2025 is an extraordinary year, a year of both opportunities and risks. The rapid changes in internal and external environments have posed new demands on risk awareness and decision-making capabilities for practitioners in the magnesium industry.

Affected by the downward fluctuation of raw material prices, magnesium prices in 2024 continued to decline. Taking the price of 90# magnesium ingots in Fugu, the main production area, as an example, the year-end price of 16,000 yuan/mt dropped significantly from 20,250 yuan/mt at the beginning of the year, marking a 21% decline. The sharp drop in magnesium prices has brought unprecedented cost pressure to magnesium ingot smelters, drastically compressing profit margins and making operations challenging for most magnesium ingot smelters.

[Magnesium Ingot Supply]

In terms of supply, China's magnesium ingot production in 2024 is expected to reach 941,000 mt, up 14.3% YoY. The increase in China's magnesium ingot production in 2024 mainly comes from the resumption of production at magnesium plants in Fugu. According to the 2024 provincial comparison of China's magnesium ingot production, Shaanxi accounted for 57% of the total magnesium ingot production, recovering to 61%.

[Magnesium Ingot Demand]

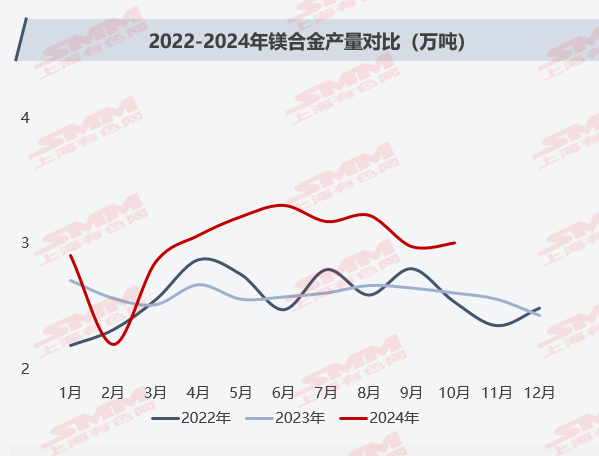

Magnesium Alloy:

The significant rise in magnesium prices in recent years has severely impacted the production and export volumes of magnesium alloys. Domestic die-casting enterprises, in particular, have faced substantial profit compression due to the sharp rise in raw material prices and the lack of pricing power. Some small and medium-sized factories, under cost pressure, opted to halt or cut production, leading to the suspension of magnesium alloy projects and significant obstacles in expanding downstream applications of magnesium alloys.

As magnesium prices gradually stabilized in 2024, the cost-effectiveness of magnesium alloys became increasingly evident. Downstream demand for magnesium alloys gradually recovered, and market acceptance improved. Some factories even resumed production for export orders. According to SMM statistics, China's total magnesium alloy production in 2024 reached 354,000 mt, up 14.2% YoY.

It is reported that dozens of automotive magnesium alloy components have been developed in the market, including steering wheel frames and dashboard brackets. Among them, magnesium alloy steering wheel frames have been applied in over 80% of vehicles. Large magnesium alloy components such as dashboard brackets, center console brackets, display screen brackets, and air conditioning brackets are increasingly used in high-end brand vehicles. Therefore, the promotion of magnesium alloy applications in NEVs is expected to significantly boost market demand for magnesium alloys. According to SMM forecasts, the demand for automotive magnesium alloys is expected to reach 161,000 mt, 229,000 mt, and 307,000 mt in 2023, 2024, and 2025, respectively.

Aluminum Alloy:

As an indispensable additive in aluminum alloys, magnesium, though consumed in limited quantities per unit, still holds a significant share in magnesium applications due to the large production base of aluminum alloys. According to the SMM survey, China's aluminum billet production in 2024 is expected to reach 16.79 million mt, up 5.1% YoY, with domestic aluminum alloy magnesium consumption at 182,000 mt.

From the supply and demand perspective of the aluminum alloy market, the domestic aluminum market's supply side shows limited elasticity and is likely to remain at a high level. On the demand side, the fundamentals are constrained by the domestic economic growth rate, with elasticity changes more dependent on policy expectations. The demand for magnesium in aluminum alloys is expected to remain stable.

