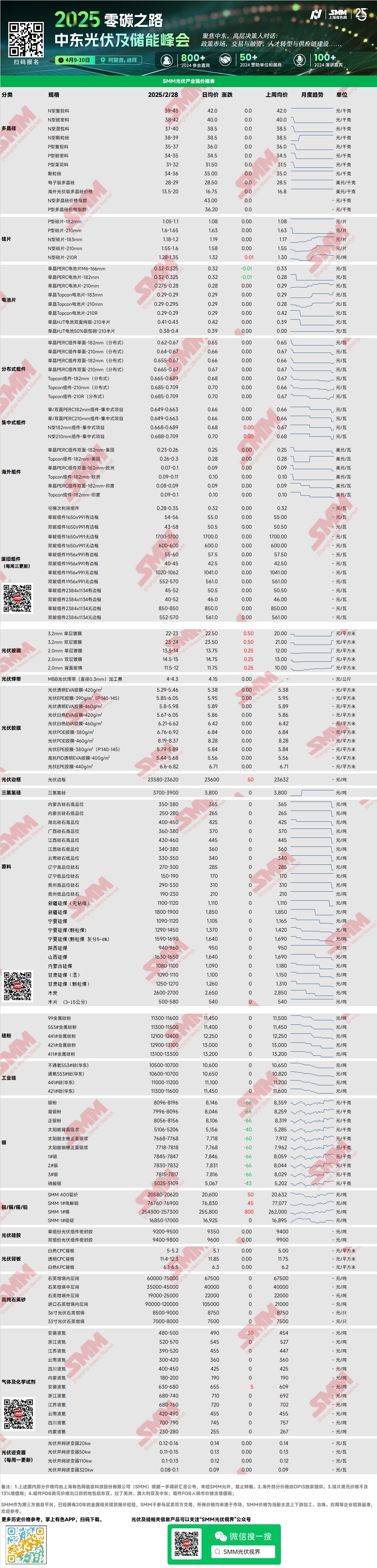

Polysilicon: This week, the mainstream transaction prices for N-type recharging polysilicon were 39-45 yuan/kg, while N-type dense material prices were 38-42 yuan/kg. Polysilicon transaction prices remained stable this week. In March, wafer production schedules were limited due to self-regulation, and market sentiment was relatively stable. From the perspective of March's supply-demand balance, polysilicon supply and demand were tightly balanced. Currently, there is still some inventory of polysilicon, and prices remain stable. Some enterprises intended to stand firm on quotes, but no actual implementation has been observed yet.

Wafers: This week, domestic N-type 18Xmm wafers were priced at 1.18-1.2 yuan/piece, N-type 210R wafers at 1.28-1.35 yuan/piece, and N-type 210mm wafers at 1.55-1.6 yuan/piece. Wafer prices increased this week, mainly due to collective price hikes by top-tier enterprises. It is understood that the new prices will take effect next week. Additionally, some enterprises with previously lower quotations began adjusting their wafer prices upward this week. March wafer production schedules were slightly insufficient compared to battery demand. Combined with the market sentiment boost in the earlier period and anticipated demand over the next 2-3 months, this led to the current round of price increases.

Solar Cells: This week, PERC cell prices saw some adjustments, mainly impacted by the resumption of production lines by some enterprises, which increased supply. Shipments were primarily directed to Indian customers, with minimal domestic demand. Current tolling business prices are 1.25 yuan/piece, while direct sales prices are 0.32 yuan/piece. Meanwhile, Topcon cell prices increased, driven by rising costs and growing demand. Shipments of Topcon cells increased, with current prices for Topcon 183 cells (efficiency of 25% and above) around 0.29 yuan/W, and transaction prices are expected to rise to 0.295-0.3 yuan/W. Topcon 210RN cells are priced at 0.29 yuan/W, expected to rise to 0.3 yuan/W, while Topcon 210 cells are priced at 0.29-0.295 yuan/W, showing an upward trend. However, there was no significant growth in demand for HJT and BC cells.

PV Modules: In this week's module market, mainstream transaction prices for centralized PERC 182mm modules were 0.649-0.673 yuan/W, PERC 210mm modules were 0.659-0.683 yuan/W, N-type 182mm modules were 0.659-0.693 yuan/W, and N-type 210mm modules were 0.669-0.703 yuan/W. Prices increased. March module production schedules rose approximately 40% MoM. Distributed rush-for-installation orders increased, and demand for centralized shipments also grew.

