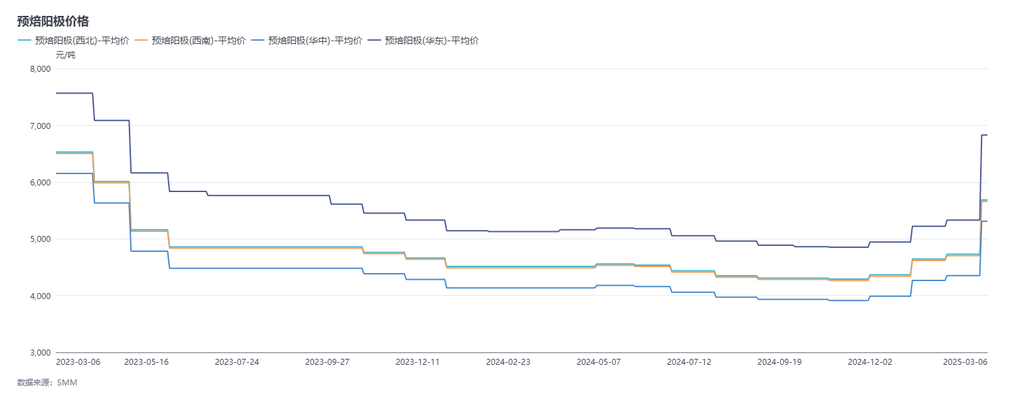

During the February cycle (February 6 to March 6), SMM prebaked anode prices increased significantly. The March 2025 procurement benchmark price of a certain aluminum smelter in Shandong was 5,066 yuan/mt, up 23.26% MoM. According to SMM, March prebaked anode export order prices followed the domestic raw material price surge, with adjustments concentrated around $130-220/mt. As of now, SMM's prebaked anode prices in east China closed at 5,066-8,594 yuan/mt.

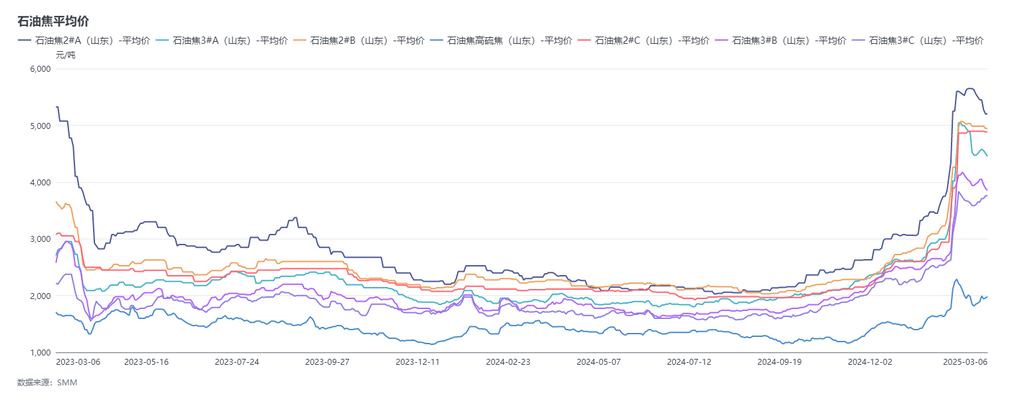

Raw material side: During this cycle, petroleum coke prices surged and then pulled back, especially after the holiday resumption of production, with significant price increases. The rise in the low-sulphur petroleum coke market was mainly driven by low refinery inventory levels in north-east China, combined with restocking and stockpiling demand from downstream enterprises after the holiday, leading to multiple price increases to a new annual high. Entering March, as downstream sentiment turned cautious, purchases slowed, and low-sulphur petroleum coke prices began to soften. According to SMM statistics, as of now, the average price of low-sulphur petroleum coke in north-east China reached 5,356 yuan/mt, up 20.63% from February 6. During the cycle, local refinery petroleum coke prices rose steadily due to support from both sellers and buyers, reaching a high of 3,138 yuan/mt on February 12. Subsequently, as downstream purchases weakened, prices entered a consolidation phase. According to SMM survey data, as of March 6, the average price of petroleum coke at local refineries rose to 2,864 yuan/mt, up 27.46% from February 6. Regarding coal tar pitch, its prices fluctuated upward during the cycle. According to SMM data, as of March 6, the average price of coal tar pitch was 4,671 yuan/mt, up 22.67% from February 6. Overall, the cost side pressure on prebaked anode enterprises increased significantly.

Supply side: In February 2025, the operating conditions of domestic prebaked anode enterprises slightly improved. The main reasons included the resumption of production in some enterprises in Henan and Shandong due to relaxed environmental protection policies and the commissioning of new capacity, as well as the recovery of production in other regions following maintenance. Additionally, the resumption of production by a certain enterprise in Fujian further contributed to the supply increase of prebaked anodes. However, as February is a short month, the overall production increase was somewhat limited. According to SMM calculations, the industry's operating rate in February was 73.18%, down 1.47 percentage points MoM. Overall, although the supply of prebaked anodes decreased, the overall supply remained relatively sufficient.

Demand side: By the end of February, SMM statistics showed that the existing capacity of domestic aluminum enterprises was approximately 45.81 million mt, with operating capacity around 43.64 million mt. The industry's operating rate increased by 0.07 percentage points MoM and 2.26 percentage points YoY to 95.3%. Currently, the operating capacity of domestic aluminum smelters is in a slight growth phase. Following the recovery of aluminum profits during the month, several previously curtailed enterprises in Sichuan and Guangxi resumed production in early February. Additionally, a capacity replacement and upgrade project at a certain aluminum smelter in Qinghai started production, contributing to the growth momentum of aluminum operating capacity. Entering March 2025, the operating capacity of domestic aluminum enterprises is expected to rise further as related enterprises reach full production, with annualized operating capacity stabilizing at 43.84 million mt/year by the end of March. The prebaked anode industry performed well in terms of domestic demand.

Brief analysis: During the cycle, a certain aluminum enterprise in Shandong adjusted its prebaked anode tender benchmark price for March 2025, up 956 yuan/mt MoM. Meanwhile, another major domestic prebaked anode sales company also raised its March sales price, up 1,381 yuan/mt MoM. This price adjustment was driven by the significant rise in petroleum coke prices and the gradual increase in coal tar pitch prices, leading to continuous cost increases for prebaked anodes. According to SMM calculations, as of March 6, the cost of prebaked anodes in China had reached approximately 6,032 yuan/mt. Despite the significant price increase for prebaked anodes in March, it was insufficient to offset the pressure from rising petroleum coke prices, resulting in some compression of enterprise profitability. Entering March, the petroleum coke market showed signs of weakness due to slowing downstream purchases, and refinery petroleum coke prices began to decline gradually. Currently, downstream demand for petroleum coke remains moderate, with most enterprises maintaining just-in-time procurement, providing limited support for petroleum coke prices. There are no clear signs of improvement in the short term. Therefore, SMM expects that prebaked anode prices may stabilize or decline slightly next month as the raw material market weakens. Future attention should focus on the operating conditions of prebaked anode and downstream aluminum enterprises.