SMM Network News: 1, the impact of the outbreak of the epidemic, gold and silver were greatly affected

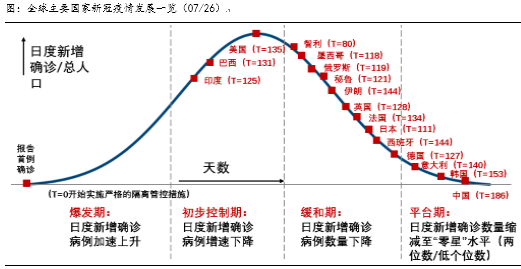

Since the beginning of the summer in the Northern Hemisphere, the global outbreak of novel coronavirus has been neither weak nor strong. At present, the domestic epidemic has been effectively controlled, but the spread of the overseas epidemic has accelerated. Novel coronavirus diagnosed a record increase of 1 million people within 100 hours! Since July, the number of new cases in a single day in the world has exceeded 200000 for the first time, and it has only been less than 200000 in five days. Data show that nearly 40 countries and regions around the world have recorded the highest number of confirmed cases of novel coronavirus in a single day.

Novel coronavirus's global pandemic constitutes a disaster, and the global economic system is facing the greatest threat since World War II in 1945. It is expected that the degree of world economic recession in 2020 will exceed that of the financial crisis in 2008. However, since the second half of the year, the new outbreak area of novel coronavirus has gradually shifted from developed countries in Europe and the United States to less developed regions such as South America, the Middle East and South Asia. This change has significantly reduced the negative impact of the epidemic on global economic growth, especially on the service consumption industry, and the market has temporarily ignored the impact of the outbreak in less developed areas on global economic growth.

For the supply and demand of the commodity industry, in today's economic globalization, any product may be the result of the division of labor and cooperation of the global industrial chain, and the epidemic is impacting the pattern of the global industrial chain. In particular, the transfer of hot spots of the epidemic has stimulated the speculation of supply disturbance themes to heat up, because among the strong metal varieties, including precious metals, a very high proportion of mining resources come from the worst-hit areas of the epidemic. At the same time, gold and silver surged to record highs, taking into account loose market liquidity, a rebound in inflation expectations and intensified games among big countries.

2. with the change of a hundred years, all parties scramble to buy gold and silver.

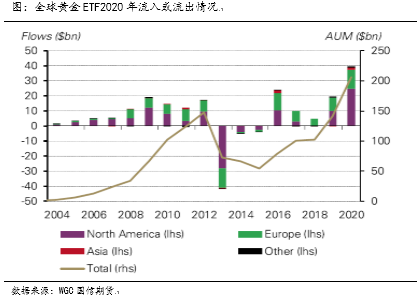

The global economic crisis triggered by the novel coronavirus epidemic has intensified great changes not seen in the world in a century, forcing global institutions and individual investors to seek value-protected assets to avoid risk. The demand for investment allocation of precious metals by institutional and individual investors continued to rise in the first half of 2020. At present, gold ETF in all regions of the world is a net inflow, of which North America accounts for 80% of the total global inflow. In the first half of the year alone, the total global gold ETF inflow exceeded 700 tons, equivalent to 45% of the global gold minerals in the same period this year, far exceeding the previous annual inflow records in terms of tonnage and net inflow value.

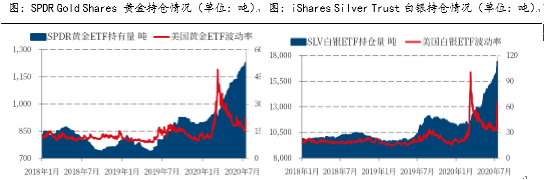

Data show that as of July 24, the gold position of the world's largest gold ETF SPDR Gold Shares was 1228.81 tons, an increase of 49.91 tons from the end of June 2020, setting another all-time high. Silver holdings of the world's largest silver ETF iShares Silver Trust was 17379.97 tons, an increase of 1890.21 tons from the end of June 2020 and an all-time high. The flow of gold and silver ETF is usually one of the important indicators of investor sentiment, and US CFTC data also show a sharp rise in bullish sentiment in overseas futures markets since July, indicating that bullish sentiment in the gold and silver market is high.

