SMM: the 12th meeting of the standing Committee of the 13th National people's Congress of the people's Republic of China adopted the Resource tax Law of the people's Republic of China on August 26,2019.The new tax law will come into effect on September 1, 2020. at the same time, the interim regulations of the people's Republic of China on Resource tax issued by the State Council on December 25, 1993 shall be annulled.

Compared with the resource tax system, the main changes in the resource tax law are as follows:

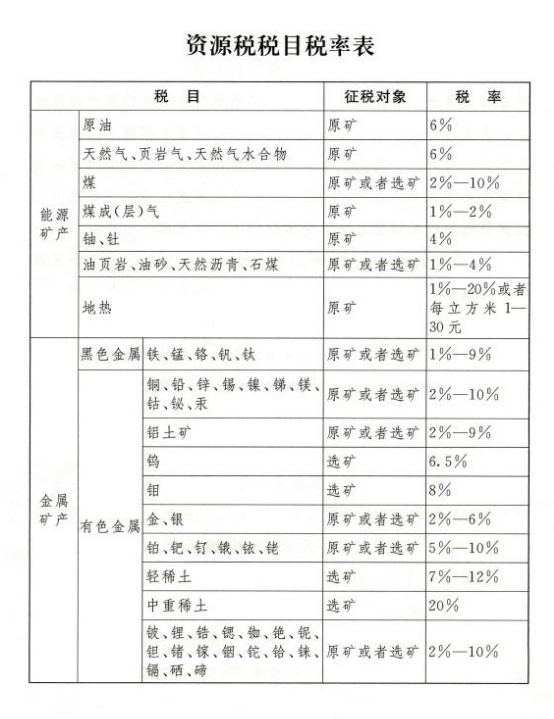

First, unify the tax items. Tax items will be uniformly standardized, and all taxable resource products will be listed in the tax law one by one, with a total of 164 tax items, covering all minerals and salts that have been discovered.

Second, adjust the limits of authority determined by the specific tax rate. The Resource tax Law continues to adopt two types of tax rates: fixed tax rates and range tax rates. for resources that implement the statutory principle of taxation, it is clear that the specific applicable tax rates shall be proposed by the people's governments at the provincial level and submitted to the standing Committee of the National people's Congress at the same level for decision.

Third, standardize the policy of tax reduction and exemption. The tax law has made clear provisions on the preferential policies that have been implemented for a long time and have been proved to be effective in practice.

The change of Resource tax in Metal Industry and its influence

Copper:

According to SMM, the detailed rules for the implementation of the interim regulations of the people's Republic of China on Resource tax, which came into effect on November 1, 2011, adopts ad valorem levy on copper ore, while the latest resource tax law adopts ad valorem levy on copper ore.

You might as well make a brief calculation. Based on 0.8% of the copper content in the original copper ore, the copper mine should be levied a resource tax of 1 / 0.8% 66,750 yuan / metal ton according to the original interim regulations; according to the new resources law, a resource tax of 5300002% "88.5%" 938.1 yuan / metal ton will fluctuate with the copper price, but on the whole, the resource tax will be higher than before.

In addition, SMM believes that the reform of resource tax collection will also have the following effects:

1. The production cost of polymetallic mines is expected to increase. The original ad valorem levy only needs to levy resource tax according to the original ore weight, which in disguise saves the cost of by-product metals in polymetallic minerals, but after the ad valorem levy, different metal minerals are required to pay resource tax, so this part of the cost will be increased.

two。 Part of the cost of the enterprise that only produces the raw ore for sale will be reduced, and when the resource tax is levied according to the original volume, the original mine production enterprise will have to bear the resource tax, while after the ad valorem levy, the resource tax of the mineral processing value-added part will be borne by the mineral processing enterprise.

