This week, the total rebar inventory nationwide continued to increase slightly, with the growth rate further narrowing. However, the trends of in-plant and social inventories diverged, as in-plant inventory shifted from an increase to a decrease, with the turning point arriving earlier than expected. Specifically, the total rebar inventory increased by 1.76% WoW, while in-plant inventory decreased by 2.23% WoW. The total wire rod inventory increased by 0.46% WoW, while in-plant inventory decreased by 3.66% WoW. This week, construction steel market prices first declined and then rose, showing significant fluctuations. The price increase stimulated speculative demand in the market, while end-use demand continued to recover. Although supply also increased slightly, the demand growth outpaced it, leading to a further narrowing of the total construction steel inventory growth this week.

This week, the total rebar inventory reached 8.0714 million mt, up by 139,800 mt WoW, an increase of 1.76% (previous value: +3.47%), and decreased by 4.2364 million mt YoY, a decline of 34.42% (previous value: -33.26%).

Table 1: Overview of Rebar Inventory

Source: SMM

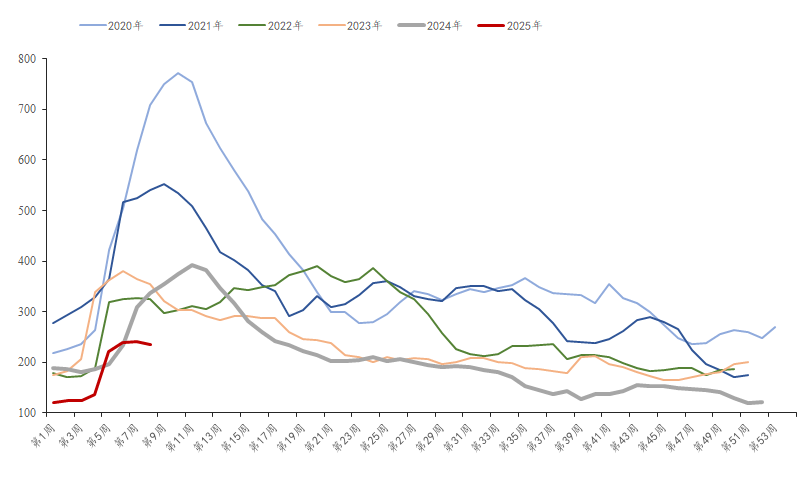

This week, the in-plant rebar inventory was 2.3604 million mt, down by 53,800 mt WoW, a decrease of 2.23% (previous value: +1.12%), and decreased by 1.3858 million mt YoY, a decline of 36.99% (previous value: -31.86%). As downstream demand gradually recovered, some steel mills increased direct supply to end-users. Meanwhile, market prices rose significantly during the week, prompting agents to restock. Consequently, the in-plant rebar inventory shifted from an increase to a decrease, with the turning point arriving earlier than expected.

Chart-1: Trends of In-Plant Rebar Inventory, 2019-2024

Source: SMM

This week, the social rebar inventory was 5.7109 million mt, up by 193,700 mt WoW, an increase of 3.51% (previous value: +4.54%), and decreased by 2.8506 million mt YoY, a decline of 33.3% (previous value: -33.86%). Currently, the recovery of downstream demand in south China is significantly faster than in north China. This week, the social rebar inventory increased slightly, with the growth rate continuing to narrow compared to last week.

Chart-2: Trends of Social Rebar Inventory, 2019-2024

Source: SMM

Looking ahead, February is coming to an end. Currently, downstream end-use demand in south China is recovering well, while in north China, resumption of work has been delayed due to climatic factors. It is expected that demand in many regions will recover significantly in early March. On the supply side, although the average production cost of rebar for blast furnace steel mills is slightly profitable, the profit margin is relatively low compared to other products, and the demand intensity has not yet returned to normal levels, leaving steel mills with little incentive to increase rebar production. While EAF steel mills have mostly resumed production, they are constrained by difficulties in sourcing steel scrap and thin profit margins, with some already experiencing slight losses. Overall production is more likely to decrease than increase. Fortunately, the absolute inventory level remains relatively low YoY, demand continues to recover, and supply growth is limited. The fundamentals are relatively healthy, and it is expected that next week, construction steel inventory will still see an increase in social inventory and a decrease in in-plant inventory, with the total inventory growth rate continuing to narrow.

![Before the holiday, the black chain is unlikely to see a trend-driven market [SMM Steel Industry Chain Weekly Report].](https://imgqn.smm.cn/usercenter/zUFfM20251217171748.jpg)

![[SMM Chromium Daily Review] Inquiries and Transactions Weakened, Chromium Market Showed Mediocre Performance Before the Holiday](https://imgqn.smm.cn/usercenter/ENDOs20251217171718.jpg)