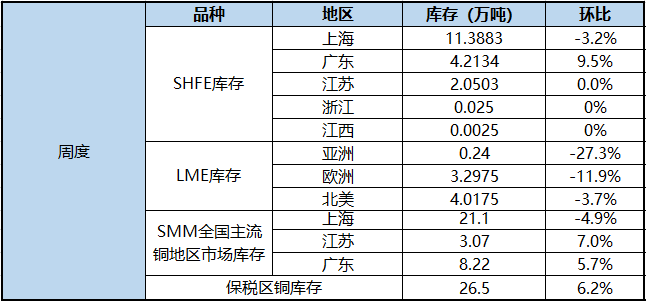

Copper:

Fundamentals, LME copper stocks this week still have a large extent of destocking, down 6900 tons to 75550 tons, but on Thursday ended 20 consecutive days of destocking, inventory increased by 2550 tons a day, the follow-up to continue to focus on overseas consumption persistence. Domestically, in order to catch up with the annual production target, refineries began to increase output in September, and with the subsequent introduction of new capacity, domestic copper production will increase significantly in the fourth quarter; while copper producers generally downgraded their forecasts for the traditional peak season in September, and no warming signals for Electroweb orders were observed in the first week of September, and it will take some time for domestic consumption to recover. In the short term, there is no significant change in fundamentals, and copper prices are more affected by macro sentiment and the trend of related assets. It is expected that Lun Copper will operate at 6550-6750 US dollars / ton next week, while Shanghai Copper will run at 51000-52000 yuan / ton.

Aluminum:

The weekly inventory of electrolytic aluminum continues to be small, and the weekly inventory of domestic electrolytic aluminum is 3000 to 764000 tons. The arrival of aluminum bars continued to be added to the warehouse to maintain stability, with inventories increasing by 3400 tons to 63600 tons compared with last Thursday. Inventory in Foshan, Changzhou, Huzhou and Nanchang all increased, with the largest increase in Nanchang inventory and only a slight decline in Wuxi inventory.

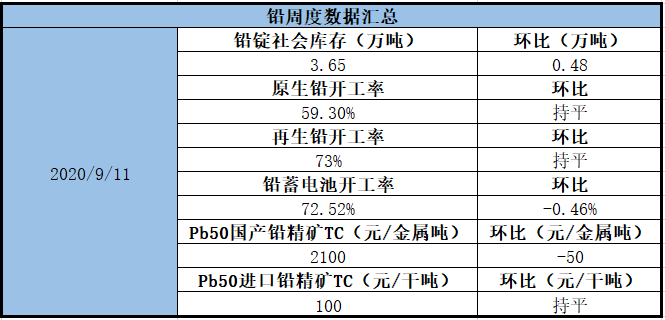

Lead:

Next week, China will mainly invest in fixed assets. at present, there are few bright spots in domestic fundamentals, stable production of primary lead at the supply end, good production profits of enterprises, and lower production profits of recycled lead enterprises. however, at present, the supply of waste batteries is relatively loose, the price of waste batteries follows quickly, the production costs of enterprises continue to move down, and lead prices always have room for shorting. In terms of consumption, at present, automobile consumption is recovering, and car batteries are relatively good, but the performance of electric bicycles is general. In the short term, there is limited room for consumption to continue to improve compared with the previous month. In the short term, it is mainly to maintain the current order, and the domestic fundamentals are relatively empty. Follow-up attention to the supply of waste batteries and the primary price difference.