Although the cost of copper production enterprises has increased to a certain extent after the implementation of the new resources tax, considering that the current high copper price is beneficial to mining enterprises, and the pricing coefficient of domestic copper concentrate is already high due to tight supply this year, it is expected that the implementation of the new resource tax law will have little impact on the trading end coefficient of domestic copper concentrate. "View full text

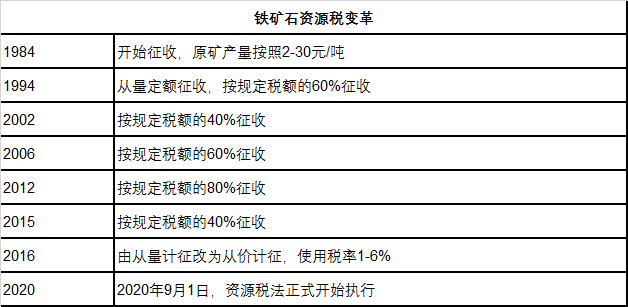

Iron ore: China's iron ore resource tax was levied on an ad valorem basis in the past. In the past 20 years, the iron ore resource tax has also been adjusted many times, and the reform of the iron ore resource tax has been comprehensively promoted since July 1, 2016. the iron ore resource tax is levied from the ad valorem of the original ore to the ad valorem of fine powder. Starting from September 1, 2020, the Resource tax Law of the people's Republic of China has been formally implemented. Compared with the previous interim regulations on resources tax, the resource tax law unifies the tax items, adjusts the specific tax rate, and standardizes the tax reduction and exemption policy.

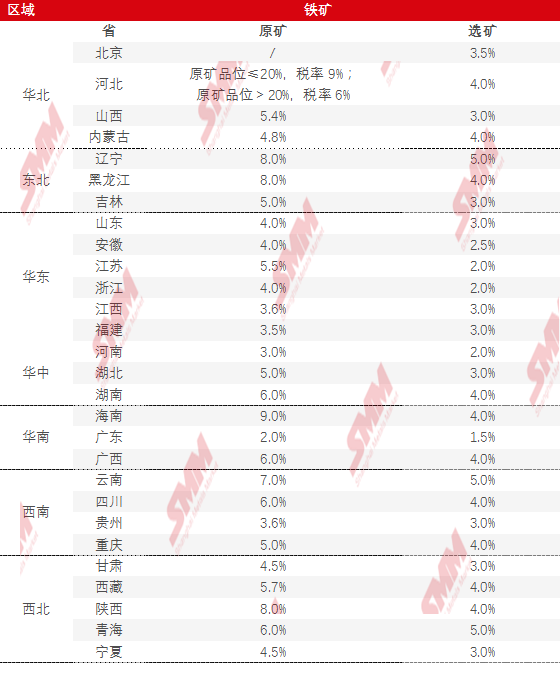

In addition to the Xinjiang region, the other 28 provinces and cities have announced the applicable tax rates for raw ore and mineral processing:

Compared with the interim regulations:

1) SMM compared the latest tax rates and found that concentrate tax rates rose from 3 per cent to 4 per cent in Hebei, from 5 per cent to 4 per cent in Inner Mongolia, from 4 per cent to 5 per cent in Qinghai and from 2.5 per cent to 3 per cent in Fujian, which are basically the same in other provinces and cities.

2) in the interim regulations, only the tax rate on the concentrate is stipulated, and the raw ore part is converted. Shandong Jinling Mining Industry said that if they produce both iron ore and iron concentrate, the amount of tax paid on the raw ore needs to be converted to calculate, which is more complicated. Two tax rates are stipulated in the Resources tax Law.

3) many domestic iron ore dressing enterprises sell raw ore by mixing purchased raw ore with self-mining raw ore, or by mixing purchased mineral processing products with self-produced mineral processing products. Therefore, the resource tax law clearly stipulates the amount of deduction and avoids double calculation. When calculating the sales volume or sales quantity of taxable products, the purchase amount or quantity of purchased raw ore or mineral processing products purchased shall be directly deducted. The amount of purchased taxable products allowed to be deducted (quantity) = the purchased amount of raw ore (quantity) × (applicable tax rate for raw ore in this area / applicable tax rate for mineral processing products in this area)

According to the Resource tax Law, enterprises can have certain preferential policies in the following five situations:

1. If a taxpayer suffers heavy losses due to accidents or natural disasters in the process of mining or producing taxable products, the resources tax may be reduced by 50% of the loss amount, but the maximum amount of tax reduction shall not exceed the resource tax payable in the year in which he suffered heavy losses.

two。 If taxpayers mine symbiotic mines, and the sales of symbiotic ores and main ore products are accounted separately, the symbiotic mines shall be subject to a 10% reduction in resource tax;

3. If taxpayers mine associated mines, and the sales of associated mines and main ore products are accounted separately, the associated mines shall be exempted from resource tax.

4. Taxpayers' mining of low-grade ores will reduce the resource tax by 50%;

5. Taxpayers shall be exempted from resource tax when mining tailings.

Specific implementation and impact, SMM will continue to follow up.

