SMM7 May 27: the LME metal market is all red this morning. As of 09:35, Lunni is up nearly 1%, Lunxi is up 0.9%, Lunzin is up 0.6%, Luncun Copper and Lunxi lead is up nearly 0.5%, Lun Aluminum is up 2%, domestic, Shanghai Tin is up nearly 2%, Shanghai Nickel is up nearly 1.7%, Shanghai lead is up nearly 1.1%, Shanghai Zinc is up nearly 0.5%, Shanghai Aluminum is up nearly 0.3%, Shanghai Copper is down nearly 0.4%. In China, Shanghai Tin rose nearly 2%, Shanghai Nickel rose nearly 1.7%, Shanghai lead rose nearly 1.1%, Shanghai Zinc rose nearly 0.5%, Shanghai Aluminum rose nearly 0.3%, and Shanghai Copper fell nearly 0.4%.

As for copper, as of Friday, the SMM copper concentrate index (weekly) was at $49.85 / tonne, down $0.050 / tonne from the previous month. Due to the possible deterioration of copper concentrate supply in Chile and Peru in the future, some traders are pessimistic about the follow-up supply and offer is lower than last week. However, most refineries are unwilling to accept the price below US $50 / ton of TC, so the spot market shows a stalemate. On the other hand, at present, the supply of negotiable goods in the market is also less, so the turnover in the copper concentrate market continues to be light this week. On the news side, the market focus is still focused on the supply interference of copper mines in South America. According to SMM, at present, the transportation sections from some mines to ports are still blocked, and they are shared by the surrounding large mines, or local troops are needed to intervene to clear the roads. After the economies of Chile and Peru have been hit by the epidemic, local instability has increased, posing a threat to the production and transportation of copper mines, and TC continues to be under pressure under tight copper supply.

[SMM Weekly selected] Peruvian Copper Mine Transportation blocked follow-up Copper Mine supply caused concern

In terms of aluminum, the contract price of 2008, the main force of Shanghai Aluminum, rose strongly last week (07.20,07.24), hitting a high near 14480 yuan / ton on Thursday, and fell somewhat near the weekend, so the position has been reduced for three consecutive weeks; Lunalco week shock rose, above 1700 US dollars / ton still-fixed resistance, the high of the week stopped at 1709 US dollars / ton. Against the background of the high Shanghai-Lun ratio, China's imports of foreign aluminum and aluminum products increased significantly in June. Lun Aluminum was relatively strong last week under the influence of comprehensive factors, but the continued upward momentum is not enough. It is expected to continue to test the size of the upper space this week. Or running between 1650-1720 US dollars / ton, it is necessary to guard against the impact of Sino-US diplomatic relations on the macro trading atmosphere.

[selected SMM Weekly report] Aluminum prices are consolidated at the 14500 yuan / ton mark and the domestic price of waste aluminum is stable.

In terms of lead, the fluctuation range of lead in Shanghai was relatively small last week, basically around the 20-day moving average. At the beginning of the week, Shanghai lead concussion rose, reaching a high of 15235 yuan / ton. in the next few days, Shanghai lead rose and fell, basically around the 20-day moving average, and finally reported at 14975 yuan / ton, an increase of 0.74%. China has entered the middle of the third quarter, downstream consumption has entered the expected peak season, consumption is worth looking forward to. The supply of waste battery is tight, the profit of recycled lead is low, even part of the loss, lead fundamental contradiction is low, the trend is relatively optimistic. Last week, the volatility of lead price is relatively large, coupled with the further narrowing of the price difference between recycled lead and primary lead, lead battery companies in the procurement of lead ingots, the preference for primary and recycled lead has changed. In terms of battery consumption, with the rise of low levels in some areas, such as signs of improvement in automobile battery replacement demand, increased purchasing enthusiasm of dealers, and steady increase in enterprise production.

[SMM Weekly report selected] lead consumption downstream is expected & waste batteries are relatively optimistic about the tight supply trend.

