SMM, January 21:

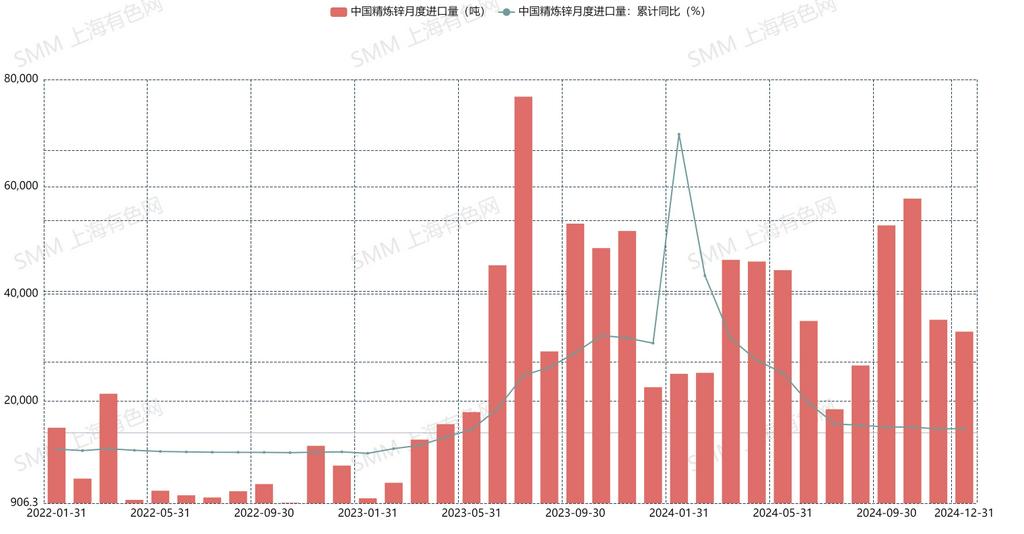

According to the latest customs data, refined zinc imports in December 2024 totaled 32,900 mt, down 2,200 mt or 6.31% MoM, but up 45.94% YoY. From January to December, cumulative refined zinc imports reached 445,700 mt, up 17.22% YoY. Refined zinc exports in December were 4,300 mt, resulting in net imports of 28,600 mt for the month.

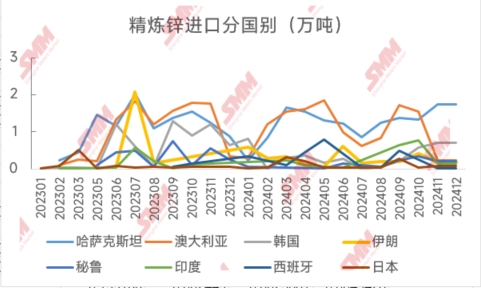

The top three sources of refined zinc imports in December were Kazakhstan (12,700 mt, 38.74%), Australia (5,700 mt, 17.21%), and South Korea (4,900 mt, 14.93%). Country-specific data show that Kazakhstan, South Korea, and Australia remained in leading positions. In terms of trade mode, the increase in Entrepot Trade by Customs Special Control Area was significant.

Overall, December's refined zinc import volume fell short of previous expectations, mainly due to the SHFE/LME zinc price ratio remaining at a low level, with limited import window openings. Imports were primarily driven by overseas inflows, resulting in relatively low overall import volumes.

In January, during the early period of Trump's overseas inauguration, market information is expected to be relatively scarce. Although LME inventory is expected to decline to around 200,000 mt, the LME cash-3M contango is expected to widen to approximately $40/mt, leading to weaker LME zinc performance. Domestically, under the expectation of overseas tariff hikes, policy support is expected to strengthen. Although TC continues to rise, it remains at a historically low level below 3,000 yuan/mt (metal content), and social inventory is at a relatively low level of less than 60,000 mt, providing some support for SHFE zinc. Overall, LME underperforms SHFE, with intermittent import window openings offering market import opportunities. However, downstream demand is expected to weaken as the Chinese New Year approaches, coupled with long-term contract import volumes. January's import volume is expected to remain around 30,000 mt.

![Supply-Side Support Pushed the Zinc Price Center Higher [SMM Weekly Zinc Commentary]](https://imgqn.smm.cn/usercenter/tAyyp20251217171754.jpg)

![[SMM Conference] PbZn Conference 2026 Gathers Global Leaders to Navigate Evolving Market Dynamics](https://imgqn.smm.cn/production/admin/votes/imagesbznIX20260330170246.jpeg)