3. Negative interest rates superimposed inflation expectations to support gold and silver

Gold is sensitive to the interest rate market of US Treasuries. as an interest-free asset, the holding cost of gold investors is the real interest rate. Because the higher the interest rate of the market currency, the higher the opportunity cost of holding gold. Therefore, the price of gold is inversely related to the real interest rate, and it is more sensitive to inflation expectations. At a time when the global real economy is waiting for the economy to restart and take a turn for the better, market inflation expectations have rebounded faster than long-term US Treasury interest rates, which reflect market expectations of the economic boom, prompting recent real interest rates to fall further, further reducing the opportunity cost of holding precious metals.

Data show that as of the week of July 24, US inflation expectations continued to rise to 1.49%, rapidly approaching pre-epidemic levels. Nominal interest rates on 10-year US bonds fell further, real interest rates were deeply negative, and the long-term average real interest rate on US Treasuries was-0.41%. It continued to hit an all-time low, and the 10-year real interest rate fell to-0.90%, an all-time low. In the future, it is expected that under the background that the Fed is likely to adopt the yield curve control policy, nominal interest rates will remain low for a long time, greatly limiting the further upward adjustment of real interest rates in the future, making the correction of gold prices relatively limited, and the upper rebound space is further opened.

It is worth noting that the price of crude oil, another important indicator reflecting market inflation expectations, has not strengthened with gold recently, which means that the inflation expectations implied in interest rates may not be firmly supported. If crude oil prices remain depressed, it is very likely that economic demand has not recovered in essence, and the current optimistic inflation expectations in the market may be falsified and downtrend, putting pressure on precious metal prices in the short term.

4. the weakening of the US dollar and the rise of risk aversion will push up gold and silver in the next step.

From a macro policy point of view, after several rounds of large-scale fiscal stimulus policies, the US fiscal deficit reached a record high, with a budget gap of US $864 billion in June, which was close to the annual deficit in fiscal year 2019, weakening the credit of the US dollar to a certain extent. In terms of fiscal policy, while the epidemic continues to spread, the US job market is still under great pressure. As the unemployment benefits subsidy program expires, the US Congress is formulating a new stimulus package of nearly trillion yuan, which will continue to release water loosely. In terms of monetary policy, the Fed's monetary overissue is far more than in the past, and the extremely loose monetary policy releases liquidity while producing negative spillover effect against the US dollar. At the same time, for the Fed's current record balance sheet of nearly US $7 trillion, although it has declined for four consecutive weeks, the main reason for the decline is the reduction in the amount of central bank dollar swaps and repurchase agreements, two short-term dollar liquidity instruments, which is not the result of the Fed's initiative to tighten monetary policy. Since late July, the Fed's balance sheet has begun to pick up. Overall, global easing stimulus expectations continue to provide support for gold and silver prices.

From the perspective of the US real economy, although the US real economy was repaired in June, the US economy began to face a new round of shocks after entering July. Us non-farm payrolls data rose by 4.8 million in June to a record high, while ISM manufacturing PMI rose to 52.6 in June, the highest level since April 2019. In the US, CPI became regular for the first time since the outbreak in June. Retail sales rose 7.5 per cent month-on-month in June than expected, and total retail sales have rebounded to close to February levels. However, considering that the economic data in June did not take into account the negative impact of the resurgence of the epidemic, employment and the real economy are still under great pressure. The number of job losses in the US at the end of the week rose for the first time in four months at the end of July, and the pace of marginal labour market repair slowed. And the epidemic continues to get out of control, the weekly unemployment benefit policy of $600 is nearing expiration, the willingness of the American people to spend weakens, and the US consumer confidence index fell sharply in July, wiping out almost all the growth in the past two months.