In terms of zinc, as far as Shanghai zinc is concerned, the trend of zinc prices in Shanghai maintained a wide range of fluctuations last week, the tension in Sino-US relations intensified, and the macro mood was negative. It is difficult for Shanghai zinc to hold the Wan Ba barrier. This week, the influencing factors of macro mood may be greater than the fundamentals. On the supply side this week, there are no new variables compared with last week, but mining and metallurgical negotiations are continuing, and another rise in zinc concentrate processing fees will boost the smelter's willingness to produce. In addition, the import loss narrowed slightly this week, and some zinc was imported into the market. Although it is difficult to open the import window this week, if the import loss narrows again, the inflow of imported zinc will still increase. From the consumer point of view, the current galvanized plate orders are the main support of the consumer side, relatively stable and improved, alloy and zinc oxide also have signs of external demand warming. On the whole, the efforts to remove the treasury since July are relatively strong, and the recovery of downstream consumption is more significant. On the technical side, MACD indicators want to become a dead fork, indicating that Shanghai zinc may be able to move down, but the lower 10-day moving average support is stronger, Shanghai zinc is expected to maintain a range shock next week. We still need to pay attention to the impact of macro on the price of zinc.

[selected SMM Weekly] the macro risk of strengthening Sino-US relations is expected to be difficult for zinc prices to continue to rise.

Nickel, last week, the fundamental contradiction is not prominent, all kinds of news broke out multi-short intertwined nickel prices continued high shock. The demand for pure nickel is not good, but there is less import supply last week. During the period of high nickel price correction, there is still purchasing action downstream of rigid demand, and the overall performance is OK; nickel pig iron and stainless steel are also stable, and nickel pig iron is in a state of balance between supply and demand in the short term. Stainless steel market recent shipment situation is OK, the fundamental contradiction is not prominent; The tension between China and the United States has intensified, the stock market and most commodities driven by bearish funds, the strength of safe-haven precious metals, and the general performance of overseas macro data; domestic policies to stimulate domestic demand, such as the transformation of old residential areas, and so on; Musk's speech advised nickel mines to increase production to provide material for emotional speculation.

[SMM Weekly selection] Nickel pig iron short-term market price may maintain stable operation downstream demand as the main influencing factor

With regard to zinc, it is expected that in the short term, Shanghai tin will fluctuate slightly upward along the five-day moving average, with the upper pressure level near the weekly high of 143700 yuan / tonne. We should pay attention to the impact of the development of Sino-US contradictions on macro investment sentiment, as well as the impact of the future on the downstream exports of the tin industry. In terms of liter discount, last week's spot on the Shanghai tin 2009 contract Yunxi and small card discount generally rose first and then suppressed, Yunzi basically returned to the vicinity of Pingshui, and the small brand discount expanded. Before last Thursday, due to the downward shift of the center of gravity of the market, the center of gravity of the discount rose at the beginning of the week. The price of tin in Shanghai on Friday was higher than that of the previous Friday, so the center of gravity of the discount on Friday was lower than that of the previous Friday.

[SMM Weekly selection] the support of the Shanghai-tin 20-day moving average is quite stable and is expected to fluctuate slightly upward along the five-day moving average in the short term.

In terms of black, the thread fell nearly 0.3%, the hot coil fell nearly 0.5%, stainless steel rose nearly 1.6%, coke fell nearly 0.5%, coking coal rose nearly 0.5%, iron ore fell nearly 0.8%, and the current price trend in the threaded period last week was not in line with each other. Spot prices are subject to the suppression of high inventories and high-cost stack to strengthen the support of expectations, up and down dilemma, narrow fluctuations. Futures continue to strengthen under the guidance of strong expectations. Then tensions between China and the United States escalated in half a week. Following the forced "eviction" of the Chinese consulate in Houston by the US side, China asked the US side to evacuate the consulate in Chengdu on Friday, causing the capital market to float green and the snail to dive.

The current prices of hot rolls last week all showed a fluctuating trend. Recently, the domestic macro side is good, superimposed at the beginning of the week iron ore and other raw materials rotated to stimulate, the overall black performance is more excited. However, compared with the hot futures market, the hot spot market appears to be relatively deserted, the spot price is insufficient with the rising power, and there is no volume phenomenon in the market transaction. Superimposed in the past two days, the friction between China and the United States escalated again, the stock market futures market was dragged down, and the market mentality weakened, so the overall spot market performance was lower than expected, mainly with shocks.

