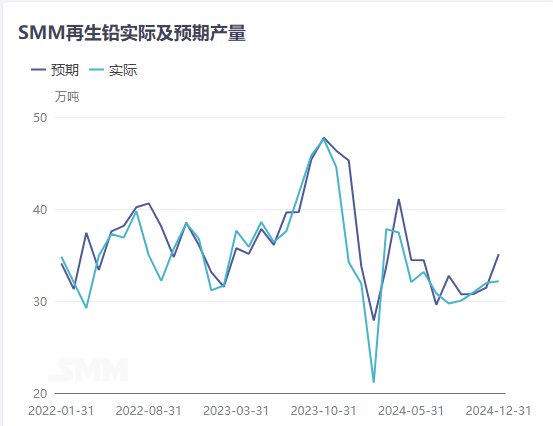

After Christmas, lead futures entered a downward fluctuation trend. Overnight, the most-traded SHFE lead 2502 contract hit a nearly one-month low of 16,305 yuan/mt before briefly bottoming out. Despite reduced primary lead supply in some regions and the slow recovery of secondary refined lead production in January, downstream consumption also weakened simultaneously. Some market traders expressed concerns about the expected inventory buildup of refined lead before and after the Chinese New Year holiday.

In the spot market, lead prices continued to weaken, directly impacting the cost support of secondary refined lead. Following the slight decline in battery scrap prices, secondary refined lead's comprehensive cost slightly decreased to around 16,450 yuan/mt. However, due to lower-than-expected secondary refined lead production in December, both supply and profit declined, leading to SMM secondary refined lead prices maintaining a premium over SMM #1 lead prices for several consecutive days.

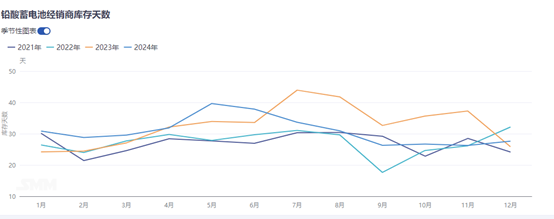

On the downstream operating side, the average spot lead price in December exceeded 17,000 yuan/mt, raising production costs for lead-acid battery enterprises. Among them, electric bicycle battery manufacturers increased battery selling prices, stimulating dealers to rush to buy amid continuous price rise and transfer inventory from enterprises to dealers. Entering January, the Chinese New Year atmosphere began to emerge in the lead market. Weakening lead prices, combined with early stocking by electric bicycle battery dealers, significantly dampened downstream consumption orders. Approaching the weekend, although logistics and transportation impacts had not yet started, many small and medium-sized battery enterprises indicated that pre-holiday stocking demand was nearly complete, with only minimal buying the dip expected later.

Looking ahead to January, with the Chinese New Year holiday approaching, downstream battery enterprises and dealers are expected to conduct their customary pre-holiday stocking in early January. By late January, as lead-acid battery enterprises generally enter the Chinese New Year break, operating rates are expected to decline, and just-in-time procurement demand will shrink accordingly. Recently, the spread between futures and spot prices has narrowed. Coupled with the limited availability of spot market supplies and high premium quotes from smelters in many regions, downstream enterprises tend to procure relatively cheaper local supplies, leading to a continued decline in social inventory before the holiday. With suppliers expected to offload stocks before the holiday, the pre-holiday inventory buildup of lead ingots is anticipated to remain low. Post-holiday, attention should still be paid to refined lead production schedules and pre-sale conditions during the holiday period, as the customary inventory buildup of lead ingots after the holiday cannot be ruled out.