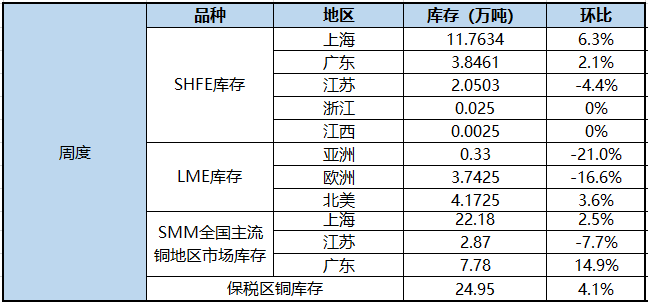

Copper:

Fundamentals, this week LME copper inventory to keep going to the warehouse, down 6900 tons to 82450 tons, the recovery of copper consumption in Europe is still an important support below copper prices; Chile earthquake news week once pushed Gao Lun Copper to a high of 6830, but the domestic copper production was actually unaffected, and as the impact of the epidemic subsided, the contradiction in copper supply gradually weakened; on the other hand, no signs of peak consumption season were observed in China, and the unsalable electrolytic copper continued to accumulate. On the whole, the fundamentals are intertwined and there are no marginal variables, and copper prices will follow the macro trend next week. While recent US economic data boosted the dollar index, non-farm data are expected to improve, while risk sentiment has been hit by the stock market, and copper price volatility is expected to test the support range next week. It is expected that Lun Copper will operate at 6550-6700 US dollars / ton next week, while Shanghai Copper will run at 51000-52000 yuan / ton.

Aluminum:

Electrolytic aluminum inventory, Sept. 3, weekly inventory is small, regional inventory differences continue to highlight, Gongyi, Shanghai contributed the main increase, domestic electrolytic aluminum social inventory accumulation of 6000 tons to 761000 tons. Aluminum rod arrival increment out of the warehouse to maintain stable aluminum rod inventory increased by 4000 tons to 60200 tons compared with last Thursday. Inventory in Wuxi, Changzhou, Huzhou and Nanchang all increased, with the largest increase in Nanchang inventory and only a decline in Foshan inventory.

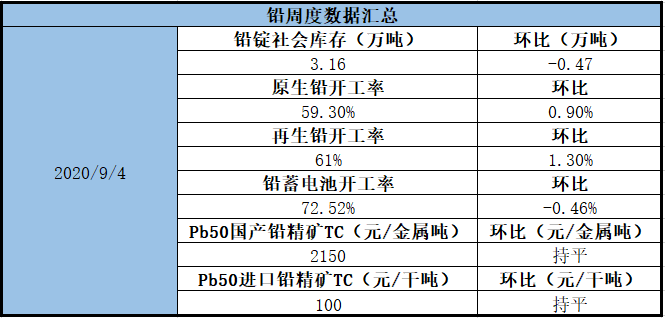

Lead:

Domestically, China releases inflation data next week, which is expected to have a limited impact on the market. Technically, lead has entered a downward trend, and the height of short-term technical rebound is limited. Fundamentally, the overhaul of the western mining industry affects the release of certain output, but as the output of the three refineries in Jiyuan, Henan Province returns to normal, the domestic electrolytic lead supply picks up steadily, recycled lead, the impact of solid waste method continues, some refineries suspend the purchase of waste batteries, raw material inventory is relatively tight, coupled with the current lower lead prices, declining regeneration profits, the willingness to continue to expand production in the short term is not high, after the completion of follow-up approval procedures, The situation of refinery production in this part. Consumption last August car sales maintained the same month-on-month increase, car consumption is still good, coupled with the National Day holiday, some big battery manufacturers plan to stock, consumption is still looking forward to, lead price fundamentals are still good, did not continue to deteriorate.

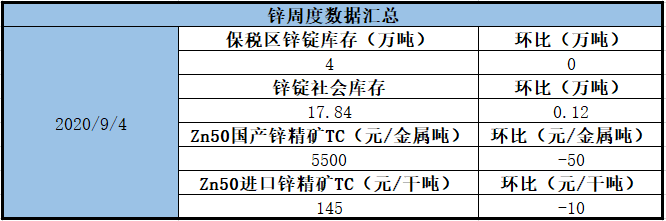

Zinc:

In terms of Shanghai Zinc, the drag on consumption by environmental protection in Tianjin has not yet ended, the domestic inventory records have slightly increased, and the upward logic of taking consumption as the anchor has been tested, but the export improvement brought about by policy-guided infrastructure consumption and the recovery of overseas consumption has not failed. Funds will wait and see carefully and sell short cautiously. Looking back to the supply side, the output of the smelter is expected to return to a high level in September. For domestic smelter production in the fourth quarter, the main restriction lies in the mine supply and the corresponding profit level. As the balance of domestic mines needs to be adjusted by imports, there is uncertainty as to whether the imported ore supply can improve as expected in the fourth quarter. Some smelters intend to take the lead in signing some winter storage supply contracts, and the winter storage demand is released ahead of schedule. Coupled with the low quoted price of imported mines, the mine supply side will provide lower support for zinc in the future. It is expected that the main zinc operation in the next cycle will be around 19500-20600 yuan / ton. It is expected that the spot price of zinc in Shanghai will rise by 90-160 yuan per ton in October. Lun Zinc may be in operation next week. In the range of 2440-2570 US dollars per ton.

Nickel:

The sharp correction in the prices of nickel and various metals is dominated by macro factors such as the collapse of US stocks and the appreciation of the US dollar, and there is a range of appropriate recovery and adjustment in the short term; the performance of nickel fundamentals is temporarily stable, but stainless steel prices tend to peak at a high level. the upward pressure on nickel prices will increase, but at the same time, the space for pullback is also limited; at present, the short-term fundamentals of nickel are good, and in the long run, they are better than expected. In the third quarter, 300 series stainless steel high output assist high nickel pig iron from leftover to deficient, fourth quarter or tight balance, the surplus is less than originally expected, so some nickel market fundamentals of nickel pig iron are good; in terms of pure nickel, although consumption is not good, however, the reduction of domestic nickel spot imports has a certain adjustment to the market, so that the domestic social inventory is basically balanced, and the market performance is relatively stable.

Tin:

Spot prices have also risen since the beginning of the week, when goods rose for four days in a row. There was a big increase during the week, and it was difficult for the downstream market to accept the daily rise in tin prices for the time being, mainly to consume existing factories and warehouses. Fluctuations are large and downstream consumption is not good, it is difficult for traders to ship goods, and at the same time, they are also more cautious in receiving goods. Although the futures price rose in the first four days, the spot demand is poor, the spot price is difficult to keep up, and the discount has shrunk slightly. Tin prices fell under pressure on Friday, giving up their gains in the previous three days in early trading. On Friday, the spot price of the water jacket rose about 500 yuan / ton for the Shanghai tin futures 2011 contract, about 500 yuan / ton for Yunzi sticker, and 1000-1500 yuan / ton for small card stickers.

"Click to sign up: 2020 Tin Industry chain Trading Summit

Scan the code to participate in the meeting or apply to join the SMM tin industry exchange group

![Platinum Prices Continued to Be in the Doldrums, with Moderate Trading in the Spot Market [SMM Daily Review]](https://imgqn.smm.cn/usercenter/obeMy20251217171735.jpg)