I. 2024 Non-Oriented Silicon Steel Price Review

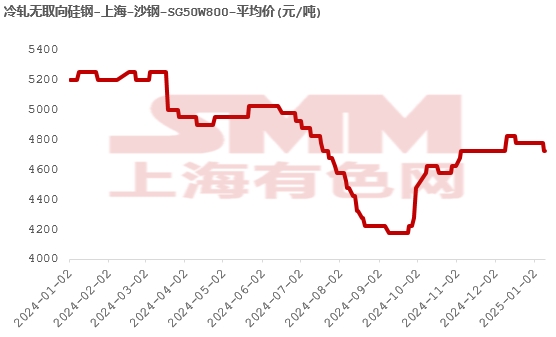

The price trend of non-oriented silicon steel in 2024 exhibited a "V" shape, with the overall price center moving downward.

Specifically: From January to March, non-oriented silicon steel prices fluctuated at high levels. The main reasons were: due to the impact of the Chinese New Year holiday, market trading sentiment was subdued. Additionally, the market at that time showed strong expectations but weak reality, with steel mills having a strong sentiment to stand firm on quotes, high market resource costs, and merchants generally maintaining a firm stance on prices. Therefore, from January to March, non-oriented silicon steel prices fluctuated at high levels.

From March to April, non-oriented silicon steel prices fluctuated downward. With the end of the Chinese New Year holiday, downstream manufacturing resumed production. Due to high inventory levels and consumption falling short of expectations, non-oriented silicon steel prices fluctuated downward overall.

From April to June, non-oriented silicon steel prices experienced a weak rebound. The arrival of the traditional consumption peak season provided bottom support to the market. Additionally, steel mills slightly cut production of non-oriented silicon steel in May due to poor order intake. As a result, from April to June, non-oriented silicon steel prices experienced a weak rebound.

From July to September, non-oriented silicon steel prices continued to decline significantly. At that time, the market faced significant inventory pressure, coupled with the arrival of the traditional consumption off-season. With strong supply and weak demand, high inventory levels led to fluctuating price declines for non-oriented silicon steel.

From September to December, non-oriented silicon steel prices bottomed out and then fluctuated at high levels. Under the dual conditions of continuous release of strong favourable macro front and tight supply-demand balance, non-oriented silicon steel prices rebounded rapidly after hitting bottom. In August, steel mills reduced silicon steel production, alleviating supply-side imbalances. Furthermore, in September, favourable macro policies were continuously released. Internationally, the US Fed announced its September FOMC meeting rate decision, cutting interest rates by 50 basis points, reducing the federal funds rate from 525-550bps to 475-500bps. Domestically, the PBOC implemented interest rate cuts and RRR cuts, marking the beginning of a monetary policy easing cycle. Additionally, by the end of 2024, manufacturing industries were rushing to fulfill export orders, leading to relatively strong overall consumption of non-oriented silicon steel. These combined factors resulted in non-oriented silicon steel prices bottoming out and then fluctuating at high levels from September to December.

II. 2025 Non-Oriented Silicon Steel Outlook

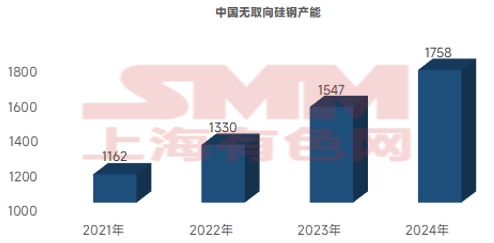

With the rapid development of China's manufacturing industry, the consumption of non-oriented silicon steel in China is also expected to show a trend of fluctuating growth, driven primarily by the incremental demand for automotive steel and home appliance steel, as well as stable and improving export performance. Meanwhile, China's non-oriented silicon steel capacity is also expected to grow steadily. Judging from the development trends of the manufacturing industry in recent years, non-oriented silicon steel has made significant contributions to the high-quality development of the domestic manufacturing industry, especially in providing strong support for the rapid growth of China's NEV industry in recent years. Looking ahead to 2025, China's overall capacity for non-oriented silicon steel is not expected to face shortages, and the supply-demand balance in the market for non-oriented silicon steel will still rely on dynamic adjustments in production to be achieved.

![Before the holiday, the black chain is unlikely to see a trend-driven market [SMM Steel Industry Chain Weekly Report].](https://imgqn.smm.cn/usercenter/zUFfM20251217171748.jpg)

![[SMM Chromium Daily Review] Inquiries and Transactions Weakened, Chromium Market Showed Mediocre Performance Before the Holiday](https://imgqn.smm.cn/usercenter/ENDOs20251217171718.jpg)