SMM7 March 23: at the 15th lead and Zinc Summit 2020 held by SMM, Dr. Wang Anzhi of Shanghai Cross-Cool Materials Technology Co., Ltd. brought you a keynote speech on "Green Metallurgy and New Materials-the Power of restructuring the Nonferrous Metals Industry chain".

The Challenge of traditional Industry chain of Nonferrous Metals

Wang Anzhi said: at present, the traditional industrial chain of non-ferrous metals has the characteristics of standardization, large scale, high energy consumption and heavy pollution, facing the complexity of raw materials: depletion and depletion of resources, and the pressure of environmental protection: the requirements of renewable energy and renewable resources. pollution-free production; the challenge of the impact of new materials and technologies on the market.

Restructuring path of non-ferrous metal industry chain

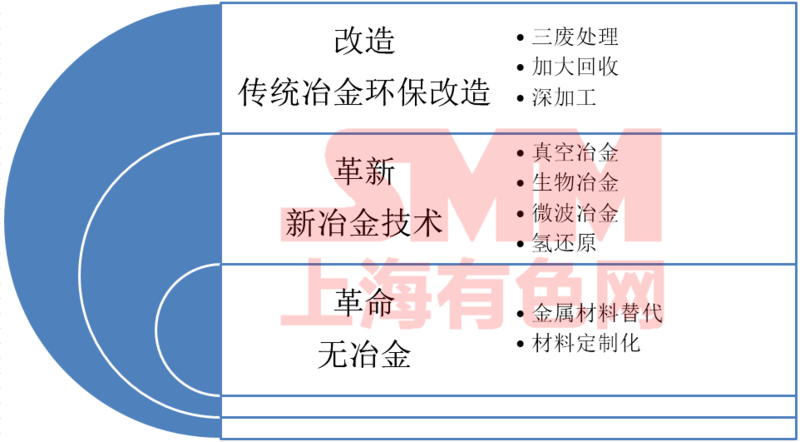

The Power of the restructuring of Nonferrous Metals Industry chain-Green Metallurgical Technology and New Materials

Green metallurgy technology mainly has the characteristics of no pollution, short process and interdisciplinary.

The following technologies have been industrialized: vacuum metallurgy; microwave metallurgy; biological metallurgy, short process technology including high pressure leaching technology; direct reduction technology; enhanced metallurgical technology.

New materials are the foundation of new civilization, and the revolution of materials brings about the progress and development of human civilization. As mankind enters the post-modern society from the modern society, materials will enter the material age and even the intelligent material era from the metal age.

The typical characteristics of new materials are: Designable, platform, customized and personalized.

New business model of non-ferrous metals

It mainly includes: 1. Transnational industrial chain integration: overseas processing-import-domestic processing-export

As the international trade of waste and mineral resources is under the dual pressure of environmental protection and trade protection, the localization of resources has become inevitable. The logic of the business model of transnational industrial chain integration is: transnational investment in the processing of primary raw materials, primary raw materials are imported into China for material processing, and even materials are processed locally, exported to China for local processing and supply to the local market or to the international market.

2. Industrial Internet

Industrial Internet is an industrial e-commerce platform and a platform for the integration of technology providers, suppliers, logistics and consumers. The Internet of non-ferrous metals industry can take the transformation of non-ferrous metals industry as an opportunity to guide the transformation of non-ferrous metals industry. As the non-ferrous metals industry is currently in a fragmented state, minerals, basic metals, rare and precious metals, and metal working metal materials, not to mention new materials are independent systems, information providers, technology providers and product production and consumption are also individual cases, so it is necessary to integrate first of all through the Internet.

Trade opportunities for the restructuring of non-ferrous metals industry chain

1. Metal scrap trade

The situation that the world's metal raw materials mainly rely on minerals has completely changed, and it has become a reality that all metals can be recycled. In the past, the industrial chain was the transfer of metal scrap from developed countries to underdeveloped countries for smelting, and then the raw materials after smelting were returned to developed countries for processing to become new materials for re-use-metal recycling industry.

With the improvement of environmental requirements of underdeveloped countries, the waste trade chain from developed countries to underdeveloped countries has been interrupted, and new technologies and waste processing models are beginning.

2. Metal material trade

The traditional industrial chain is fragmented, and metal minerals, metal smelting and metal materials become independent industrial chains. A new industrial chain is being formed, and the trade of metal materials will be dominant. once the industrial chain from scrap to metal materials is formed, the international trade of basic metals will decrease, the trade of metal materials will increase, and technology will play a leading role in the trade.

