SMM7: at the 2020 China Ni-Cr stainless Steel Industry Market and Application Development Forum held in SMM on July 20, Feng Hang, general manager of Henan Getian Renewable Resources Co., Ltd., gave a speech on the situation and problems of China's scrap market.

Present situation of waste stainless Steel Industry in China

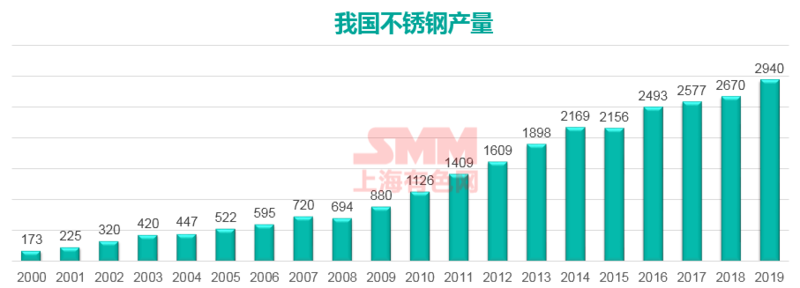

Since the first furnace stainless steel production of Taiyuan Iron and Steel Co., Ltd. in 1952, the output of stainless steel was 88900 tons in 1978. In 1979, China's output exceeded 100000 tons. From 2000 to 2019, the total output of stainless steel in China was 260 million tons.

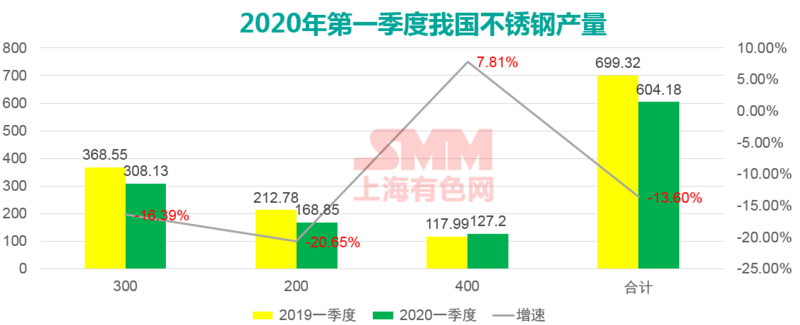

The national output of stainless steel crude steel in the first quarter of 2020 was 6.0799 million tons, a decrease of 604200 tons or 9.04 percent compared with the first quarter of 2019. Of these, the output of 300 series stainless steel decreased by 248000 tons, decreased by 7.45% to 1.6885 million tons, or 439300 tons, and decreased by 20.64%. The output of 400 series stainless steel increased by 92100 tons, or 7.81%, and the output of duplex stainless steel was 38155 tons.

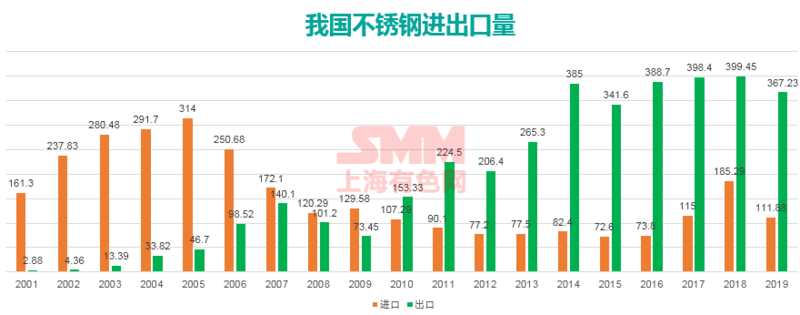

According to customs data, China imported 147000 tons of stainless steel from January to February 2020, down 94000 tons or 39 percent from the same period last year. Exports were 440700 tons, a decrease of-12%. From 2001 to 2019, China imported 29.51 million tons of stainless steel and exported 36.44 million tons.

According to regional analysis, the coastal capacity of South China, mainly Guangxi, Guangdong and Fujian, is about 12 million tons, accounting for 40% of the production capacity, while that of the eastern coastal areas dominated by Jiangsu and Shandong is about 7 million tons, accounting for 25%. The production capacity of the central and western regions is about 9 million tons, accounting for about 30%. In terms of overall distribution, 60% of stainless steel production capacity is concentrated in coastal areas, while the remaining 30% is scattered in the central and western regions.

