SHANGHAI, Sep 11 (SMM) – Inventories of rebar across Chinese steelmakers and social warehouses stood at 11.5 million mt as of Sep 10, down slightly by 0.7% from a week ago and up 49.4% from a year earlier.

Rebar inventories shrank slower than expectations in a high season which the market has been looking forward to, and rate of decline of rebar inventories is only 0.6 percentage points greater as compared to last week.

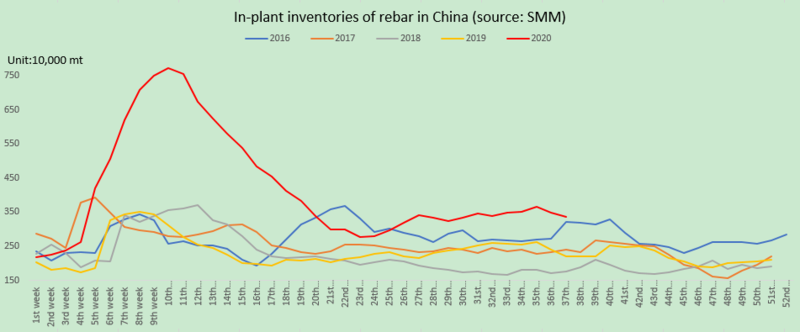

Inventories at Chinese steelmakers fell 112,900 mt on the week and stood at 3.37 million mt, down 3.2% from a week ago and up 53.3% from a year ago.

Profits saw a rapid decline (as of September 10, the average rebar profit stood at just -2 yuan/mt based on iron ore prices of $131.45/mt, according to SMM calculations), and rebar production has declined. The average rebar profit stood at less than 100 yuan/mt based on iron ore prices of $130/mt, and blast furnace (BF) steel mills stepped into the losses.

The funding and production limitation that missed expectations, as well as tensions between the US and China have weakened performance of rebar futures, suppressing market sentiment and dampening purchasing enthusiasm. Inventories at Chinese steelmakers declined 1.6 percentage points slower than last week.

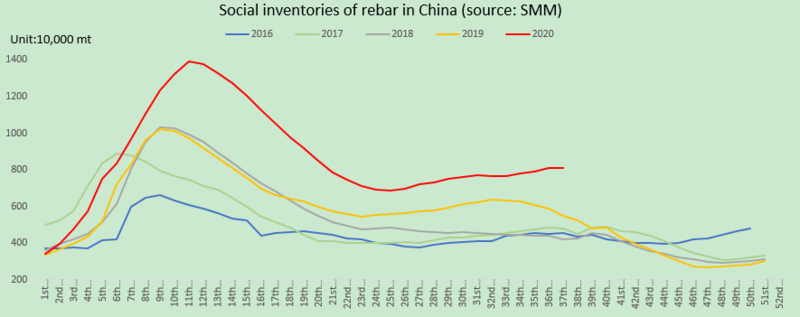

Inventories at social warehouses rose 29,900 mt on the week and stood at 8.12 million mt, up 0.4% from a week ago and 47.8% higher from a year ago.

In terms of settlement price, prices has dropped by nearly 100 points with weak performance of rebar futures since September 4, and the panic sentiment is increasingly felt in the markets. Cargoes are sold at low prices, leading to a slowdown of inventories accumulation. Demand has failed to meet market expectations, but demand has improved from a week ago. Inventories at social warehouses declined 1.7 percentage points slower than last week.

Rebar output remained high in the near term, and the inventories increased by about 50% year-on-year. The support from fundamentals was not very stable. Therefore, when inventories declined slower than expectations in a high season, the "strong expectation" that prompted the increase of prices in the early-stage will gradually turn into the risk of the downward movement of spot prices. Moreover, the continuous decline of rebar futures in recent days is just a sign of downside risk, and adjustment of prices is unlikely to be over.