SMM9 March 2: yesterday, the outer plate of metal was all red. Lunxi rose 2.11%, Lunxi rose 1.47%, Lunnickel rose 1.44%, Lun aluminum rose 1.14%, Lun copper rose 0.13%, Len lead rose 0.05%, and (LME) copper on the London Metal Exchange climbed to a two-year high on Tuesday. Sentiment and expectations of strong demand for industrial metals were boosted by strong manufacturing activity data from China, the largest consumer, a weaker dollar and falling inventories. Domestically, shanghai zinc rose 0.77%, shanghai tin rose 0.56%, shanghai lead rose 0.41%, shanghai nickel rose 0.2%, shanghai copper fell 0.65%, and shanghai aluminum fell 0.93%.

In precious metals, COMEX futures edged higher on Tuesday, hitting a two-week high; at one point in intraday trading, it broke through the $2000-an-ounce mark, but closed with gains scaled back as better-than-expected US manufacturing data for August helped lift the dollar index from about two-year lows. The US ISM manufacturing PMI rose to 56 in August, the highest level since January 2019, as new orders surged, according to (ISM), the Institute for supply Management. After the release of the data, global stock markets rose, also putting pressure on gold prices.

The dollar index rallied yesterday and the euro fell on Tuesday afternoon as investors took profits after breaking the $1.2 mark for the first time since 2018, pushing the dollar back from a 28-month low.

U. S. stocks closed higher on Tuesday, with the Dow up more than 200 points and the S & P 500 and Nasdaq hitting new highs. Fed governor Brainard said the economy faces considerable uncertainty and still needs fiscal and monetary support. The US ISM manufacturing index in August reached its highest level since January 2019. The Dow closed up 215.61 points, or 0.76%, at 28645.66; the Nasdaq was up 164.21 points, or 1.39%, at 11939.67; and the S & P 500 was up 26.34 points, or 0.75%, at 3526.65.

On the crude side, NYMEX crude oil futures edged higher on Tuesday as better-than-expected U.S. manufacturing activity data boosted hopes of an economic recovery after the pandemic and analysts expected U.S. crude stocks to decline for the sixth consecutive week. Us crude oil inventories are expected to fall for the sixth consecutive week last week, and refined oil inventories will also fall, according to an in-depth survey released on Tuesday.

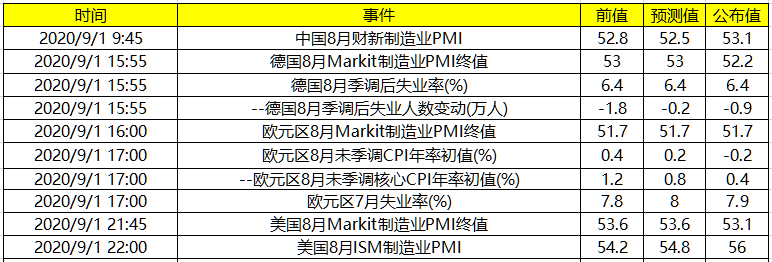

In terms of data, China's Cai xin manufacturing PMI, in August was 52.8, expected to be 52.6, and announced 53.1.

Wang Zhe, senior economist at Cai xin think tank: the economic recovery after novel coronavirus's epidemic continues, with both supply and demand improving synchronously, and overseas demand also strengthening. Employment is still the top priority, the expansion of employment depends on the longer-term improvement of economic prosperity, and the support of macro policies is essential, especially when there are still many uncertain factors in the economic operation at home and abroad. the relevant policies should not be significantly tightened.

The final value of German manufacturing PMI in August, the previous value is 53, expected to be 53, announced 52.2. Germany's unemployment rate after quarterly adjustment in August, with a previous value of 6.40%, is expected to be 6.40%, with an announcement of 6.4%.

The recovery of Phil Smith:, an economist at market research firm IHS Markit, is not widespread, and some German manufacturers are still struggling to cope with weak demand. The encouraging revenue figures mask the continuing woes of some industries, particularly machinery and equipment production, which are being hit by a lack of willingness to invest. Factory jobs continued to be lost at a disturbing rate in August, which is bad news for German domestic demand.

Euro zone manufacturing PMI final value in August, the previous value of 51.7, expected to be 51.7, announced 51.7.

In the month of Chris Williamson:8, an economist at market research firm IHS MARKIT, factory output in the eurozone rose strongly again, providing further encouraging evidence that production will rebound sharply in the third quarter after the collapse at the height of the COVID-19 epidemic in the second quarter. A key message of the latest survey is that companies are cautious about costs and spending, particularly in terms of investment and recruitment, where there are still concerns about the strength of future demand and uncertainty in the development of the epidemic.

The euro zone's initial annual CPI rate in August, with a previous value of 0.40% and an expected rate of 0.20%, was announced at-0.2%. The unemployment rate in the euro zone in July, previously 7.80%, is expected to be 8.00%, with a forecast of 7.9%.

The final value of Markit manufacturing PMI in the United States in August, the previous value of 53.6, expected to be 53.6, announced 53.1.

Chirs Williamson:, chief economist of market research firm IHS Markit, is encouraging that the inflow of new orders has improved significantly, outpacing the pace of production, making it difficult for many companies to produce enough products to meet demand, usually because of a lack of operational capacity. As a result, the backlog of unfinished work is growing at its fastest pace since early 2019, encouraging more and more companies to hire more workers.

The pre-PMI, value of ISM manufacturing in the United States in August was 54.2, expected to be 54.5, announced 56.

Institutional comments on US ISM manufacturing PMI: US manufacturing activity accelerated to a more than one-and-a-half-year high in August as new orders surged, but employment still lagged behind, supporting the view that the job market recovery has lost momentum. The data showed that the US ISM manufacturing PMI rose to 56 in August, the highest level since January 2019. But the continued improvement in manufacturing has been uneven, with the COVID-19 pandemic leading to a shift in spending from equipment for service industries such as restaurants and bars to goods such as household appliances.

"Click to sign up: 2020 Tin Industry chain Trading Summit

Scan the code to participate in the meeting or apply to join the SMM tin industry exchange group