》View SMM Copper Prices, Data, and Market Analysis

》Subscribe to View SMM Historical Spot Metal Prices

During the month, Jiangxi Copper Corporation, China Copper, Tongling Nonferrous Metals, and Jinchuan Group finalised the 2025 copper concentrate long-term contract TC benchmark at $21.25/mt and 2.125¢/lb. The 2024 copper concentrate TC long-term contract benchmark was set at $80/mt and 8.0¢/lb.

However, following the conclusion of negotiations between Chinese smelters and Antofagasta, the negotiation results between Japanese smelters and Antofagasta are also imminent. According to market rumors, one Japanese smelter, with an annual trade volume of approximately 50,000 mt with Antofagasta, is likely to follow the $21.25 result. Another Japanese smelter, with an annual trade volume of 300,000-400,000 mt with Antofagasta, was among the first to agree on a $25 benchmark. The last Japanese smelter, with an annual trade volume of over 300,000 mt with Antofagasta, is still in negotiations and is demanding a benchmark above $30 for next year.

Historically, the benchmark figures quoted by Antofagasta/Freeport to smelters in China, Japan, and South Korea have remained largely consistent, with minimal differences. However, due to the significant supply-demand gap for copper concentrates next year, the forms and outcomes of long-term contracts have become more diverse. Since the last century, Japan and South Korea, with their advanced economies in Asia, had the largest demand for copper concentrates annually. As a result, Japan became the primary negotiator with Antofagasta/Freeport each year. With the subsequent economic growth of China and the expansion of its nonferrous metals industry, China replaced Japan as the primary negotiator with Antofagasta/Freeport. For a long period in the 21st century, smelters in Japan and South Korea had to accept the benchmark results negotiated between China and Antofagasta/Freeport. So why is there such a strong subjective stance from Japanese and South Korean smelters in this year's negotiations with Antofagasta?

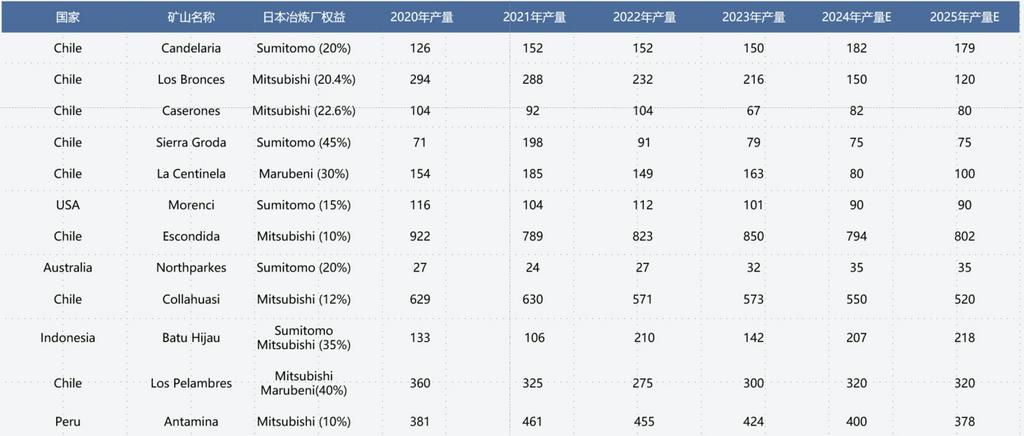

Japanese and South Korean smelters have long recognized the scarcity of domestic resources, which cannot meet the demands of their industrial development. As a result, smelting enterprises in Japan and South Korea began investing in mines in regions such as the Americas and Australia early on. However, instead of participating in mine dividends, they secured mining rights to address the issue of insufficient domestic resources.

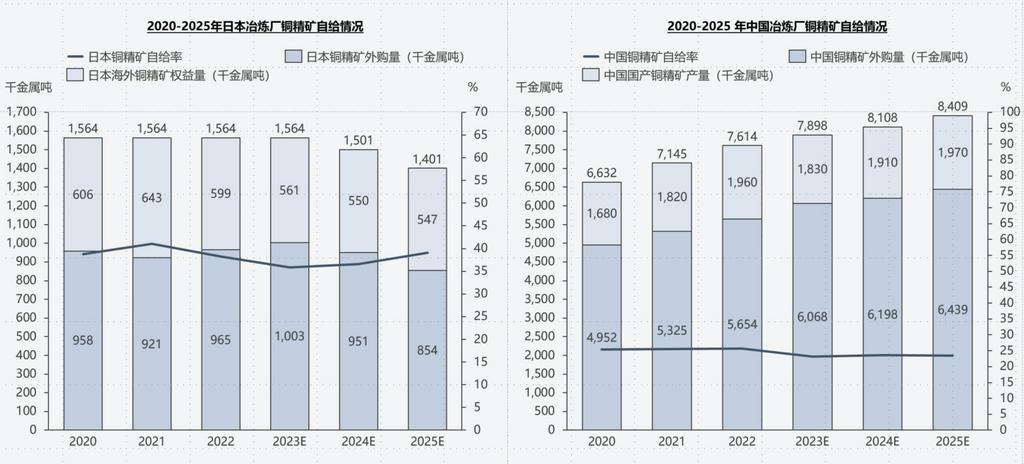

Comparing the raw material self-sufficiency rates of China and Japan, it is evident that Japan's copper concentrate self-sufficiency rate can be maintained at 40%-50%, while China's rate is only around 25%. In other words, the raw material structure of Chinese smelters is far more dependent on external sources compared to Japanese smelters. Therefore, Japanese smelters, compared to their Chinese counterparts, have greater leverage to negotiate a benchmark figure with Antofagasta when facing significant supply shortages in the future.

》Click to View the SMM Copper Industry Chain Database