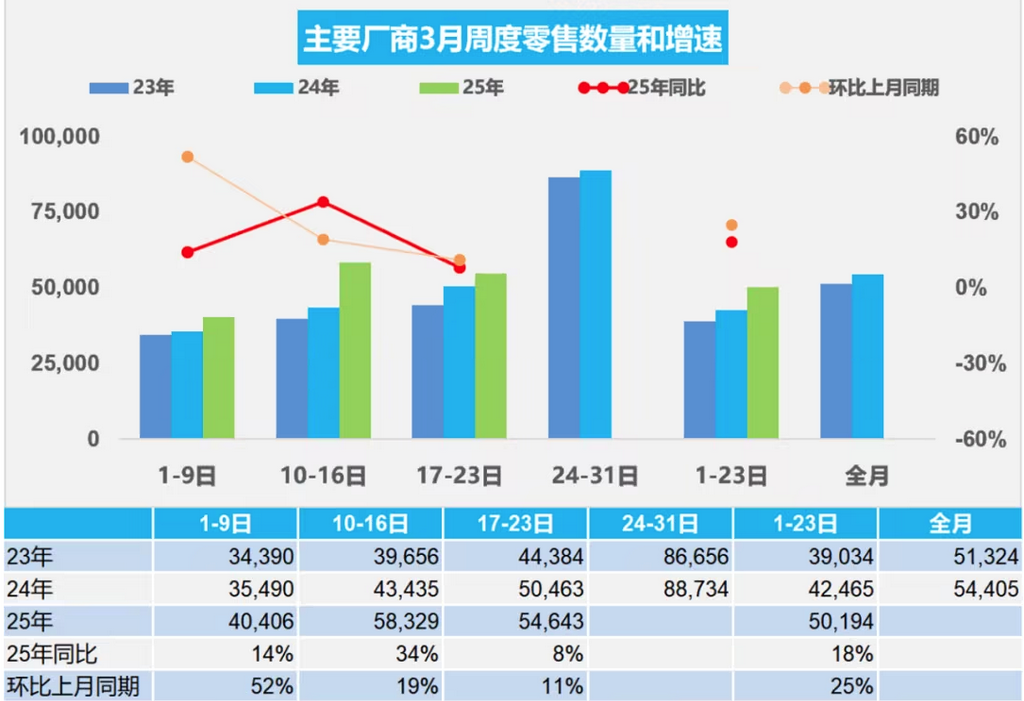

According to the latest weekly data released by the CPCA (China Passenger Car Association), the national passenger car market's daily average retail sales reached 55,000 units in the third week of March 2025 (March 17-23), up 8% YoY and 11% MoM. Although this growth rate has slowed compared to the previous two weeks, it still continues the mild recovery trend of the post-holiday car market. In terms of cumulative data, the national passenger car retail sales from March 1 to 23 reached 1.154 million units, up 18% YoY and 25% MoM, indicating strong resilience in overall market demand.

From the perspective of market drivers, the continuous efforts of the stimulus policy package remain the core support. The "program of large-scale equipment upgrades and consumer goods trade-ins" policy (NEV promotion and trade-in) launched by the central and local governments has created a superimposed effect, especially the early implementation of the trade-in policy, which has effectively stimulated demand for unit vehicles and private consumption. Meanwhile, the low prices of raw materials such as lithium carbonate have provided automakers with room to optimize the cost structure of NEV models, further accelerating product iteration. Data shows that NEV retail sales from March 1 to 23 reached 622,000 units, up 30% YoY, with the penetration rate expected to rebound to 54.1%, becoming the main engine driving market growth.

Producer strategies show significant differentiation, with leading producers (accounting for over 80% of market share) increasing their March retail targets by 8.5% YoY, mainly by increasing discounts to maintain competitiveness. The overall car market discount rate remained stable at 23.4% in mid-March, basically flat with month-end February, but some brands are competing for market share through diversified promotional methods such as limited-time offers and financial subsidies. The intensive launch of new models has also boosted market heat, with the daily average wholesale volume in the third week reaching 64,000 units, up 1% YoY, reflecting producers' confidence in stockpiling for the subsequent market.

Notably, the daily average retail sales in the fourth week (March 24-31) are expected to reach 79,800 units, although a 10.1% YoY pullback is possible, mainly due to the high base in the same period last year. Based on the full-month data, the CPCA maintains its forecast of 1.85 million units for March's narrow passenger car retail sales, up 9.1% YoY and over 30% MoM. This performance not only benefits from the release of policy dividends and the natural recovery of post-holiday demand but also reflects the resilience of the automotive industry as an economic pillar.

SMM NEV Industry Research Department

Cong Wang 021-51666838

Rui Ma 021-51595780

Disheng Feng 021-51666714

Yanlin Lu 021-20707875

Zhicheng Zhou 021-51666711

Haohan Zhang 021-51666752

Zihan Wang 021-51666914

Jie Wang 021-51595902

Yang Xu 021-51666760

Bolin Chen 021-51666836