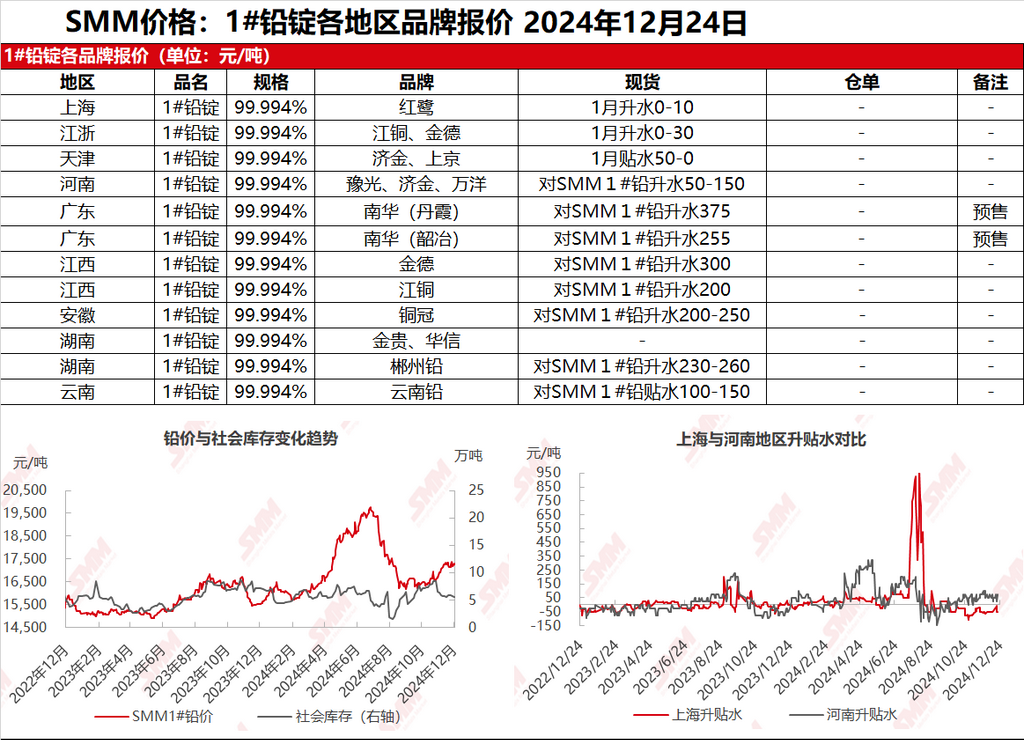

SMM, December 24: In the Shanghai market, Honglu lead was quoted at 17,340-17,385 yuan/mt, with premiums of 0-10 yuan/mt against the SHFE 2501 contract. In the Jiangsu and Zhejiang regions, JCC and Jinde lead were quoted at 17,340-17,405 yuan/mt, with premiums of 0-30 yuan/mt against the SHFE 2501 contract. SHFE lead pulled back slightly, while the impact of environmental protection on the supply side persisted. Additionally, some suppliers had sold out their December cargoes, resulting in limited spot market availability. Suppliers stood firm on quotes, generally offering at premiums over the SMM 1# lead average price. Meanwhile, secondary lead smelters increased their willingness to sell, with secondary refined lead quoted at discounts of 50 yuan/mt to premiums of 50 yuan/mt against the SMM 1# lead average price on an ex-factory basis. Downstream enterprises leaned towards secondary lead, and the primary lead market remained sluggish with muted trading activity.

Other markets: Today, the SMM 1# lead price dropped by 50 yuan/mt compared to the previous trading day. In Henan, suppliers showed significant differences in quotations, with some standing firm on quotes and reluctant to sell, but actual transactions were scarce. In Hunan, smelters had extremely limited circulating supply, and the situation of halted quotations after inventory depletion showed no improvement. Spot primary lead quotations maintained premiums of over 200 yuan/mt, with downstream buyers making small-scale purchases based on rigid demand. In Yunnan, small-scale lead ingot transactions were limited, and refined lead supply was locally tight. As year-end inventory checks approached, some downstream battery manufacturers postponed procurement, leading to overall weak market transactions.