[SMM Weekly selection] Black Swan comes out again. What about the steel price next week?

Crude oil fell nearly 1.2 per cent in the previous period, boosted by some positive economic data, which rose slightly on Friday and fluctuated flat, up 1.7 per cent last week; the dollar's fall to its lowest level in nearly two years has boosted the attractiveness of dollar-denominated commodities; at the same time, fears of a slowdown in demand caused by rising inventories and a warming coronavirus epidemic have increased.

In terms of precious metals, Shanghai gold rose nearly 1.8 per cent and Shanghai silver rose nearly 1.4 per cent. Rising geopolitical tensions and concerns about global economic growth contributed to the rise in gold. Gold prices were also supported by factors such as low or negative real interest rates, a weaker dollar and rising inflation expectations.

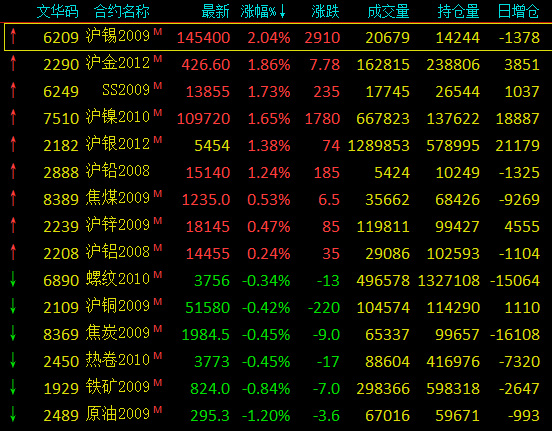

As of 09:35, the status of contracts in the metals and crude oil markets:

Brief comments on SMM:

Copper: last Friday night trading closed at 6400 yuan / ton, down 1.63%. Trading volume was 20, 000 lots, and long positions were reduced by 2056 to 314000 lots. Shanghai Copper 2009 contract closed at 51590 yuan / ton, up 0.72%, with trading volume of 84000 lots and short positions reduced by 74 to 113000 lots. After a sharp correction in copper prices on Friday due to strained relations between China and the US, Panlun copper fell all the way down in the afternoon, falling $140from above $6500 a tonne to an one-week low. Copper prices rebounded to recover some of their losses after a sharp fall in the evening, but then turned downwards, closing at $6400 a tonne. Copper prices fell on Friday as investors worried about a tense international situation and a potential stagnant economic recovery, risk aversion returned, COMEX gold hit a record high of $1937.5, and global stock markets fell, dragging copper prices down. Copper prices are expected to remain under pressure today, but they are underpinned by supply-side support and a $1 trillion fiscal stimulus package to be discussed in the US this week, raising expectations of easing in the US and Europe and a limited correction in copper prices. On the spot side, consumption is weak after entering the off-season, and traders are not willing to receive goods after the end of long order delivery, so although copper prices fall, rising water is expected to rise. It is expected to be 6350-6420 US dollars / ton for Lun Copper and 51800-52200 yuan / ton for Shanghai Copper today. It is expected that the spot water will rise to 20-90 yuan per ton today.

Aluminum: last Friday, the main contract of Shanghai Aluminum opened at 14495 yuan / ton in the morning, then fell continuously to around 14400 yuan / ton, then stabilized and fluctuated in a narrow range; the decline remained unchanged in the afternoon, the intraday low fell to 14305 yuan / ton, and then the V-shaped rebound returned to the top of 14400 yuan / ton, closing at 14405 yuan / ton at the end of the day, trading volume increased to 85000 hands, position reduced to 104000 hands, daily close of crosses. The total position in Shanghai Aluminum Futures decreased to 377000 lots, and the trading volume increased to 223000 lots. Last Friday night trading Shanghai Aluminum opened at 14420 yuan / ton, opened concussively and rose to a high of 14460 yuan / ton, then fell back to below 14400 yuan / ton, and closed at 14415 yuan / ton at the end of the day. Domestic fundamental demand is good, inventory is still relatively low, and the bullish effect of spot rising water on futures still exists. It is estimated that the main operating range of Shanghai Aluminum today is 14300-14700 yuan / ton.