The trade model of metal materials will be a customized platform model, rather than the traditional large-scale standardization model.

New Power of Nonferrous Metals-New Enterprises of Green Metallurgy

1. Green Metallurgical Technology + Renewable Resources

Recycled metal resources have become the main resources of the non-ferrous metal industry. Using green metallurgical technology to deal with renewable resources does not produce new pollution, which is a new force for the development of the non-ferrous metal industry.

Renewable resources include green metallurgical technology and equipment industry; centralized treatment and regeneration of solid waste; recovery and regeneration of industrial waste.

2. Short flow technology + complex ore development

The short process technology and new material technology in green metallurgy are combined to deal with complex ores. It mainly includes the full recovery enterprise of complex mine, the tailings treatment enterprise of single mine, and the regeneration and ecological restoration enterprise of abandoned mine.

New Power of Nonferrous Metals-New material Model

Horizontal integration development strategy

Horizontal integration basically has no successful cases in international multinational enterprises, but it is basically the leading strategy of large resource-based state-owned enterprises.

The investment trap of horizontal integration: the industry barrier is relatively high; the industry span is relatively large; the structural competition strategy of the industry is difficult to choose.

It is suitable for financial investors to make industry integrated portfolio investment.

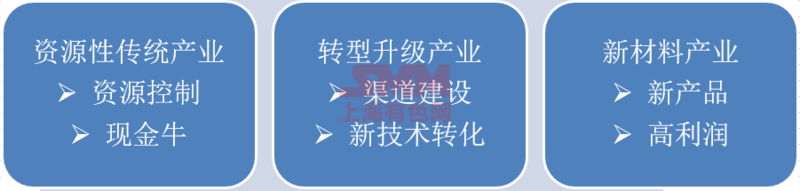

Development strategy of transforming industry

Transformation industry refers to the development strategy of using new technology to help traditional industries upgrade. It mainly includes the following aspects:

1. Environmental protection industry

2. Renewable resources industry

3. New technologies in the industry: 1 vacuum metallurgy technology 2 bio-metallurgy technology 3 short process technology

Development strategy of resource-based traditional industries

Mining industry: the mineral resources of large major metals have been carved up.

Major development opportunities:

Treatment technology of polymetallic complex mineral resources: tantalum-niobium-tungsten-tin-gold rare earth ore

Comprehensive recovery technology of main metal ore: recovery of iron and rare and precious metals from bauxite

Short process and New material Technology of Mineral Resources: direct reduction of Sponge Iron Powder of Iron Ore

Development Strategy of New Metal-based Materials

There are many opportunities for the development of new metal-based materials, which can be divided into four categories:

The technology is mature and the market is growing.

(2) the technology is in the pilot period, and the market is in the introduction period or replacement period.

(3) the technology is in the small trial period, and the market is in the R & D period.

(4) the technology is in the concept period and the market is in the concept period.

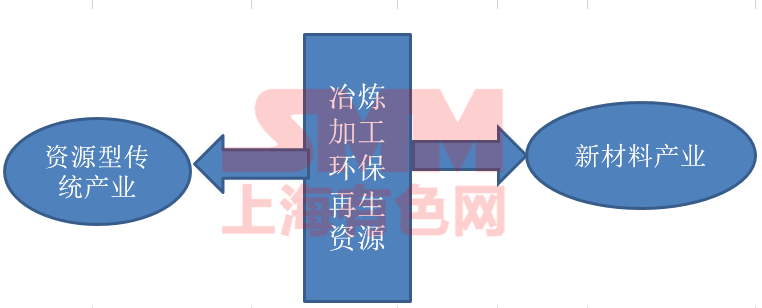

Two-way integration development strategy: starting from the intermediate industry of the industrial chain, extending to both ends of the industrial chain.

Two-way integration is a more rational strategic choice for many investors. Successful enterprises at home and abroad can be found everywhere. For example, Huayou Cobalt Industry: starting from the recovery of cobalt and nickel, entering ternary cathode materials on the one hand and acquiring cobalt ore resources in Africa on the other; a foreign company: starting from the recovery of silver catalyst. On the one hand, it enters the conductive silver paste industry, and on the other hand, it enters the acquisition of silver mineral resources.

Reverse integration development strategy: it is a new development strategy. Obtain investment through new technology, profit through new materials, and cash flow through resources.

The new technology of green metallurgy will give birth to new world-class enterprises of non-ferrous metals. The main characteristics of these enterprises are platform, customization and personalization. New material technology and market will affect the future non-ferrous metal industry.

Scan the code and apply to join the SMM metal exchange group.