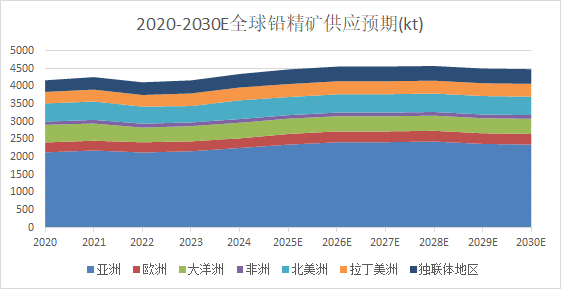

From 2020 to 2023, challenges such as the pandemic, strikes, extreme weather, and declining grades impacted the smooth commissioning of lead and zinc mine projects. Meanwhile, the recovery of downstream lead consumption in Asia and the rapid operation of newly commissioned smelter capacity expanded the supply gap for lead concentrates. It was not until 2024, when newly commissioned lead and zinc mine projects ramped up production, that the tight supply of lead concentrates began to ease.

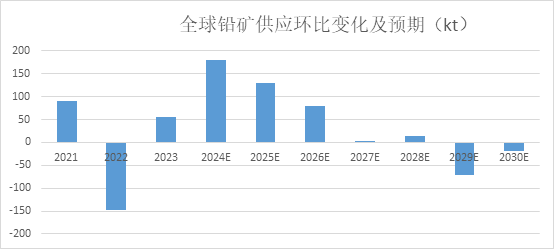

According to SMM's understanding and preliminary estimates, the global supply of lead ore is expected to grow from 2024 to 2026, a trend that has reached consensus. However, the output growth of lead concentrates or silver-lead ore from polymetallic mine projects, which are widely monitored by smelters, is expected to be relatively limited. Additionally, as new projects enter stable operation, the growth rate of lead ore supply may slow relatively from 2026 to 2028.

In terms of the contribution to the growth of lead concentrate supply in 2025, regional data shows that Asia is expected to see an increase of over 90,000 mt in metal content (49%), while Europe (excluding Russia) and the CIS region are each expected to record an increase of approximately 30,000 mt in metal content (15% and 17%, respectively). Other regions are expected to record negative growth.

Therefore, Asia remains the primary supply region for lead concentrates over the next five years, with the growth in lead ore supply in 2025 also mainly contributed by Asia. Additionally, new projects in Latin America and the restart of lead and zinc mines in the CIS region will bring some incremental supply. Meanwhile, existing mines in North America and Australia are expected to record negative growth due to declining grades and nearing the designed mining life, leading to production declines.

![SHFE Lead Prices Lacked Upward Momentum, and the Pattern of Doldrums Was Difficult to Change [Lead Futures Brief Review]](https://imgqn.smm.cn/usercenter/mIbTL20251217171721.jpg)

![LME Lead Rebounded Strongly After Hitting Bottom; SHFE Lead Opened Higher With a Gap, Came Under Pressure, and Pulled Back [SMM Lead Morning Brief]](https://imgqn.smm.cn/usercenter/qnyHQ20251217171721.jpeg)