Lead: last Friday, Shanghai lead opened at 14970 yuan / tonne. At the beginning of trading, Shanghai lead quickly rose to 15125 yuan / tonne. At the end of the session, Lun lead diving led to an accelerated decline in the domestic market. Shanghai lead was finally reported at 14945 yuan / ton, down 0.2 per cent. Shanghai lead continued high shock, continuous many daily newspapers increased the shadow line, the upward pressure is greater, short-term shock consolidation is mainly expected.

Zinc: last Friday, Lun Zinc recorded a negative column, below which jumped away from the support of each long moving average, and the positive column of MACD narrowed. Last Friday, LME inventory increased by 4450 tons to 154500 tons, or 2.97%. Against the background of the continuous fermentation of the overseas epidemic, trade disputes between China and the United States have resumed, the market risk aversion mood has risen, and Lunzinc is weak, but the decline has narrowed somewhat due to the positive data of total sales of new homes in the United States in June and manufacturing data in July. Pay close attention to the development of Sino-US trade in the short term. The price of lun zinc is expected to operate in the range of 2200-2250 US dollars per ton. Last Friday, Shanghai zinc recorded a positive pillar, the lower 10th line to provide support, KDJ indicators to become a golden fork. Macroscopically, the US data is good to drive, and under the background of domestic peak season consumption expectations, the social inventory is deconstructed faster, and the fundamental support is temporarily strong, boosting the trend of Shanghai zinc, but Sino-US relations increase short-term risk factors. The contract price of Shanghai Zinc 2009 is expected to operate in the range of 17900-18400 yuan / ton, and it is expected that the price of domestic Shuangyan zinc will rise by 60-70 yuan / ton in August.

Nickel: the overnight Shanghai Nickel 10 contract opened at 107620 yuan / ton last Friday. After the night trading opened, it continued the upward trend at the end of the day, and the bulls increased their positions by more than 10,000 hands. Shanghai Nickel pulled up through the 110000 mark to 110150 yuan / ton. The pass is post-holiday high, the pressure is strong, it is difficult for the bulls to rise, the bears take advantage of the opportunity to suppress, the bulls take profits, and the Shanghai nickel concussion falls below the daily average line, and the center of gravity revolves around 108800 yuan / ton until the close, which is quoted at 108660 yuan / ton. compared with the previous trading day, the settlement price increased by 1040 yuan / ton, or 0.97%, the trading volume was 572000 lots, and the position increased by 11000 lots to 130000 lots. Overnight, Shanghai nickel closed at the small positive pillar of the long upper shadow line, and the upper rail pressure level of 110000 and Boll line was detected on the shadow line, and a technical crossing was formed around 107200 yuan / ton below the 5 / 20 moving average. Today, we will pay attention to the shock between this position and the 110000 gate.

Tin: Shanghai tin trend: the Shanghai tin main 2009 contract opened at 141130 yuan / ton last Friday night, with a maximum of 144320 yuan / ton and a minimum of 141130 yuan / ton, closing at 144100 yuan / ton, up 2260 yuan / ton, or 1.59%. 14159 hands were traded and 14275 positions were held, a decrease of 1347 hands. Last Friday, the stock of the previous period was 2931 tons, 75 tons less than the same period of the period, and 2753 warehouse receipts, a decrease of 205 tons. Last Friday, after the main tin 2009 contract in Shanghai opened at 141130 yuan / ton, under the influence of short sellers, it fluctuated all the way up, with a slight pullback in intraday trading, and reached the highest point of 144320 yuan / ton in the late session. After reaching the peak, there was a pullback, closing at 141130 yuan / ton, showing a long positive line, and the solid part received 20-day moving average support, crossing the 5-day and 10-day moving average as a whole. The upper pressure level is expected to be near the previous high of 144600 yuan / ton.

"Click to sign up: 2020 Tin Industry chain Trading Summit

![China’s Copper Anode Imports Edged Up YoY in January-February 2026, with Growth Expected in Q2 [SMM Analysis]](https://imgqn.smm.cn/usercenter/XTMPt20251217171713.jpeg)