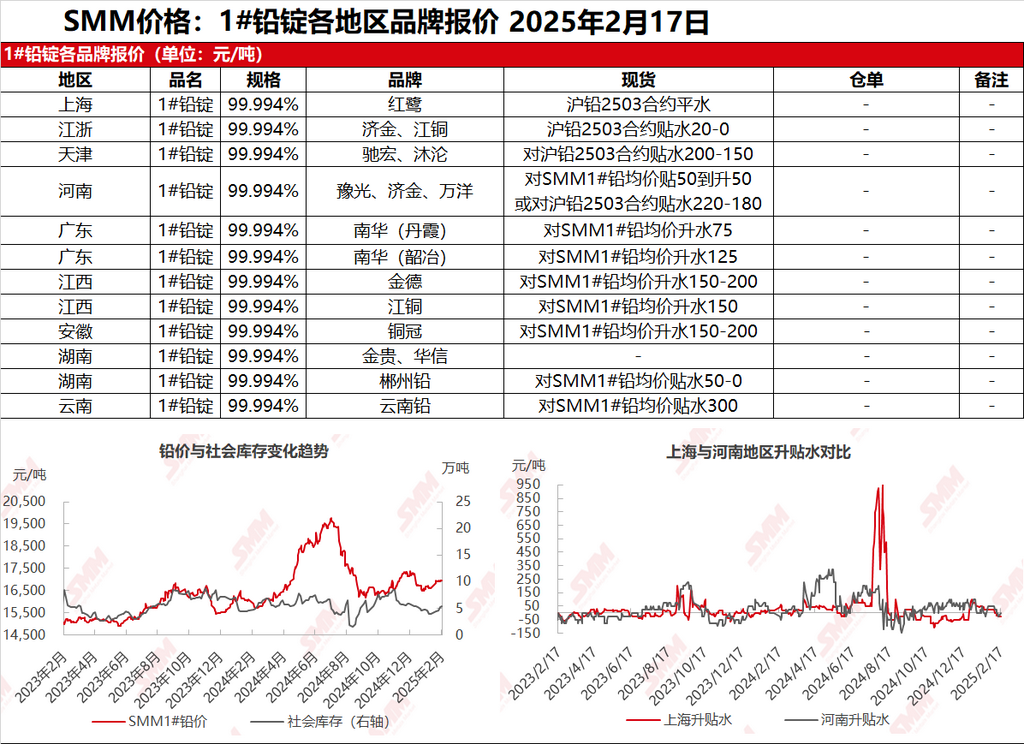

SMM, February 17: In the Shanghai market, Honglu lead was quoted at 17,135-17,170 yuan/mt, on par with the SHFE 2503 contract; in Jiangsu and Zhejiang regions, JCC and Jijin lead were quoted at 17,115-17,170 yuan/mt, with spot discounts of 20-0 yuan/mt against the SHFE 2503 contract. SHFE lead remained range-bound, and suppliers followed the market trend in selling. As today marked the delivery date for the SHFE 2502 contract, some suppliers focused on delivery matters, and spot discounts were basically flat WoW. Meanwhile, ex-factory quotations for primary lead cargoes self-picked up from production sites were at discounts of 50 yuan/mt to premiums of 150 yuan/mt against the SMM 1# lead average price, with some traders quoting discounts as deep as 75 yuan/mt. For secondary lead, secondary refined lead was quoted at discounts of 150-0 yuan/mt against the SMM 1# lead average price ex-factory. Downstream demand remained sluggish, with long-term contract purchases dominating, while some rigid demand leaned towards the lower-priced secondary lead. Spot order market transactions were muted.

Other markets: Today, the SMM 1# lead price was flat compared to the previous trading day. In Henan, suppliers quoted discounts of 180-220 yuan/mt against the SHFE 2403 contract, while some smelters with low inventories quoted on par with the SMM 1# lead average price ex-factory. In Hunan, smelter supply had not fully recovered, and manufacturers mainly quoted on par or with slight premiums, while traders quoted discounts of 50-0 yuan/mt against the SMM 1# lead average price for transactions. In Yunnan, discounts of 300 yuan/mt were maintained with limited rigid demand transactions. Downstream production and procurement gradually resumed, and regional rigid demand transactions slightly improved WoW.