1. According to the SMM survey, the profit per ton of coke this week was 1.3 yuan/mt, with most coke enterprises operating near the break-even line.

From a price perspective, coke prices remained stable this week, and the profit per ton of coke was not affected by price changes. From a cost perspective, coal mines have been operating normally recently, coking coal supply has remained stable, and steel mill sales have improved, gradually resuming production. The sentiment to suppress raw material prices has decreased, purchase enthusiasm has increased, online auctions have seen more gains than losses, and the market transaction atmosphere has improved, keeping coking costs stable.

Next week, most market participants expect coke prices to remain stable, with the market transaction atmosphere warming up, online auctions showing more gains than losses, and coking costs remaining stable. Most coke enterprises are likely to continue operating near the break-even line.

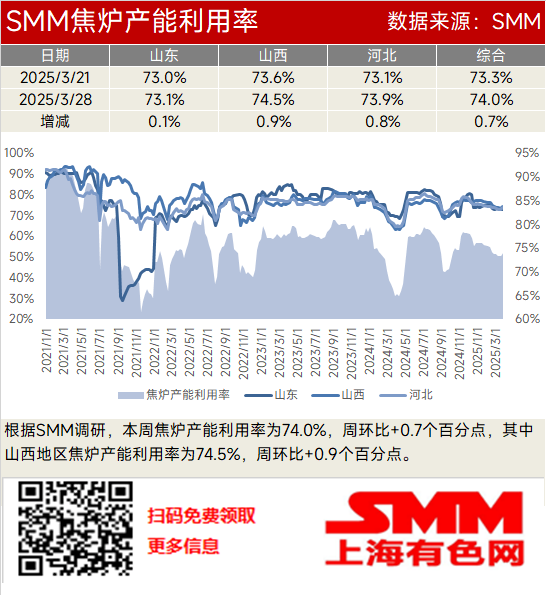

2. According to the SMM survey, the coke oven capacity utilization rate this week was 74.0%, up 0.7 percentage points WoW, with the rate in Shanxi at 74.5%, up 0.9 percentage points WoW.

From a profitability perspective, most coke enterprises are either at break-even or slightly in the red, which has a relatively small impact on production. From an inventory perspective, coke enterprises have seen improved shipments, downstream purchase enthusiasm has increased, and overall coke inventory has continued to decline, positively affecting production enthusiasm.

In the near future, the profitability of most coke enterprises is likely to remain within an acceptable range, and their inventory pressure has eased, boosting production enthusiasm. Coke supply may increase slightly. Meanwhile, the end-use market is gradually recovering, apparent steel demand has increased, and steel mill profits are moderate. Steel mills are resuming production, pig iron production has risen, and the rigid demand for coke has increased. In summary, the fundamentals of coke have improved, coke enterprise inventory has continued to decline, and profitability is moderate. The coke oven capacity utilization rate may increase slightly next week.

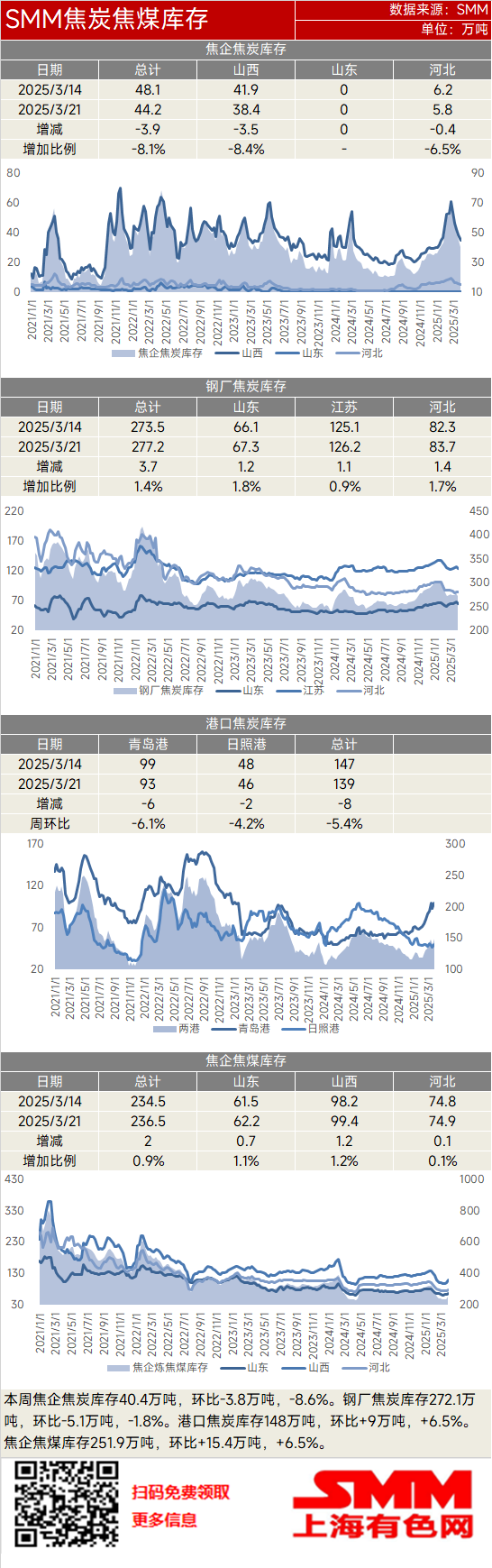

3. This week, coke enterprise coke inventory was 404,000 mt, down 38,000 mt WoW (-8.6%). Steel mill coke inventory was 2.721 million mt, down 51,000 mt WoW (-1.8%). Port coke inventory was 1.48 million mt, up 90,000 mt WoW (+6.5%). Coke enterprise coking coal inventory was 2.519 million mt, up 154,000 mt WoW (+6.5%).

This week, coke enterprise coke inventory continued to destock, and steel mill coke inventory also declined. Overall production enthusiasm among coke enterprises was moderate, coke supply increased slightly, and finished product sales improved. Steel mills gradually resumed production, driving pig iron production up and increasing the rigid demand for coke. Some steel mills with low coke inventory restocked, reducing coke enterprise inventory pressure. This week, steel market transactions performed moderately, reflecting the impact of the peak consumption season. Steel mill resumption led to increased coke consumption, and even though some steel mills restocked, it was difficult to offset the consumption.

In the near future, coke supply will increase slightly, and steel mills will continue to resume production, increasing coke consumption and restocking willingness. Coke enterprise coke inventory is expected to continue to decline next week, while steel mill coke inventory will remain stable.

This week, coke supply increased slightly, cost reduction space was limited, and steel mill purchase willingness increased. Coke prices stopped falling, and some traders began stockpiling in anticipation of opportunities. Port coke inventory may increase next week.

This week, coke enterprise coking coal inventory increased, mainly due to the limited downward space after a prolonged decline in coking coal prices and the emergence of cost-effectiveness in some oversold coal types. Some coke enterprises with low coking coal inventory began restocking. In the near future, coking coal prices are approaching coal mine production costs, mines have a strong sentiment to stand firm on quotes, and some coke enterprises and steel mills have restocking needs. Online auctions have seen more gains than losses, and the market transaction atmosphere has warmed up. Coke enterprise coking coal inventory may increase next week.

![Before the holiday, the black chain is unlikely to see a trend-driven market [SMM Steel Industry Chain Weekly Report].](https://imgqn.smm.cn/usercenter/zUFfM20251217171748.jpg)

![[SMM Chromium Daily Review] Inquiries and Transactions Weakened, Chromium Market Showed Mediocre Performance Before the Holiday](https://imgqn.smm.cn/usercenter/ENDOs20251217171718.jpg)