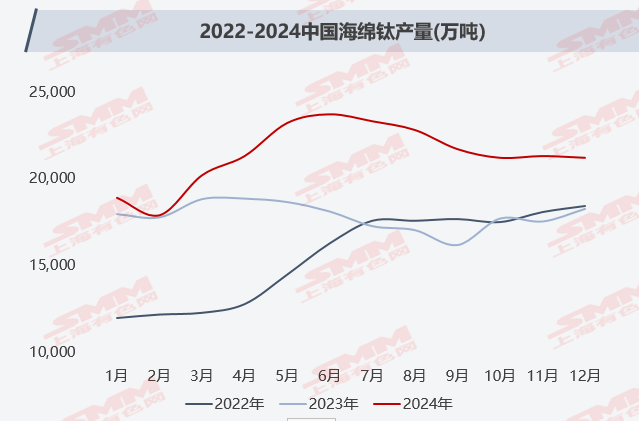

Sponge Titanium:

According to the SMM survey, China's sponge titanium production in 2024 is expected to reach 257,000 mt, up 17% YoY. Domestic sponge titanium production in 2024 maintained a growth trend, with sponge titanium enterprises reducing production costs through titanium-magnesium joint production. This adjustment reduced magnesium consumption per ton of titanium from 1.1 mt to 0.1 mt, resulting in annual magnesium ingot procurement of less than 50,000 mt by sponge titanium plants. Consequently, the demand for magnesium in the sponge titanium market dropped significantly.

Considering the gradual release of new capacity by sponge titanium enterprises and the time required for expanding downstream application fields, the cut-throat competition in the sponge titanium market has intensified. The remaining semi-process sponge titanium enterprises face increasing production pressure. SMM predicts that the demand for magnesium ingots in the sponge titanium market will remain stable in 2025.

Steel:

Currently, the primary desulfurization method in the industry involves desulfurizers made from magnesium powder, widely used in the pre-treatment stage of pig iron. Due to the relatively small magnesium powder consumption per ton of pig iron, the sharp rise in magnesium ingot prices has had a limited impact on the demand for magnesium powder in the steel sector. Considering the stringent production cuts in the domestic steel industry and the maturity of magnesium powder desulfurization technology, the application of magnesium in the steel sector is expected to continue declining in 2025.

Magnesium Ingot Export Market:

China's magnesium ingot exports in 2024 are expected to reach 260,000 mt, up 26.4% YoY. The biggest market concern this year was the magnesium ingot supply shortage reported by overseas customers in April. Due to the excessive drop in magnesium ingot prices before March, a sudden surge in restocking led to a sharp short-term price increase, significantly raising procurement costs for foreign traders. To avoid losses, overseas traders had to delay deliveries or cancel orders, disrupting market circulation and limiting overseas restocking. Meanwhile, some traders reported that price fluctuations in October led to advanced stockpiling, causing the overseas export market for magnesium ingots to face certain shrinkage from November-December 2024 to January 2025.

[Raw Materials]

China's magnesium industry primarily adopts the silicothermic reduction method, which heavily relies on coal. For ferrosilicon, a major cost component, electricity costs are closely tied to coal prices. Thus, coal price trends largely determine coal cost trends.

According to the latest data from the General Administration of Customs, China's cumulative imports of coal and lignite in 2024 reached 542.697 million mt, up 14.4% YoY. Overall, the higher-than-expected coal imports throughout 2024 were a key factor driving the continuous decline in domestic coal prices.

[2025 Market Outlook]

In the long term, there remain many uncertainties in the domestic magnesium market. On the supply side, the highly concentrated capacity of China's magnesium industry means production is significantly influenced by policies. Balancing policy coordination with industry development remains a pressing challenge. On the consumption side, this is a critical period for promoting magnesium alloy applications. Price instability is highly detrimental to promotion efforts, and the market urgently needs solutions to stabilize magnesium prices.

SMM analysis suggests that due to policy uncertainties and the immature pricing mechanism in the magnesium market, balancing green economic development with industry growth will remain a key focus for the magnesium market in 2025.