SMM, January 3:

As 2024 is coming to an end, 2025 is gradually unfolding. At this period, let us review the performance of the die-casting zinc alloy market in Q4 and look ahead to Q1. This article will focus on a detailed analysis of the overall operating situation, end-use consumption, and inventory.

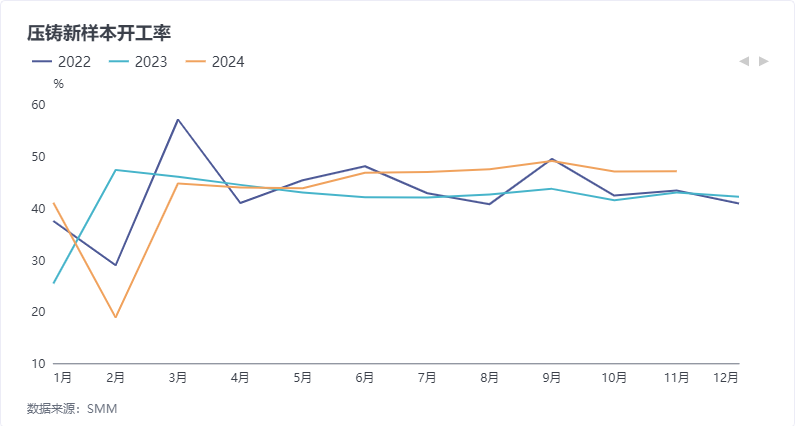

First, regarding the operating rate of die-casting zinc alloy enterprises, the average operating rate in Q4 was 47.81%, down 0.6 percentage points QoQ but up 11.89 percentage points YoY. Despite the QoQ decline, the Q4 operating rate was still significantly higher than the same period last year.

Next, from the perspective of end-use consumption, feedback from enterprises indicates that in Q4, apart from traditional Christmas export orders, downstream enterprises rushed to export to cope with potential tariff increases, driving demand for die-casting zinc alloy. In the real estate sector, as Q4 entered the off-season, the market remained stable. In the automotive parts sector, Q4 coincided with the traditional peak sales season for automobiles, and the high volatility of zinc prices had a relatively small impact on enterprises. Some enterprises saw increased orders due to participation in events such as the Canton Fair. In the clothing and luggage zipper sector, although the demand during the consumption peak in November did not improve, orders for such products began to increase in December as temperatures dropped in south China.

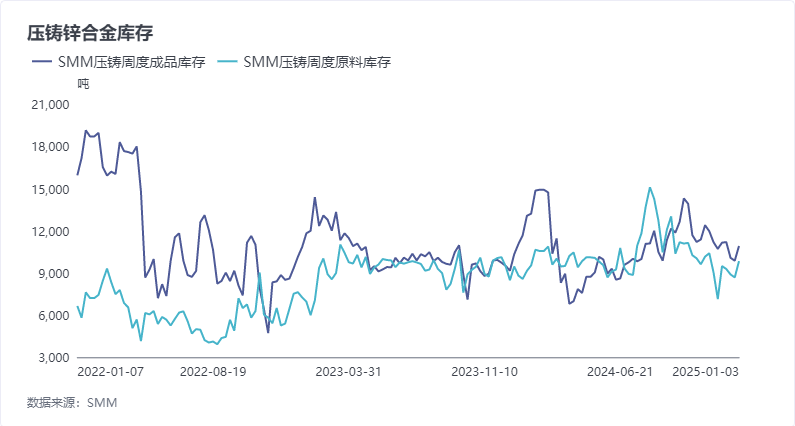

From the inventory perspective, overall inventory in Q4 decreased compared to Q3. The main reasons were that zinc prices were relatively high in Q4, and spot supply was tight towards the end of the quarter. Enterprises mainly focused on meeting basic needs through procurement or consuming existing finished product inventories. Additionally, some enterprises held a cautious attitude toward future end-use consumption, resulting in relatively low stocking willingness overall.

The Q1 situation can be analyzed from the following aspects:

First, during Q1, most enterprises take a holiday for the Chinese New Year. According to SMM, the planned holiday duration for most enterprises this year ranges from 12–30 days, averaging about 19 days, which is approximately six days shorter than last year's 25 days. Meanwhile, some enterprises reported that production workers currently show low acceptance of early resumption of work. Under the current high zinc prices, many enterprises are choosing to delay resumption until after the Lantern Festival, which is expected to significantly impact operating rates. However, as this year's Chinese New Year comes earlier than last year, January's operating situation may be lower than the same period last year, while February's overall situation may increase YoY.

Additionally, although Trump took office this year, the implementation of his specific tariff measures will still require some time. The "rush to export" situation among downstream enterprises after the Chinese New Year holiday is expected to continue.

As for terminal orders, with temperatures gradually warming in March, the real estate small hardware sector, which accounts for the largest proportion of downstream demand, is expected to receive some support, driving an overall rebound in operating rates.

In summary, the operating rate in Q1 2025 is expected to show a trend of first declining and then rising.