Rare earths: in the resource tax law, the fixed tax rate for medium and heavy rare earths is reduced from 27% to 20%, while the floating tax rate for light rare earths is 7% 12%, and the specific tax rate is determined by the people's government at the provincial level. Among them, Baotou mine tax rate is 11.5%, Sichuan mine is 9.5%, Shandong mine is 7.5%.

Some companies said that the tax rate on medium and heavy rare earths has been reduced by 7 percentage points, which will reduce the cost for mineral processing enterprises, or affect the price positioning of medium and heavy rare earth products in the later stage.

More metal items related interpretation will be updated later, please refresh it later.

State Administration of Taxation: some problems in the Collection and Management of Resource tax

In order to standardize the collection and management of resource tax, in accordance with the Law of the people's Republic of China on Resources tax, the Law of the people's Republic of China on the Administration of tax Collection and its implementation rules, and the notice of the Ministry of Finance on the implementation of issues related to Resource tax (No. 34 of 2020) and other relevant provisions, the relevant matters are announced as follows:

1. Where taxpayers sell raw ore by mixing purchased raw ore with self-produced raw ore, or by mixing purchased mineral processing products with self-produced mineral processing products as mineral processing products, when calculating the sales or sales quantity of taxable products, directly deduct the purchased amount or quantity of purchased raw ore or purchased mineral processing products.

Where a taxpayer sells mineral processing products by the mixed washing processing of purchased raw ore and self-mined raw ore, the deduction shall be made in accordance with the following methods when calculating the sales or sales quantity of taxable products:

The amount of purchased taxable products allowed to be deducted (quantity) = the purchased amount of raw ore (quantity) × (applicable tax rate for raw ore in this area / applicable tax rate for mineral processing products in this area)

If the deduction cannot be calculated in accordance with the above-mentioned method, the deduction shall be carried out in accordance with other reasonable methods determined by the competent tax authority.

2. When declaring resources tax, taxpayers shall fill in the Resource tax return (see attachment).

3. Taxpayers shall enjoy the preferential policy of resource tax and adopt the method of "self-discrimination, declaration and enjoyment, and retention of relevant materials for reference", unless otherwise stipulated. Taxpayers shall be legally responsible for the authenticity and legality of the materials retained in the preferential matters of resource tax.

4. Announcement of the State Administration of Taxation on promulgating the revised provisions on Resource tax (No. 63 of 2011), notice of the State Administration of Taxation on the publication of tax returns on Sino-Foreign Cooperation and Offshore self-operated Oil and Gas Fields (No. 3 of 2012), announcement of the State Administration of Taxation on several matters concerning the implementation of preferential policies of Coal Resources tax (No. 21 of 2015, Announcement of the State Administration of Taxation No. 31 of 2018), notice of the State Administration of Taxation on issuing revised Resource tax tax returns (No. 38 of 2016), notice of the Ministry of Natural Resources of the State Administration of Taxation on the implementation of preferential policies for Resource tax Reform (No. 2 of 2017, The State Administration of Taxation notice No. 31 of 2018 revised), the notice of the State Administration of Taxation on the promulgation of regulations on the Collection and Administration of Resource tax (No. 13 of 2018), and the notice of the State Administration of Taxation on Local tax categories and related additional tax reduction policies for small-scale value-added tax taxpayers. (No. 5 of 2019) the resource tax return issued by the State Administration of Taxation shall be annulled at the same time.

Attachment: resource tax return

Related readings:

"the domestic tin resource tax will be raised soon, and the willingness of domestic miners to ship goods will increase.

Click to sign up for the 10th Rechargeable lead Battery Industry Summit in 2020.

Please fill in your personal information on the last page and the meeting staff will contact you later!

Scan the code and apply to join the SMM waste Industry Exchange Group.

![This Week, Platinum and Palladium Experienced Significant Pullbacks, End-Use Demand Recovered, and Spot Market Trading Was Normal [SMM Platinum and Palladium Weekly Review]](https://imgqn.smm.cn/usercenter/obeMy20251217171735.jpg)

![Silver Prices Continue to Pull Back, Suppliers Remain Reluctant to Sell, Spot Market Premiums Hard to Decline [SMM Daily Review]](https://imgqn.smm.cn/usercenter/LVqfJ20251217171736.jpg)