Sources of scrap stainless steel

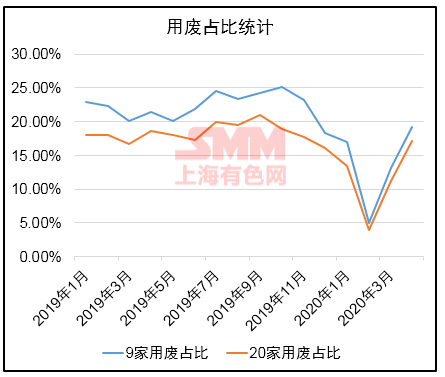

Proportion of scrap stainless steel used

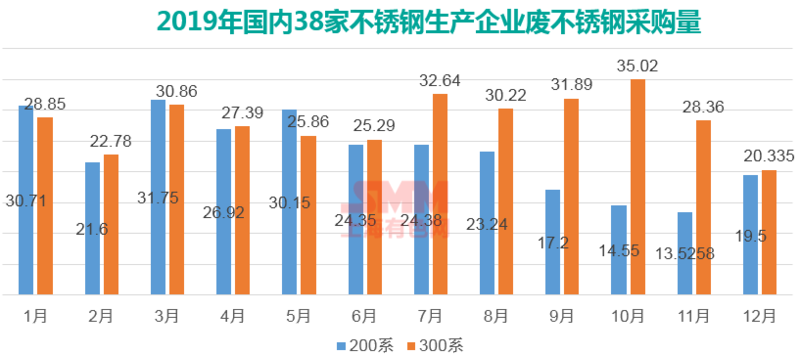

According to statistics, In 2019, there are 38 domestic stainless steel production enterprises (Taigang, Qingtuo, Guangqing, Beihai Chengde, Delong, Lianzhong, Posco, Jiugang, Fuxin, Henan Jinhui Taishan Steel, Luoyuan Baosteel Desheng, Fujian Wuhang, Yunnan Tiangao, Lianyungang Huale, Guangxi Jinhai, Liugang Zhongjin, Yongxing Special Steel, Ningbo ASEAN, Xinfeng, Yongda, Hezhou Pengda, Shenyuan Special Steel, Spark Special Steel, Lianyungang Science and Technology, Shangtai Hunan Taihe, Shandong Shengbang, Yanshan China Resources, Lianqun Sheng, Ningbo Quanxing, Ningbo Wanrong, Huaxin Lihua, Friendship Special Steel) purchased about 6.17 million tons of scrap stainless steel. Of which 2.7787 million tons are 200 series and 3.3949 million tons are 300 series.

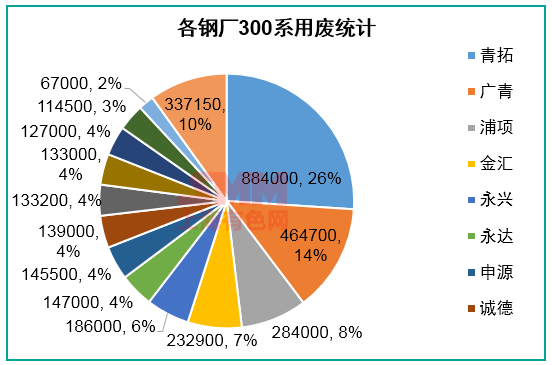

Qingshan (Qingtuo, Guangqing) in 2019, the total procurement of waste stainless steel reached 1.69 million tons, accounting for 27.39% of the overall sample data, of which 1.349 million tons accounted for 39.7%.

Quality deduction:

300 series: the contract is deducted according to the nickel price / chromium price of the day; element requirements: C-carbon ≤ 0.6%, Si- silicon ≤ 0.6%. Phosphorus (single furnace) 0.041 < P ≤ 0.043% fine 50 yuan / ton, 0.043 < P ≤ 0.045% fine 100 yuan / ton, 0.045 < P ≤ 0.050% penalty 150 yuan / ton; P > 0.05% separately. If the carbon / silicon exceeds the standard by 0.1%, the unit price will be deducted 10 yuan / ton; the five harmful metals (lead / tin / arsenic / antimony / bismuth) will be deducted.

200 series: Ni substandard: less than 1.0%, 10 yuan / ton per lower 0.1%; if less than 0.8%, 50 yuan / ton per lower 0.1%; Mn substandard: less than 9.5%, 12 yuan / ton per lower 0.1%; if less than 8.5%, 24 yuan / ton per lower 0.1%; Cr substandard: less than 13.3%, 15 yuan / ton per lower 0.1%; If less than 12.5%, 30 yuan / ton per lower 0.1%; P substandard: 5 yuan / ton for every 0.001% higher than the standard; 10 yuan / ton for every 0.001% increase above 0.06%; In addition, if the Mn is not less than 9.0% and the Cr is not less than 12.8%, and the total content of Mn and Cr is more than 23%, there is no need to withhold penalties for manganese and chromium elements, and other elements that do not meet the standards shall be withheld and punished in accordance with the above-mentioned principles.

Steel mill purchase settlement mode:

Purchasing mode

Order model 1: long-term orders, fixed monthly delivery volume, settlement in accordance with the agreed settlement method (mostly refer to the net price)

Order model 2: short-term orders, non-periodic or periodic release of purchase orders, traders are free to choose to accept orders or not, orders are determined according to the wishes of traders, some will stipulate the minimum quantity of orders.

Free purchase mode: the steel mill sets the current purchase price, and the trader delivers the goods according to the purchase price.

Settlement mode

Hot metal settlement: according to the effluent element composition standard rate for settlement, element deduction.

Cash settlement: mostly 80% of the payment on arrival, and the final payment to the account period varies from 1MUR to 3 months.

