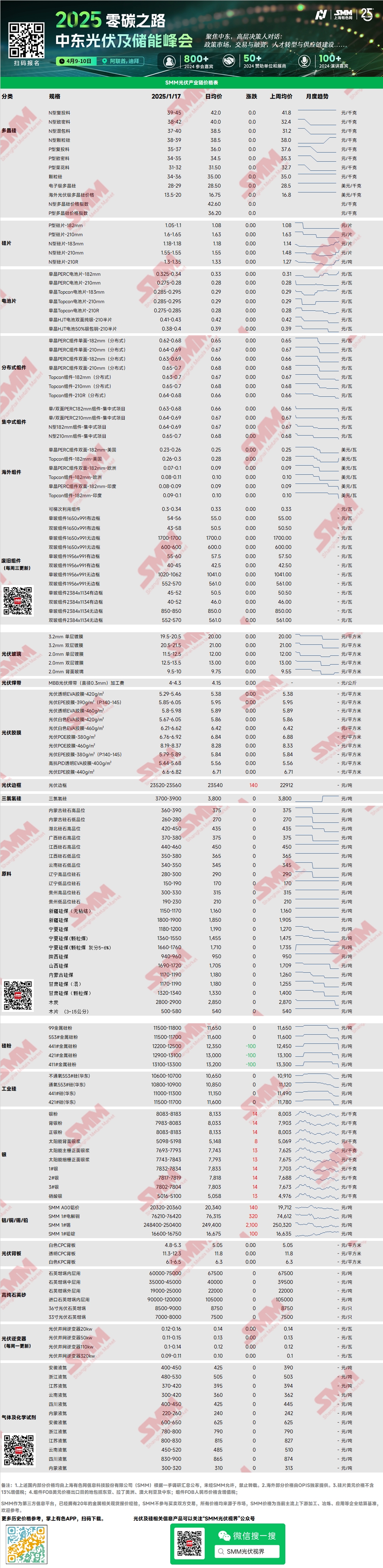

Polysilicon: This week, the mainstream transaction prices for N-type recharging materials ranged from 39-45 yuan/kg, while N-type dense materials were traded at 38-42 yuan/kg. Polysilicon quotation ranges remained stable this week, with several new transactions recorded—downstream enterprises made multiple small-volume supplementary purchases of polysilicon. Transactions showed rod-shaped silicon at around 42 yuan/kg and granular silicon at approximately 38 yuan/kg. Currently, polysilicon enterprises are generally standing firm on quotes. However, as downstream stockpiling for the Chinese New Year has been completed and raw material inventories are at high levels, short-term transaction willingness is weak. Polysilicon prices are likely to experience slight fluctuations.

Silicon Wafer: This week, domestic N-type 18Xmm silicon wafers were priced at 1.18-1.18 yuan/piece, N-type 210R wafers at 1.3-1.35 yuan/piece, and N-type 210mm wafers at 1.55-1.55 yuan/piece. Late last week, silicon wafer prices rose across the board, mainly due to the disappearance of previously low-priced delivery orders. Additionally, some solar cell enterprises replenished specific sizes they lacked before the Chinese New Year, with transactions mostly occurring at the higher end of the quotation range. However, silicon wafer enterprises are gradually facing transaction pressure, with trading volumes remaining sluggish. Downstream resistance to high prices is evident, and prices are temporarily stagnant.

Solar Cell: This week, prices for various Topcon solar cells successfully stabilized at high levels. As the Chinese New Year approaches, Topcon cells were sold at high price points, increasing downstream cost pressure. However, with pre-holiday stockpiling completed, market sentiment has pulled back, and there is a risk of price declines for Topcon cells in the future. Prices for Topcon 183 solar cells (efficiency ≥25%) were around 0.285-0.295 yuan/W, Topcon 210RN cells at 0.285-0.29 yuan/W, and Topcon 210 cells at 0.285-0.295 yuan/W. PERC cell prices have risen to 0.325-0.34 yuan/W, mainly supported by overseas demand and tight supply. Prices are expected to remain firm over the next two months.

PV Module: In the current PV module market, mainstream transaction prices for centralized PERC 182mm modules were 0.63-0.68 yuan/W, PERC 210mm modules at 0.64-0.69 yuan/W, N-type 182mm modules at 0.64-0.69 yuan/W, and N-type 210mm modules at 0.65-0.7 yuan/W. Mainstream transaction price ranges remained stable. During the off-season, order volumes have significantly decreased, and some enterprises have lowered prices to stimulate cargo pick-up. Prices in the centralized market remained relatively stable and are expected to hold steady until the Chinese New Year. Distributed market prices still showed some fluctuations, but due to reduced trading frequency, prices were slightly more stable than last week. As the Q1 off-season approaches, enterprises are producing based on sales and focusing on selling inventory. Recently, some enterprises have continued to reduce operating rates or shut down production lines. January's actual production is expected to decline further compared to forecasts, with February's operations remaining steady and many orders accumulating for delivery in March.