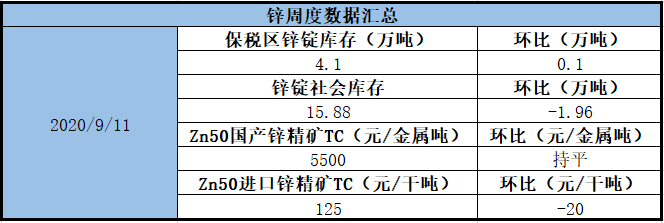

Zinc:

In terms of zinc in Shanghai, with the sharp fall in zinc prices and the release of downstream purchasing reserve demand, weekly inventory fell by nearly 20,000 tons, highlighting consumer resilience, and the price logic anchored by consumption has not been falsified. In terms of supply, according to SMM research, the monthly output of zinc ingots in September is expected to increase by more than 30, 000 tons, and the import window in mid-August may briefly open or guide a certain amount of imported zinc inflow. from two aspects, the supply pressure of zinc ingots in September can not be ignored. However, at present, the increase in domestic zinc ore production is relatively limited, the import offer price has been lowered to 100-120 US dollars / dry ton, the demand for winter storage has disturbed the market sentiment ahead of time, and the pessimistic expectation of zinc ore supply in the fourth quarter has gradually replaced consumption as a new price anchor. From an expected point of view, the outlook for zinc is more optimistic. From the perspective of returning to the fundamentals, the main force of zinc in the next cycle is expected to operate around 19000-20000 yuan / ton. It is expected that Shanghai zinc spot will rise 150-300 yuan / ton in October, and Lun zinc may rise low next week, running around 2360-2530 US dollars / ton.

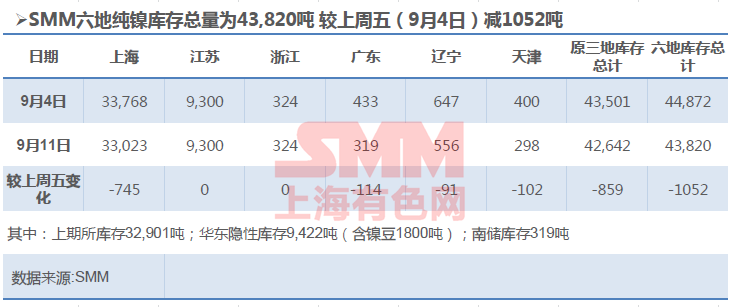

Nickel:

[the social inventory of pure nickel in SMM six is 1052 tons lower than last Friday] according to SMM, as of Friday, the total amount of pure nickel inventory in SMM six was 43820 tons, down 1052 tons from last Friday. This week, nearly 1600 tons of Russian nickel and 200 tons of nickel beans were stored in Shanghai. In terms of leaving the warehouse, due to a sharp correction in nickel prices, spot shipments of pure nickel have increased compared with last week, with nearly 2000 tons of pure nickel out of the warehouse, of which more than 700 tons to 1800 tons of nickel beans have been exported from warehouse. most of them are consumed by battery factories. In terms of Russian nickel, a large amount of warehouse receipt inventory was digested, but with the inflow of imports, the total amount was almost flat. In terms of domestic brands, most of Jinchuan nickel is sent directly to downstream factories after leaving the factory, and there is less supply flowing into Shanghai. In addition, inventory arrivals in Liaoning, Tianjin and Guangdong also decreased slightly, while inventories in Jiangsu and Zhejiang remained flat. To sum up, the spot inventory of the original warehouse receipt of SMM fell by 859 tons, and the social inventory of pure nickel in six places of SMM decreased by 1052 tons.

Tin:

There was a slight rebound at the beginning of the week compared with the weekend, with the dollar rising in mid-week spurred by positive US data in August, the overall metals market suppressed by a rise in the dollar, and tin prices rebounded sharply and began to fall all the way on Wednesday. Accordingly, as the downstream demand is still there, manufacturers also slightly raise the price, and the discount rises accordingly. At the same time, due to the low price of cloud word on the market, the price difference between small brand and cloud word narrowed. By Friday, tin prices basically returned to the levels of the end of last month and the beginning of this month, and the discount was higher than that of last week as a whole. On Friday, the set price of Yunxi, the 2011 contract for Shanghai tin futures, rose about 1500 yuan / ton, Yunzi level water rose to 500 yuan / ton, and the small card sticker rose 500 yuan / ton to flat water.

"Click to understand and sign up: 2020 China Automotive New Materials Application Summit Forum

Scan the QR code above to view the business cards of the participating companies and sign up online

Scan the code and apply to join the SMM Automotive Industry Exchange Group.