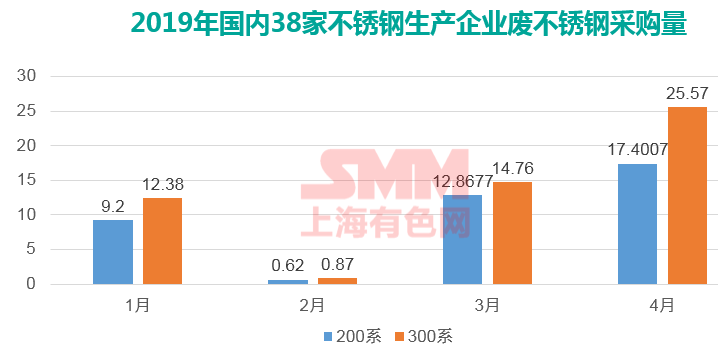

Affected by the epidemic situation in the first four months of 2020, 936000 tons of stainless steel scrap were purchased, down 1.27 million tons from January to April last year, or 58 percent, and the use of scrap stainless steel for the whole year of 2020 is expected to be 6.5 million tons!

Factors affecting the price of waste stainless steel: the cost of electric furnace steelmaking; the price of substitutes for raw materials; the price of stainless steel products

Policy of waste stainless steel industry in China

Scrap steel processing and distribution access:

In order to promote the comprehensive utilization of scrap iron and steel resources, strengthen the management of scrap iron and steel processing industry, standardize the production and operation behavior of scrap iron and steel processing industry, actively promote the connection between supply and demand of scrap iron and steel, improve the management level of intensive processing and the quality of scrap steel processing, strengthen the scale and modernization of scrap iron and steel industry, optimize the allocation of resources, realize the introduction of concentrate into furnace, and promote the scientific, healthy and sustainable development of scrap iron and steel processing industry. By 2020, a total of 399 enterprises in seven batches have obtained the qualification of scrap steel processing and distribution by the Ministry of Industry and Information Technology. The annual scrap processing capacity can reach 110 million tons, accounting for 1% of the social scrap resources.

With the revision of access conditions in 2016, scrap stainless steel and special steel processing enterprises will be brought into management, strengthen flow management, shall not be sold to "strip steel" enterprises, and strengthen the requirements of quality and environmental protection. Enterprises should pass the certification of ISO quality and environmental management system, emphasize the application of information platform, and strengthen supervision after the event.

Fiscal and taxation policy: before 2002, VAT was levied first and then returned; from 2002 to 2008, recycled enterprises were exempted from VAT, and the profit and waste enterprises were deducted 10% from 2009 to 2010, and then 70% from 2011 to 2015.6, the full amount of VAT was levied on 17% VAT; from 2015.7 to now, the VAT of access enterprises that meet the requirements will be refunded by 30%.

Import and export policy:

In July 2017, the implementation Plan for banning the entry of Foreign garbage to promote the Reform of solid waste Import Management system proposed to "classify and adjust the management catalogue of imported solid waste in batches" and "gradually and orderly reduce the type and quantity of solid waste import".

In April 2018, the catalogue was adjusted, scrap hardware, scrap ship and scrap automobile pressing parts were banned from import, which will be implemented from December 31, while scrap stainless steel will be banned from import at the end of 2019.

In December 2018, the Ministry of Ecology and Environment, the Ministry of Commerce, the National Development and Reform Commission and the General Administration of Customs jointly issued a notice on the adjustment of imported waste management catalogue (2018 No. 68) the transfer of scrap steel from non-restricted category to restricted category, which will be implemented on July 1, 2019. At the same time, the relevant departments are studying and formulating quality standards for recovered copper and aluminum raw materials, and the recovered copper and aluminum raw materials products that meet the relevant product quality standards of the state are not solid wastes and can be managed as ordinary and free imported goods.

The problem trend of waste stainless Steel in China

Policy issues: high policy threshold; lack of unity; low proportion of subsidies; policy benefits are difficult.

Tax problems: renewable resources recovery enterprises are difficult to obtain value-added tax deduction, resulting in their tax burden is too heavy; the tax preference of renewable resources processing link is not strong, difficult to implement, and the number of enterprises that can enjoy preferential treatment is limited; the tax preference of renewable resources processing link is difficult to transmit to the formal enterprises in the recovery link, which leads to "bad enterprises expel good enterprises"; The unreasonable design of tax policy leads to the high cost of recycling of renewable resources, which aggravates the consumption of primary resources and the problem of enterprise income tax.

Standardization problems: quality standardization; penalty standardization; product standardization.

Trade problems: unstable contract; asymmetric payment; long settlement cycle; high financial pressure.

Development trend:

1. The degree of standardization of the industry has been further strengthened.

2. Rapid increase in industrial concentration

3. Accelerate the integration of the upstream and downstream of the industrial chain

4. The development trend of standardization is obvious.

5. Development trend of short process steelmaking

Scan the QR code, apply for participation or join the SMM metal exchange group