Non-ferrous

Non-ferrous

Base Metals

Rare Earth

Scrap Metals

Minor Metals

Precious Metals

New Energy

Price CenterDatabaseProReportsEventsCar Insight

Language:

Language:

SMM1 March 14: yesterday, most of the outer disk metal market was green, Lun Copper fell 0.34%, Lun Zinc fell 0.48%, Lun Aluminum fell 0.62%, Lunni was flat, Lunxi fell 0.4%, Len lead rose 0.94%, London Metal Exchange (LME) copper rose slightly on Wednesday, helped by the prospect of low inventories and strong demand this year, but the strength of the dollar and the data released by China, a big consumer country, were lower than expected to limit the rise. In the domestic market, international copper fell 0.02%, Shanghai copper was flat, Shanghai aluminum fell 1.28%, Shanghai lead rose 2.09%, Shanghai zinc rose 0.1%, Shanghai nickel rose 0.18%, and Shanghai tin fell 0.53%.

The dollar index rose 0.32 per cent to 90.33 after briefly erasing gains after a strong 30-year Treasury bond issue, but investors adjusted their positions as the House of Representatives voted on the impeachment resolution. At the same time, Brainard said the current bond-buying plan was needed "for quite a long time".

U. S. stocks closed mixed on Wednesday, with the Dow falling slightly. Technology stocks led the Nasdaq and the S & P 500 higher. The US House of Representatives is about to vote on the second impeachment of US President Donald Trump. Treasury yields fell. The epidemic situation of novel coronavirus in the United States is still grim, with the number of deaths surging. The Fed's beige book said novel coronavirus's epidemic had rekindled optimism. The Dow closed down 8.22 points, or 0.03%, at 31060.47; the Nasdaq was up 56.52 points, or 0.43%, at 13128.95; and the S & P 500 was up 8.65, or 0.23%, at 3809.84.

In terms of crude oil, international crude oil futures closed lower on Wednesday, retreating from recent gains on fears that the intensification of the global novel coronavirus epidemic would dampen fuel demand. Analysts say fuel demand has rebounded from the pandemic shock last spring, but as the novel coronavirus epidemic intensifies, governments continue to impose travel restrictions that will dampen energy demand for months.

In precious metals, COMEX gold futures rose slightly on Wednesday as data showed rising US consumer prices and expectations that more fiscal stimulus measures from the Biden administration could boost inflation. Analysts point out that more stimulus is expected, higher-than-expected inflation and safe-haven buying driven by the US political environment are all supporting gold prices.

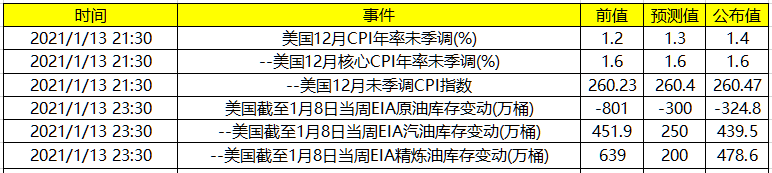

In terms of data, the monthly rate of CPI after the US quarterly adjustment in December, with a previous value of 0.20%, is expected to be 0.40%, and 0.4% is announced.

Forexlive comments on U. S. December CPI data: the data are in line with expectations, and the initial market reaction is lukewarm. Overall, wages and inflation are slightly higher, and at a monthly rate of 0.4%, the Fed will soon reach its 2% target. The real test moment will come between March and June, when the base effect will have a big impact.

Us EIA crude oil inventory (10,000 barrels) for the week to January 8, previous value-801, expected-226.6, announced-324.8.

Financial blog zero hedging EIA data: crude oil inventories fell slightly more than expected last week, but product inventories increased sharply. In line with the seasonal trend, gasoline demand is falling again, but this is much more serious than last year. Us oil production was expected to start to rise as oil prices rebounded above $50 and the number of drilling rigs continued to grow, but the data proved otherwise.

For queries, please contact Lemon Zhao at lemonzhao@smm.cn

For more information on how to access our research reports, please email service.en@smm.cn