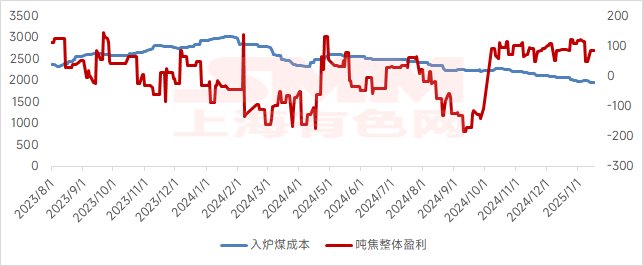

1. According to the SMM survey, coke profit per mt was 84.8 yuan/mt this week, and coke producers' profits continued to narrow.

From a price perspective, coke prices fell by 50-55 yuan/mt last week, exerting significant negative pressure on coke producers' profit per mt. From a cost perspective, the decline in coking coal prices was relatively small. For example, the price of low-sulfur primary coking coal remained at 1,450 yuan/mt, and the price drop for other coal types was also within 50 yuan/mt. As a result, coking costs decreased slowly, and coke producers' profits shrank significantly.

Coke prices still face downside risks, but the room for coking coal price declines is limited, making it difficult for coking costs to decrease significantly. If coke prices continue to fall, some coke producers may incur losses next week.

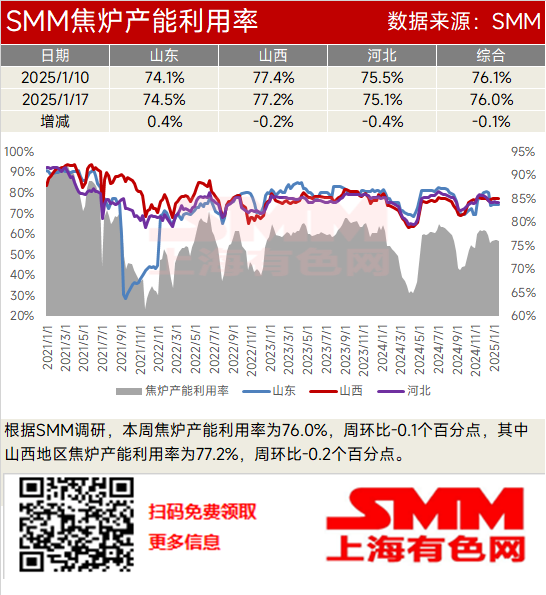

2. According to the SMM survey, the coke oven capacity utilization rate was 76.0% this week, down 0.1 percentage points WoW. In Shanxi, the coke oven capacity utilization rate was 77.2%, down 0.2 percentage points WoW.

From a profitability perspective, most coke producers still maintain profits, which positively impacts their production. From an inventory perspective, coke producers' inventories continued to build up, while downstream steel mills mainly purchased as needed, with low restocking willingness. From an environmental protection perspective, environmental protection inspections have eased in various regions, and coke producers that previously reduced production due to environmental factors have increased production.

Coke producers face the risk of losses, but these remain within the tolerable range for most producers, with little change in production. Coke supply is expected to remain stable before the Chinese New Year. Although the finished steel market has warmed up, steel billet profits remain poor, and steel mills' coke inventories are at reasonable levels, leading to low restocking willingness. In summary, the coke oven capacity utilization rate of coke producers is likely to remain stable next week.

