SMM, January 7:

Entering January, Guangdong spot premiums rose from 535 yuan/mt to 595 yuan/mt. According to historical data, spot premiums/discounts in the market generally show a downward trend before the Chinese New Year. So, why did Guangdong premiums rise against the trend this year? This article will provide a detailed analysis from the perspectives of zinc price trends, downstream demand conditions, and inventory changes in Guangdong.

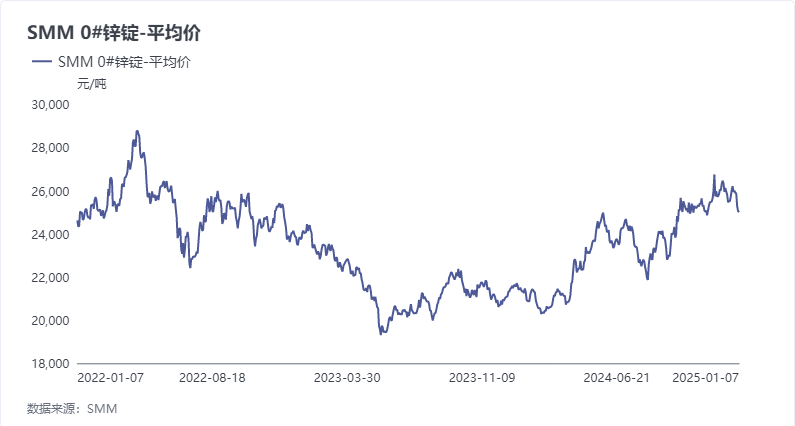

First, zinc prices in 2024 have shown an overall upward trend since early August, especially in November when prices reached an annual high. This caused many companies to fear high zinc prices, delaying orders in hopes of a price drop in the future to purchase at lower prices for fulfilling end-user orders. However, the sustained high zinc prices hindered production and delivery for enterprises. Recently, the SHFE zinc price center shifted below 25,000 yuan/mt, attracting some downstream companies to restock at lower prices, driving up spot premiums. Meanwhile, due to limited inventory from previous high-price purchases and the current zinc price dropping to around 24,500 yuan/mt, many companies opted for small-scale purchases to moderately replenish inventory in preparation for the Chinese New Year and post-holiday market demand. As a result, spot premiums in Guangdong continued to rise.

Second, in terms of downstream demand, Guangdong, as a major consumption area for die-casting zinc alloy, has shown a significantly higher operating rate compared to the same period last year. This is mainly due to zipper and small hardware orders being postponed to December because of weather conditions this year, coupled with the traditional peak season for automobile production and sales, and some enterprises ramping up to fulfill end-user orders. Last week, the operating rate of die-casting zinc alloy reached 57.4, up 12.18 percentage points YoY. For December, the operating rate recorded 47.56, up 5.41 percentage points YoY. The robust downstream consumption also contributed to the rise in premiums.

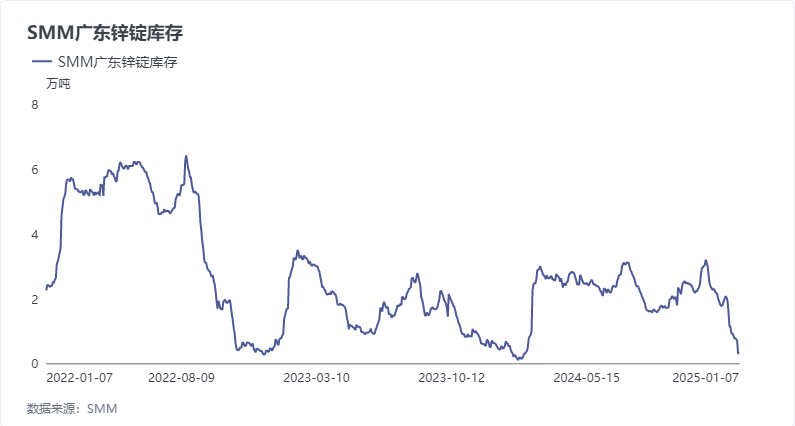

Third, from the current inventory perspective, Guangdong's total zinc ingot inventory decreased significantly from 7,149 mt last Friday to the current 2,856 mt. According to SMM's communication with enterprises, some Guangdong spot cargoes recently flowed into the east China market. Consequently, spot inventory dropped sharply, and with zinc prices declining while downstream demand remained, a supply-demand imbalance may occur. These factors have driven the continuous rise in Guangdong spot premiums, providing momentum for the increase.

In summary, current downstream demand in Guangdong remains, but reduced spot supply has led to rising spot premiums. Due to tight spot inventory, traders and producers are expected to raise premiums to manage inventory risks and ensure supply, which may result in reduced shipments or attract more cargo inflows. However, as this year's Chinese New Year comes earlier, many downstream enterprises and end-user factories are preparing for an early holiday, entering the countdown to the break. Therefore, Guangdong spot premiums are likely to fluctuate at highs but remain weak.