In terms of relative currency value, the 750 billion euro EU recovery fund was finally approved, becoming the largest economic rescue package in EU history, supporting the strength of the euro. As the foreign currency with the greatest impact on the dollar index, the dollar is therefore relatively weak. And under the impact of novel coronavirus's epidemic, the epidemic in Europe and Asia has been greatly alleviated, and the economic recovery has improved. However, after the United States restarted its economy too quickly in the early stage, the epidemic further spread. The number of confirmed cases in a single day is still at a high level of 60,000 to 80,000, with a cumulative diagnosis of more than 4 million. The performance of the real economy is relatively weak and bad for the dollar. And precious metals and other risky assets were sold off during the liquidity crisis in March, with the dollar index surging to a high of 103 in March. At present, dollar liquidity has returned to or even better than the pre-epidemic level, and the shift of dollar liquidity from shortage to easing has also led to the decline of the dollar index.

With the intensity of loose water release in Europe and the United States unabated, the US economic performance is relatively weak, and the fiscal deficit is high, the dollar index has weakened for five consecutive weeks. In July 2020, the dollar index fell from 97 to around 94, a new low in nearly two years. In addition, tensions in Sino-US relations have intensified, geopolitical risks have been highlighted, worries about the epidemic have been superimposed, and the market has a strong sense of risk aversion. At a time when real interest rates have fallen to new lows, a weaker dollar and a rise in risk aversion could be the main drivers of precious metals prices in the next stage.

5. The United States promotes the geopolitical game to intensify, and funds pour into gold and silver.

With the US election approaching, market uncertainties have increased, tensions in Sino-US relations have intensified in many ways, geopolitical risks have been highlighted, and market demand for risk aversion is strong. Driven by risk aversion, markets may no longer choose to hold dollars, driven by the weakening of dollar currency credit, in favour of non-dollar safe havens such as gold and Swiss francs. Other dollar-denominated commodities and other assets have also received more money. The dollar index may decline further in a highly uncertain geopolitical environment, and precious metals are expected to have more room to rise.

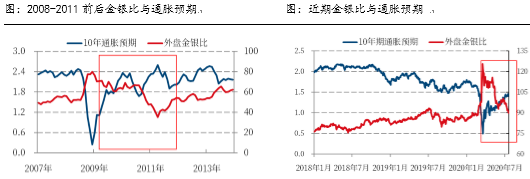

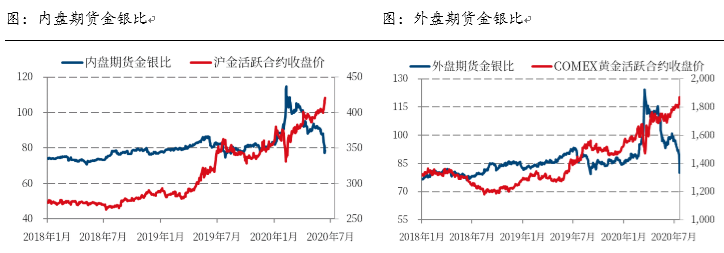

Judging from the overall performance of gold and silver in history, silver generally outperforms gold when inflation expectations pick up. At present, interest rates on long-term US Treasuries remain stable at low levels and inflation expectations continue to pick up, which is the most dynamic period for silver prices. If inflation expectations continue to pick up, there is room for the gold-to-silver ratio to fall further. In contrast to the situation in 2009-2011, a similar decline in the gold-to-silver ratio has occurred. At that time, 10-year inflation expectations in the United States were revised from 0.61% to around 2%, and the gold-to-silver ratio in the outer disk fell from an all-time high of nearly 80 at that time, falling to around 35 at its lowest point, while the spot gold-to-silver ratio in the inner disk fell from 76 in early 2009 to around 30 at its lowest point. At present, the gold-silver ratio of the outer disk has returned to the normal fluctuation range of 70-80 in the last three years, and it is estimated that there is still much room for gold and silver to decline in the medium and long term if history repeats itself.

Judging from the supply and demand of silver, Pan am Silver, the world's fourth-largest silver producer, announced in late July that it had suspended operations at two silver mines in Peru, which account for about 0.8 per cent of global silver production. According to the World Silver Association, the novel coronavirus epidemic caused a large number of mine production disruptions in major silver producing countries. This year, mineral silver production will drop by 7% compared with the same period last year, and the supply side will be greatly disturbed. On the demand side, the downstream applications of silver with industrial attributes are mainly photovoltaic (accounting for about 19% of industrial demand) and power batteries, and there is also a lot of demand in the 5G industry and the new energy vehicle industry. The recent development prospects of related industries are good, the industrial demand is strong, and silver still has the potential to rise.