End-User: During the week of January 6 to January 12, 2025, SMM statistics showed that 32 domestic enterprises won bids for PV module projects, with winning bid prices concentrated in the range of 0.66-0.75 yuan/W. The weighted average price for the week was 0.69 yuan/W, an increase of 0.02 yuan/W compared to the previous week. The total procurement capacity of winning bids was 6,890.39 MW, an increase of 6,247.82 MW from the previous week. Entering 2025, ground-mounted power station projects have entered a rest period, with progress slowing. Before the Chinese New Year, there was a rush to install residential projects, maintaining module procurement demand, while the commercial and industrial sectors showed slight weakness. Overall, Q1 remains a domestic demand off-season, with limited installations expected before and after the holiday. Most orders scheduled for pre-holiday delivery are postponed to later in the year. Starting mid-February, orders are expected to increase slightly with centralized project procurement, with most demand accumulating in March.

Encapsulation Film: This week, EVA transparent film prices ranged from 12,600-13,000 yuan/mt, EPE co-extruded film at 15,000-15,300 yuan/mt, and POE film at 17,800-18,100 yuan/mt. PV-grade EVA transparent film faced significant pressure, with some production lines already shut down. Next week, small and medium-sized enterprises will gradually begin their holidays, while large enterprises will maintain partial production at some bases during the Chinese New Year.

EVA/POE: PV-grade EVA prices were traded at 10,350-10,700 yuan/mt, while POE transaction prices ranged from 12,000-13,800 yuan/mt. The EVA market experienced tight spot supply, with robust pre-holiday stockpiling demand driving transaction centers upward.

PV Glass: This week, PV glass quotations remained stable. As of now, the mainstream quotation for 2.0mm single-layer coating glass is 12.0 yuan/m², and for 3.2mm single-layer coating glass, it is 19.5 yuan/m². Domestic PV glass market quotations were stable this week. With logistics nearing a halt, recent market glass transaction volumes were low. Leading module enterprises have not yet finalized January's pricing. Domestic supply remained stable this week, with no cold repairs or furnace shutdowns. Although there are plans for cold repairs of approximately 2,000 mt/day, these may be delayed. On the demand side, module demand has weakened recently, with some module enterprises already on holiday or halting production. Domestic demand in January continues to decline, but glass production will continue during the Chinese New Year, leading to inventory pressure for enterprises. Regarding price forecasts, mainstream transaction prices for glass are expected to remain stable in January. However, due to varying inventory levels among glass enterprises, some may offer discounts to clear inventory, potentially causing slight downward adjustments in market transaction prices.

High-Purity Quartz Sand: This week, domestic high-purity quartz sand prices remained stable. Current market quotations are as follows: inner-layer sand at 65,000-75,000 yuan/mt, middle-layer sand at 35,000-45,000 yuan/mt, and outer-layer sand at 19,000-25,000 yuan/mt. Prices have temporarily stabilized. Domestic high-purity quartz sand quotations showed no changes this week. After leading enterprises raised prices, downstream enterprises have not yet entered the market for procurement. Market consumption sentiment remains relatively low, with many crucible enterprises on holiday, reducing demand for quartz sand. Procurement willingness is low, with most enterprises indicating that negotiations and purchases will begin after the holiday. On the supply side, quartz sand supply has continued to decline recently. For outer-layer sand, some enterprises have shifted production to pipe materials due to decreasing profits, reducing supply. Middle and outer-layer sand supplies have also decreased due to production cuts by leading enterprises. On the demand side, silicon wafer production schedules have increased recently, but further growth momentum is limited. Quartz sand demand has not risen significantly, and current crucible inventories are high, limiting sand consumption. Therefore, price forecasts suggest limited demand stimulation. Although supply has decreased, supply and demand remain balanced. Sand enterprises are expected to offer discounts to clear inventory, with limited support for price increases.

PV Backsheet: This week, PV backsheet market prices remained stable at low levels. White CPC backsheet with dual fluorine coating was priced at 4.8-5.3 yuan/m², while transparent CPC backsheet with dual fluorine coating was priced at 11.3-12.3 yuan/m². Recent backsheet market transactions were sluggish. The downstream single-glass module market was already weak, and as the Chinese New Year approaches, downstream procurement demand has further weakened. January's overall backsheet production schedules declined by nearly 20% compared to December, with industry operating rates at around 8%. The market remains sluggish, and backsheet manufacturers are generally pessimistic. Backsheet market prices are holding steady. Apart from some small domestic factories that had already shut down production lines, some leading enterprises have also indicated plans to significantly reduce backsheet capacity in 2025. Due to further declines in downstream single-glass module demand, annual backsheet production is expected to remain at low levels, with industry average operating rates likely to stay around 10%.

Inverter: This week, inverter price ranges were as follows: 20kW at 0.12-0.16 yuan/W, 50kW at 0.11-0.15 yuan/W, 110kW at 0.1-0.14 yuan/W, and 320kW at 0.09-0.11 yuan/W. Supply-side production remained stable and sufficient, while overall demand sentiment was mediocre. Large-power string and centralized models accounted for most shipments.

》View the SMM PV Industry Chain Database

![[SMM PV News] Puerto Rico Rooftop Solar Hits 20% of Total Power Capacity](https://imgqn.smm.cn/usercenter/kuMAH20251217171739.jpg)

![[SMM PV News] US Solar Faces Labor Shortage Ahead of 'OBBBA' Deadline](https://imgqn.smm.cn/usercenter/xBtJB20251217171738.jpg)