End-User: During the week of February 17-23, 2025, SMM statistics showed that domestic enterprises won bids for 22 PV module projects, with winning bid prices concentrated in the range of 0.65-0.82 yuan/W. The weighted average price for the week was 0.69 yuan/W, unchanged from the previous week. The total procurement capacity of winning bids was 2,807.96 MW, a decrease of 339.49 MW compared to the previous week. Domestic rush-for-installation orders increased, and demand in the distribution market improved.

EVA: This week, mainstream transaction prices for PV-grade EVA were 11,300-11,650 yuan/mt, while prices for foam-grade and cable-grade EVA also rose slightly. The market atmosphere was relatively active. Under the influence of policies, downstream module manufacturers may engage in rush-for-installation activities, leading to tight supply and increased demand. The overall market still exhibited an undersupply situation, and the supply-demand imbalance is unlikely to ease in the short term. Prices are expected to remain high in the near future.

EVA Film: Prices from top-tier enterprises remained stable this week, with mainstream transaction prices at 12,600-12,800 yuan/mt. Rising raw material prices, coupled with the strong demand boost from the PV "rush-for-installation wave," drove both supply and demand. Under this dual push, EVA film prices are expected to trend upward in March.

PV Glass: This week, PV glass prices increased. As of now, the mainstream quotations for 2.0mm single-layer coated glass are 14.0 yuan/m², 3.2mm single-layer coated glass are 22.5 yuan/m², and 2.0mm back glass are 12.0 yuan/m². This week, glass prices rose significantly by 2 yuan/m². Module enterprises mainly engaged in price negotiations this week, with no new orders signed for purchases yet. Meanwhile, the cost increase caused by stable module prices and rising glass prices led to a strong desire among module enterprises to bargain down prices. However, glass destocking performed well, and module demand is expected to continue rising. Under the supply-demand mismatch, the trend of rising glass prices became evident.

High-Purity Quartz Sand: This week, domestic high-purity quartz sand prices remained stable, but a slight increase is expected next week. Current market quotations are as follows: inner-layer sand at 65,000-75,000 yuan/mt, middle-layer sand at 35,000-45,000 yuan/mt, and outer-layer sand at 19,000-25,000 yuan/mt. Prices remained stable. Domestic leading enterprises plan to raise quotations for middle and outer-layer sand due to changes on the supply side, which have significantly reduced production recently. However, crucible enterprises have not yet depleted their quartz sand inventories, and some crucible products remain unsold. In the short term, crucible enterprises have low purchasing intentions, adopting a wait-and-see attitude toward price increases. Nevertheless, leading enterprises showed a clear intention to increase prices, and other sand enterprises also expressed willingness to follow suit. In the short term, sand prices are expected to trend upward.

Backsheet Weekly Review: This week, PV backsheet prices in the high-price range increased. White CPC backsheets with double fluorine coating were priced at 5.0-5.3 yuan/m², with the average price rising by 0.1 yuan/m². Transparent CPC backsheets with double fluorine coating were priced at 11.4-12.3 yuan/m², with the average price also rising by 0.1 yuan/m². The main reason for the high-price range increase was that new orders for conventional CPC backsheets from leading external backsheet manufacturers were mostly signed at around 5.3 yuan/m², with some manufacturers maintaining high quotations of 5.5 yuan/m². However, actual transactions at high prices were not ideal. Most high-price orders at 5.3 yuan/m² were small spot orders. Leading backsheet manufacturers maintained quotations at 5.1-5.2 yuan/m². Overall, based on orders on hand, March production schedules for manufacturers were not ideal. March orders were mainly concentrated among the top two backsheet enterprises, while other backsheet manufacturers expected March production schedules to remain around 1 million m² or even lower.

》View the SMM PV Industry Chain Database

![[SMM PV News] Armenia Hits 1.1 GW Solar Capacity,](https://imgqn.smm.cn/usercenter/qQwIB20251217171741.jpg)

![Spot Market and Domestic Inventory Brief Review (February 5, 2026) [SMM Silver Market Weekly Review]](https://imgqn.smm.cn/usercenter/tSwaX20251217171735.jpg)