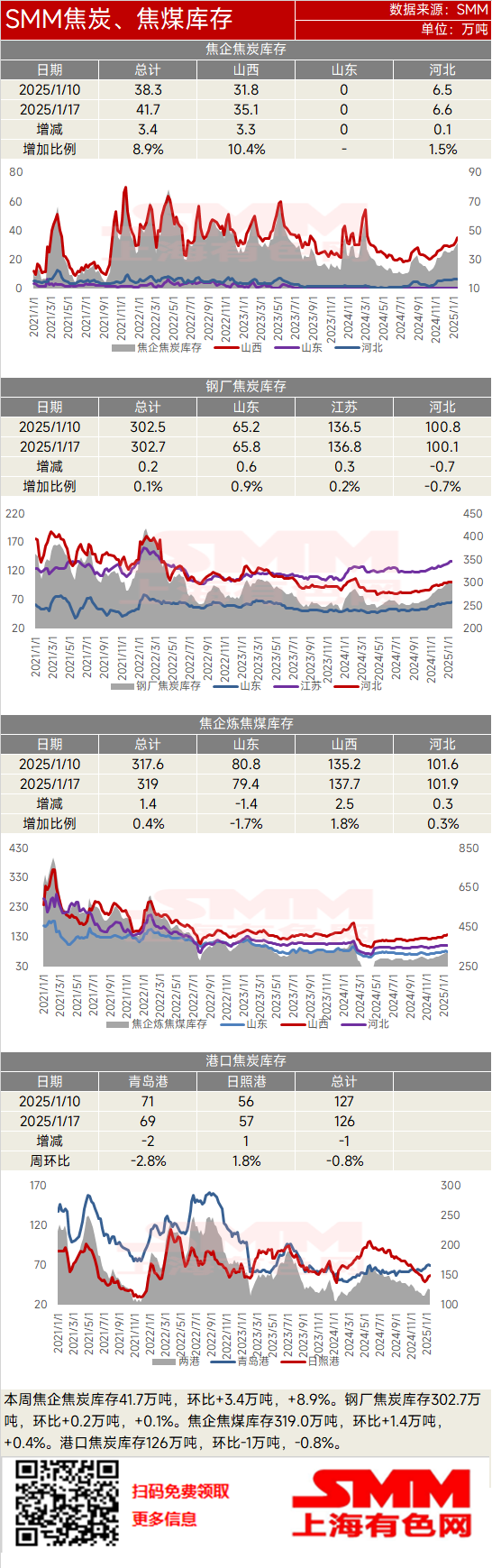

3. This week, coke producers' coke inventory was 417,000 mt, up 34,000 mt (+8.9%) WoW. Steel mills' coke inventory was 3.027 million mt, up 2,000 mt (+0.1%) WoW. Coke producers' coking coal inventory was 3.19 million mt, up 14,000 mt (+0.4%) WoW. Port coke inventory was 1.26 million mt, down 10,000 mt (-0.8%) WoW.

This week, coke producers' coke inventories continued to build up, while steel mills' coke inventories fluctuated rangebound. Coke producers have maintained profits, and the situation remains stable, with coke supply staying at high levels. Most steel mills have completed their pre-Chinese New Year restocking needs. Even as the finished steel market warms up, steel mills continue to purchase coke as needed, with only a few mills with low inventories engaging in restocking.

Coke producers' profits are likely to hover around the break-even point. Even if losses occur, they remain within the tolerable range for most producers, and overall production is expected to remain stable. However, most downstream steel mills have completed restocking, and their demand for coke is moderate. Some steel mills with high coke inventories have already started controlling coke arrivals. The market is entering the holiday mode for the Chinese New Year, with a relatively subdued trading atmosphere. Therefore, coke producers are expected to continue building up inventories next week, while steel mills' coke inventories may continue to fluctuate rangebound.

This week, private coal mines began to shut down for the holiday, and state-owned coal mines are expected to follow suit next week. Coking coal supply from coal mines is expected to decline. However, as coke producers' profits shrink and their coking coal inventories have already been replenished, online auction prices for coking coal remain mostly on a downward trend. Most coke producers show moderate purchase willingness for coking coal, so coke producers' coking coal inventories are expected to fluctuate rangebound next week.

This week, coke supply remained ample, and market participants continued to hold bearish expectations for coke prices. Speculative demand from traders was limited, and port coke inventories are expected to decrease next week.

![Strong Cost Support Remained; Ferrous Metals May Hold Up Well in the Short Term [SMM Steel Industry Chain Weekly Report]](https://imgqn.smm.cn/usercenter/gaBsW20251217171749.jpg)

![[SMM Daily HRC Trading Volume] Futures Hovered at Highs, Spot Trading Changed Relatively Little](https://imgqn.smm.cn/usercenter/JSngP20251217171719.jpg)