Copper:

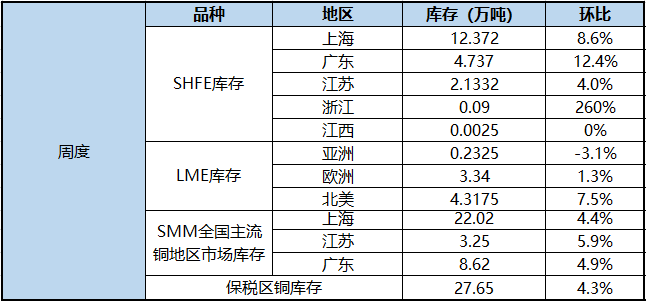

Fundamentals, LME copper stocks rose 3350 tons month-on-month to 78900 tons this week, still at an all-time low, while the market expects higher domestic consumption. Due to the long National Day holiday, downstream bargains have been prepared in advance since this week, and the procurement volume is expected to continue to increase next week. Domestic rising water continues to be strong, and there is also support for the disk. On the other hand, the domestic supply of scrap copper is tight, and the substitution effect of refined copper is also weakening. On the whole, the short-term macro stimulus to the copper price is more obvious, and it is difficult for the copper price to fall significantly under the expectation of loose liquidity. It is expected that Lun Copper will operate at 6700-6850 US dollars / ton next week, while Shanghai Copper will run at 51200-52500 yuan / ton.

Aluminum:

Electrolytic aluminum went to the warehouse smoothly in many places this week, and the weekly inventory of electrolytic aluminum in the domestic electrolytic aluminum society decreased by 24000 tons to 740000 tons. Nanhai and Gongyi contributed mainly to the decline, mainly due to the lack of arrival and the maintenance of warehouse delivery; the weekly inventory in Wuxi and Shanghai was tired, mainly due to the increase in arrival. While the arrival of aluminum bars increased out of the warehouse to maintain stability, the inventory of aluminum bars increased by 4000 tons to 67600 tons compared with last Thursday. Inventory in Foshan and Nanchang rose, while inventory in Wuxi, Changzhou and Huzhou declined.

Lead:

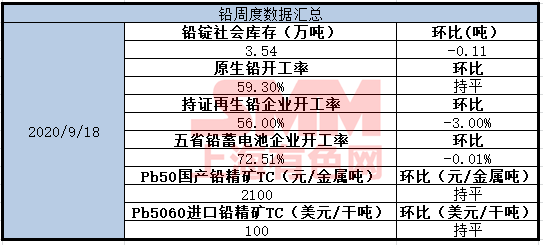

Shanghai lead has stopped falling and stabilized after a smooth decline for nearly a month, but the trend is downward and the technical trend is pessimistic. In terms of capital, the current rebound of Shanghai lead is mainly due to short positions, the buying intensity of long positions is low, the fundamentals are relatively stable at the supply end, the primary price difference for regeneration remains at the normal level, and the end consumption of electric bicycles weakens seasonally. car production still temporarily supports lead consumption, overall lead fundamentals are weak.

Zinc:

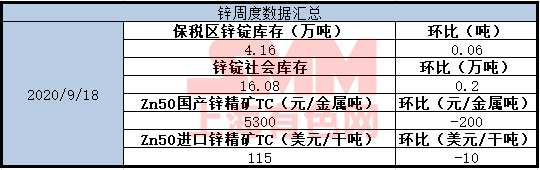

In the case of Shanghai zinc, due to the continuous decline in the quoted price of imported mines, the logic of tightening of mineral supply boosting the price logic is strengthening, and the early release of winter storage demand is also aggravating this tense atmosphere. Pessimistic expectations of zinc supply in the fourth quarter are gradually replacing consumption as the new price anchor, and this medium-term logic has not changed. In the short term, on the one hand, the Shanghai Zinc 2010 contract far exceeds the excess position in the same period in previous years, with warehouse receipts falling to about 19000 tons as of Friday, which is too low. At the same time, the price difference between far and near Synchronize expands the risk of corroboration. At the same time, the import window has successively reached the margin of profit and loss, and imported zinc may inflow and replenish. Coupled with the fact that the violent fall in zinc prices last week has already formed a certain overdraft on consumption, the release of reserve demand before the National Day may be restricted by the fact that the price is lower than expected, that is, the high point of going to the warehouse within the month has already appeared. Short-term fundamentals are intertwined, zinc is expected to run around 19400-20500 yuan / ton in the next cycle, and spot zinc in Shanghai is expected to rise 120-280 yuan / ton in October. Lun Zinc is expected to rise but not fall next week, running around 2430-2600 US dollars / ton.

Nickel:

As of Friday, the total inventory of pure nickel in SMM six places was 42313 tons, with a reduction of 1507 tons. Although the trading volume in Shanghai this week is less than that of last week, there is little import supply, so the inventory decline is enlarged. in terms of depots out of the warehouse, the inventory in Shanghai has been reduced by 1513 tons, of which Russian nickel warehouse receipt inventory has dropped by 1133 tons, while nickel beans have dropped by 1133 tons to 1600 tons. According to SMM research, a certain amount of Russian nickel and Australian nickel bean imports will be moved into the Shanghai social warehouse next week. Guangdong stock has a small amount of electroplated nickel supplies, inventory has increased. While the inventory in Liaoning and Tianjin in the north is in a state of net outflow, a small amount of Xinjiang Bofeng nickel is expected to enter the warehouse later this month. Inventories in Jiangsu and Zhejiang continue to be flat. To sum up, SMM original warehouse receipt spot inventory decreased by 1447 tons, SMM six pure nickel social inventory decreased by 1507 tons, and domestic pure nickel social inventory decreased for the second consecutive week.

Tin:

At the beginning of this week, the center of gravity moved down as a whole compared with last weekend, showing a concussion trend during the week. This week's futures were suppressed by the dollar, at a low position in a month, spot prices above the pressure is greater, a slight rise, demand will react fiercely, trading reduced. Last Friday, the transaction was positive, there was a little reserve downstream, and the transaction was general at the beginning of the week. Thursday belongs to the low of the week, and there is a decrease in inventory downstream, so the transaction is better. Due to the small brand price hesitation to sell, there is a small brand price gradually close to the cloud word, to Friday the two prices have narrowed to less than 500 yuan / ton. The rising discount is higher than that of last week. Yunxi Shengshui is more stable, and the small brand rising discount is close to Yunzi. On Friday, the set price of Yunxi, the 2011 contract for Shanghai tin futures, rose about 1500 yuan / ton, and Yunzi level water rose to 500yuan / ton, near the small brand level water.

2020 China Zinc Salt Industry chain Trading Summit

The eighth Zinc oxide Industry Summit Forum

Scan the code to participate in the meeting or apply to join the SMM zinc oxide industry exchange group