5. the uncertainty of the external environment has increased, and the configuration value of precious metals has been highlighted.

Judging from the overall trend of precious metals, under the background of monetary easing and fiscal stimulus in Europe and the United States, inflation expectations have rebounded sharply, and there is a good chance that real interest rates in the United States will remain low in August. Under the influence of the spread of the epidemic, the performance of the real economy in the United States is relatively backward, the fiscal deficit is high, the negative spillover effect of monetary policy appears, and the dollar index may further weaken. And given the rising tensions in Sino-US relations, as the US election approaches, the global geopolitical landscape is highly uncertain, which will inspire more risk aversion in the future. The allocation value of gold as a "de-dollarized" asset is highlighted and may benefit from a weaker dollar and more room to rise in the market for safe-haven demand. In the long run, we continue to be bullish on gold and silver, and the long-term gold / silver ratio may decline further.

As far as the outlook for August is concerned, under the influence of recent geopolitical factors, market risk sentiment is more likely to cool in the short term, and the further rebound in inflation expectations under the early optimism may be suppressed. Silver may be difficult to further continue the strong rally in late July in the short term. If the pessimistic performance of the US real economy is hit by a second shock, the gold-to-silver ratio will not be ruled out rising again in the short term. Compared with the more flexible silver, gold rose more moderately, peaked later in the last precious metals bull market in 2008-2011, and is more resilient in extreme markets, and the value of gold asset allocation is expected to be further highlighted.

6. Gold and silver futures lead the rise again, focusing on the game trend of big countries in the short term.

On July 27th, gold and silver led a strong rise again. By the midday close, the main contract of Shanghai Silver 2012 rose 6.10% to 5708 yuan / kg, the highest since April 2013. the main contract of Shanghai Gold 2012 rose 2.87% to 430.86 yuan / gram, a record high. The main contract of COMEX gold rose more than 1.5% in August, and at one point it rose to $1938 / oz in intraday trading, breaking through the September 2011 high, while the main contract of COMEX silver rose nearly 6% in September, breaking through the $24 / oz mark.

From an event-driven point of view, the recent escalation of tensions between China and the United States shows no sign of easing. With the US election approaching, global market uncertainty has increased sharply, geopolitical risks have been highlighted, and funds are eager to seek safe-haven assets. In addition, the epidemic situation in the United States is grim, the number of people diagnosed in a single day is high, and the market demand for risk aversion is strong. Under the domestic and foreign difficulties of the US government, the impact of the weakening of dollar currency credit, coupled with a high fiscal deficit and ultra-loose interest rate policy, the dollar index will probably decline further in the future, and more institutions are expected to allocate more non-dollar currencies and precious metals assets as a safe haven, which provides more room for precious metals to rise.

In terms of policy trends, the Federal Reserve will release its July interest rate decision in the early hours of Thursday, and the market generally expects the Fed to continue to hold interest rates close to zero. Us Treasury Secretary Nooqin said he would formally launch a new $1 trillion bailout bill later today. Against the backdrop of a sharp rise in policy stimulus expectations in major economies led by the United States, market inflation expectations have risen sharply and real interest rates continue to hit new lows, providing impetus for gold and silver prices to hit record highs.

Generally speaking, under the circumstances that the geopolitical risks are highlighted in the current great power game, the dollar index continues to decline, inflation expectations pick up, and real interest rates are deeply negative, we continue to be optimistic about the asset allocation value of precious metals in the second half of the year. Short-term need to guard against market risk preference swings and long high settlement pressure. Make recommendations, firmly optimistic about gold bullish opportunities, unilateral pullback buying is appropriate, silver is more affected by market inflation expectations, short-term see more than move is appropriate, non-Jiancang customers are not recommended to buy to catch up, pay attention to risk control, band operation ideas.

Scan the QR code and join the SMM metal communication group.