View SMM Aluminum Product Quotes, Data, and Market Analysis

Order and View SMM Metal Spot Historical Prices

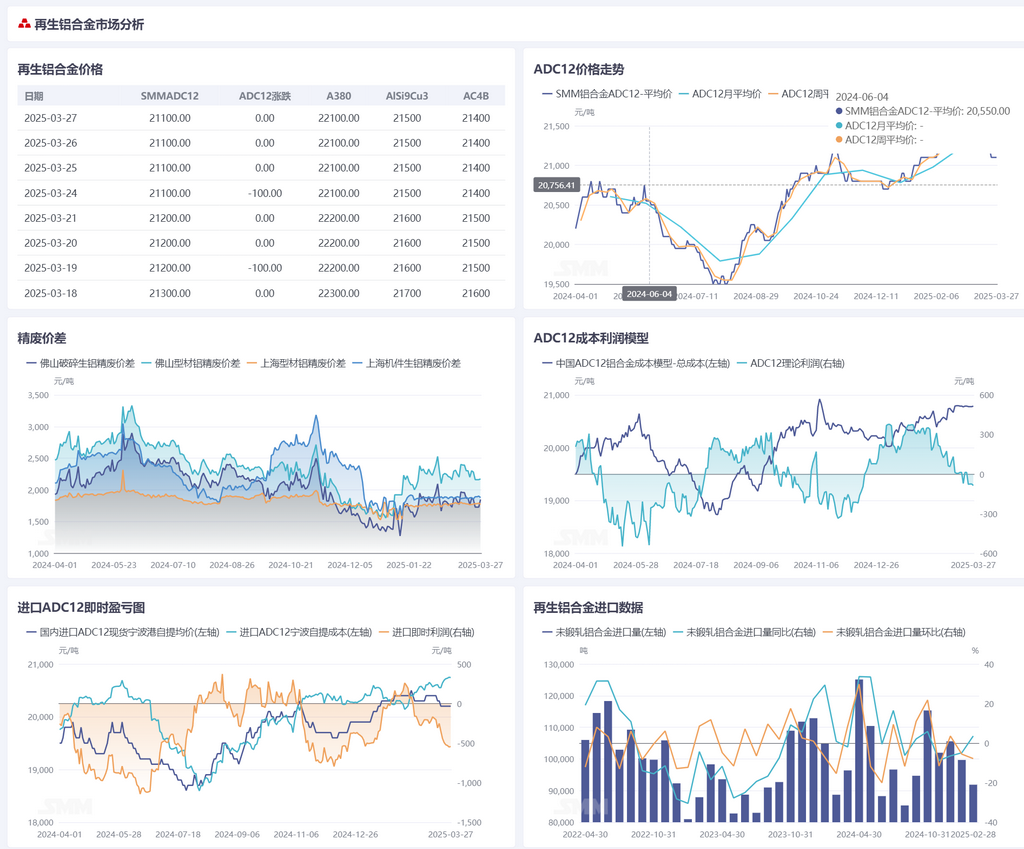

Secondary Aluminum Raw Materials:

This week, aluminum scrap prices remained stable overall. Following a significant rise in aluminum prices today, aluminum scrap prices stood firm on quotes. The market continues to maintain purchasing as needed, with the price difference between primary metal and scrap adjusting within a narrow range. In terms of supply, the operating rate of aluminum processing has continued to recover during the peak consumption season, and the supply of new scrap remains in an increasing range. Overseas, the price spread between domestic and overseas markets, with the overseas market outperforming the domestic market, has limited the growth of aluminum scrap imports. Additionally, export restrictions on aluminum scrap in Southeast Asia may increase, resulting in limited supply growth overseas. As of Thursday this week, the SMM A00 spot price was reported at 20,810 yuan/mt, flat WoW. The price of Shanghai machinery aluminum tense scrap was 18,933 yuan/mt, flat WoW, with the price difference between A00 aluminum and aluminum tense scrap flat WoW at 1,877 yuan/mt. The price difference between A00 aluminum and aluminum extrusion scrap in Foshan fell 129 yuan/mt WoW to 2,172 yuan/mt. In the short term, domestic aluminum scrap prices will follow the fluctuations of primary aluminum. However, due to weak downstream demand, buying sentiment weakened after the price increase, and the price difference between primary metal and scrap is expected to fluctuate rangebound next week.

Secondary Aluminum Alloy:

This week, aluminum prices first declined and then rose, while secondary aluminum alloy prices remained more likely to fall than rise. As of March 27, the SMM ADC12 price was down 100 yuan/mt WoW to 21,100 yuan/mt. Cost side showed divergence, with copper costs slightly increasing during the week, while aluminum scrap and silicon prices declined, leading to a slight pullback in overall costs. However, the price drop of finished alloy ingots exceeded the adjustment range of raw materials, further expanding theoretical losses in the industry. Under cost-side resistance, the downward range of low-priced goods in the market narrowed slightly. On the demand side, orders at secondary aluminum plants remained sluggish, and weak demand has made it difficult for secondary aluminum alloy prices to rise. Finished product inventories at enterprises increased. Supply side showed seasonal recovery, with the industry's operating rate rebounding in March, but limited production growth due to demand constraints. Under current production losses and inventory resistance, some companies are beginning to consider production cut plans. In terms of imports, overseas ADC12 quotes remain high at over $2,500/mt, with spot import prices concentrated at 20,100-20,300 yuan/mt. Recent domestic price trends have been under pressure, and with the continued depreciation of the RMB, the immediate loss on imported ADC12 has expanded to over 500 yuan/mt, keeping the import window closed. Overall, the supply-demand imbalance in the secondary aluminum alloy market has not been alleviated, and ADC12 prices will continue to face downward pressure. Future attention should be paid to raw material price fluctuations and changes in end-use consumption.