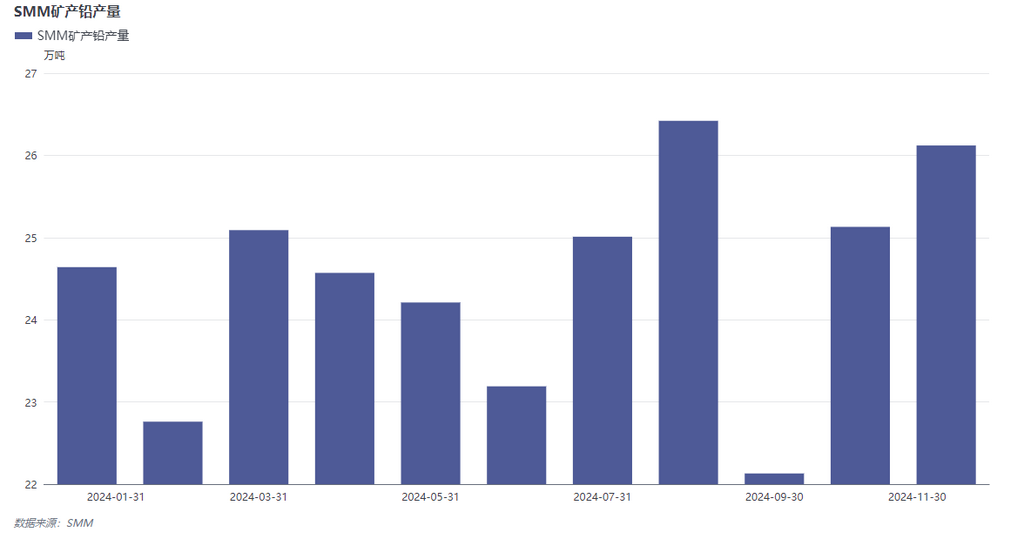

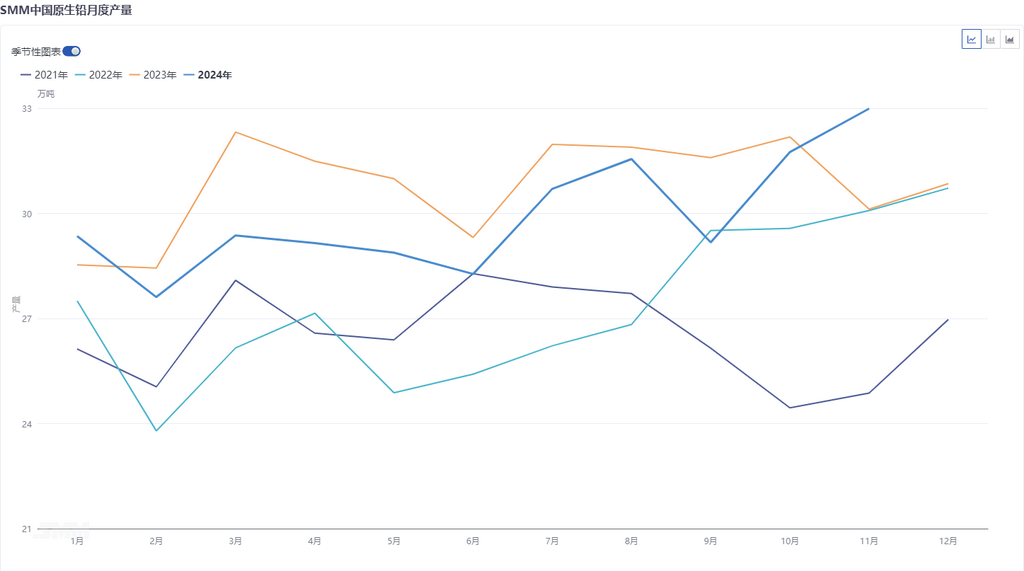

According to SMM production survey, the commissioning of new primary lead capacity in 2023 coincided with global lead-zinc mines falling short of commissioning progress expectations and record-high battery scrap recycling prices. In H1 2024, primary lead smelters faced cut-throat competition for raw materials. Some lead smelters shifted their operational focus to comprehensive recovery, with increased recovery of lead-containing materials from mining and smelting systems indirectly boosting the proportion of mine-sourced lead in smelters. Additionally, the annual production of primary lead in 2024 is expected to record a YoY decline.

After the technological transformation of raw material structures in primary lead smelters, many smelters have reduced their reliance on traditional pb50/pb60 lead concentrates. On one hand, the waste battery dismantling production lines commissioned by primary lead smelters have been operating steadily. Based on this change, excluding the non-mine-sourced lead production derived from the commissioning of new waste battery dismantling lines, SMM released the mine-sourced lead production data for primary lead smelters. According to SMM statistics, mine-sourced lead is expected to account for approximately 65% of primary lead in 2024. The import window has boosted smelters' enthusiasm for importing ores, and with the concentrated arrival of imported ores in Q4 2024, the proportion of mine-sourced lead is expected to rebound YoY. On the other hand, lead-containing comprehensive smelting materials within mine-sourced lead also play a significant role in the raw material structure of lead smelters. Due to regional advantages, such lead-containing materials (including copper, zinc, tin, antimony, and other minor precious metals) are applied more extensively in the South China market.