》View SMM Copper Quotes, Data, and Market Analysis

》Click to View Historical Spot Copper Price Trends on SMM

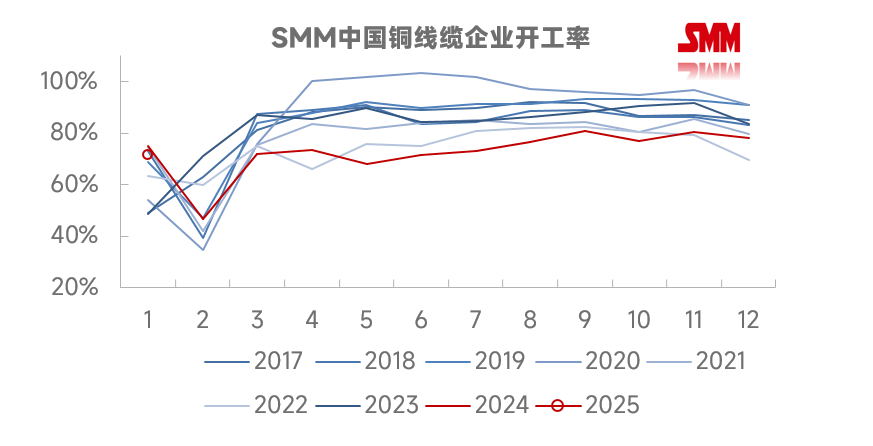

According to SMM, the operating rate of domestic copper wire and cable enterprises in December was 78.35% (surveyed 64 enterprises with a sample capacity of 3.643 million mt), down 2.33 percentage points MoM and 5.31 percentage points YoY, only 0.59 percentage points lower than the expected operating rate. Among them, the operating rate of large enterprises was 84.02%, medium-sized enterprises 59.39%, and small enterprises 43.59%.

Data Source: SMM

Overall, in December, industry orders for copper wire and cable enterprises showed a trend of rising first and then falling. In the first half of the month, rush-to-meet-deadlines demand from the end-use market emerged, and wire and cable enterprises actively pushed for higher output during this period, with new orders and operating rates both at high levels. However, in the latter half of the month, as the year-end approached, most enterprises in the industry chain faced the need for payment collection and account settlement, limiting the emergence of new orders, leading to a significant decline in operating rates. By industry, orders across all sectors increased, particularly in the power grid and new energy power generation sectors, which performed strongly in December. However, orders related to real estate, infrastructure, and other construction projects saw relatively limited growth. The raw material inventory/output ratio of copper wire and cable enterprises in December was 18.33%, down 1.04 percentage points MoM, while the finished product inventory/output ratio was 18.91%, down 1.82 percentage points MoM. As the year-end approached, some enterprises tightened inventory control to ensure cash flow, resulting in reduced raw material and finished product inventories in December.

In 2024, most copper wire and cable enterprises are expected to see a YoY decline in annual copper usage. According to SMM, the YoY decline in copper usage among copper wire and cable enterprises in 2024 will range from 3% to 50%. Larger enterprises with a higher proportion of power-related orders will experience relatively smaller declines, while smaller enterprises with a higher proportion of real estate and infrastructure-related medium- and low-voltage orders will be more severely affected.

SMM expects the operating rate of domestic copper wire and cable enterprises in January 2025 to decrease by 6.99 percentage points MoM to 71.36%, with a YoY decline of 3.74 percentage points. The Chinese New Year in January is the main factor affecting the operating rate of copper wire and cable enterprises. It is worth noting that since the 2025 Chinese New Year holiday spans January and February, the operating rate in January will be significantly higher than in previous Chinese New Year months. For 2025, most wire and cable enterprises expressed a lack of optimism. By industry, while power grid orders are expected to remain strong, uncertainty around new energy power generation orders is increasing, and orders related to real estate, infrastructure, and other construction projects are unlikely to improve. Overall, the total end-use demand will remain challenging. At the same time, the impact of aluminum products is intensifying. In 2024, most wire and cable factories reported a noticeable increase in aluminum-related orders, with some enterprises indicating to SMM that their aluminum cable orders could grow by 40% or more YoY in 2024. In 2025, under the backdrop of high copper prices, the impact of aluminum cables is expected to intensify further. Therefore, overall, copper wire and cable enterprises will continue to face numerous challenges in 2025, and industry reshuffling is far from over.