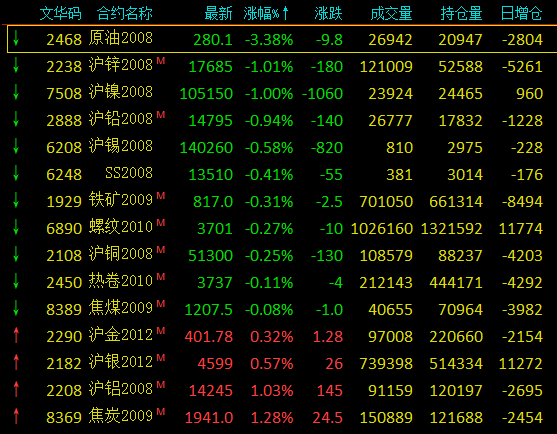

SMM7 March 20: today's non-ferrous metals market generally fell. By the end of the day, Shanghai nickel fell 1.13%, Shanghai zinc fell 1.01%, Shanghai lead fell 0.94%, Shanghai tin fell 0.79%, Shanghai copper fell 0.25%, Shanghai aluminum alone rose 1.03%. In terms of lead, since May 8, the social inventory of lead ingots has opened the accumulation model. As of July 17, the total inventory of SMM lead ingots in five places has reached 47700 tons. Up 29900 tons from May 8. Lead prices have erased a wave of gains since July 7 under the pressure of a receding stock boom and rising stocks of lead ingots. SMM believes that at present, due to the decline in lead prices, and waste battery prices remain high, recycled lead smelters maintain a capital preservation state, recycled refined lead stickers have shrunk, refineries show cherished sales sentiment, some just need to return to the primary lead, but the primary lead enterprises are overhauled and returned to normal production, and downstream consumption is afraid of falling cautiously, it is expected that the social inventory of lead ingots will continue to rise this week.

[SMM Analysis] inventory increases sharply, lead prices fluctuate, supply loosens and consumption drags down inventories will still increase.

In terms of black, thread fell 0.27%, hot coil fell 0.11%, stainless steel fell 0.19%, coke rose 1.28%, coking coal fell 0.08%, iron ore fell 0.31%. The inventory of 35 ports tracked by SMM for the current period totaled 102.9 million tons, an increase of 1.48 million tons from the previous month and a decrease of 4.2 million tons compared with the same period last year. In this period, the increase in the inventory of imported mineral ports expanded, and the month-on-month growth of Shandong and Tangshan main ports showed an increasing trend. At the same time, the average daily dredging volume of the port fell by 55000 tons to 2.811 million tons compared with the previous month. Most steel mills continue the on-demand procurement strategy, leaving Hong Kong for a short-term or difficult to see a substantial increase. Although the last period of SMM statistics of iron ore arrival decreased slightly compared with the previous period, there is still a pressure on the port in some ports, and the inventory of imported ore ports is still expected to continue to increase in the later period. SMM believes that short-term iron ore in the case of absolutely low inventory, prices are also high during the year, while the current long-process steel mill operating rate remains high, strong demand, the market has no obvious incentive to take the initiative to reduce production. It is predicted that after the current high falls in the short term, if there is no other external news stimulation, the imported mining market will fluctuate mainly this week or at a high level.

[SMM Analysis] Port inventory continues to increase and change the high price pattern of iron ore

Crude oil fell 3.01% in the previous period, and the biggest threat to the oil market is still the risk of a second spread of the epidemic, which may have an impact on crude oil demand as more states in the United States are forced to restart the blockade because of the rebound in the epidemic. At the same time, as OPEC+ cuts production by 2 million b / d from August, it has also added to the market's misgivings, with news that Russia will increase production by 400000 b / d. In addition, with the second spread of the epidemic, gasoline, which is at the peak of summer demand, has declined for two weeks in a row, highlighting weak demand. With the recent recovery in refinery operation rate, insufficient gasoline demand may cause refineries to reduce production again, thereby reducing demand for crude oil.

As of today's day close:

Today's capital flow

< updating >

A brief comment on SMM analysts on July 20th

Copper: today, the main force of Shanghai copper opened at 51390 yuan / ton in the morning. After opening, the copper price quickly fell to 51210 yuan / ton, rebounded slightly and fell again, with a daily low of 51120 yuan / ton. After that, with the bulls increasing positions one after another, copper prices fluctuated upward, the center of gravity rose to 51300 yuan / position, and closed at 51310 yuan / ton at noon. In the afternoon, bulls entered the market to drive up copper prices to the highest point of the day, 51450 yuan / ton, but long days continued to promote limited energy, the market declined slowly, near the end of the day, bulls reduced their holdings and left the market. Copper prices finally closed at 51270 yuan / ton, down 120 yuan / ton, down 0.23%. During the day, 09 contracts reduced positions by 294 to 112000, mainly by long positions, while trading volume decreased by 29000 to 87000. 08 the contract day reduced positions by 4203 to 88000, mainly by long positions, while trading volume decreased by 31000 to 109000. The central bank's one-year lending rate announced today remains unchanged at 3.85%, the tone of monetary policy easing remains unchanged, and investors remain cautiously optimistic. However, market worries about the continuing grim state of the new crown epidemic plaguing the economic recovery still exist. At present, the global new crown confirmed cases have broken through the 14 million mark, while the epidemic has not yet ended and tensions between China and the United States continue to ferment. Market expectations for the prospects of economic recovery have been suppressed, putting pressure on copper prices. Today, Shanghai copper negative, KDJ opening continues to expand, the upper pressure 5-day moving average, waiting for the outer disk guidelines at night, test whether the bulls can defend the 10-day moving average.

Aluminum:

Lead: within a day, the 2009 contract for Shanghai lead is opened at 14740 yuan / ton. In early trading, Shanghai lead was entrusted with 14685 yuan / ton, and the daily moving average fluctuated horizontally under pressure. In the afternoon, basic metals rose generally, and Shanghai lead was also boosted. It broke through the intraday moving average on the 20-day moving average, gave up some of the gains after reaching the intraday high of 14835 yuan / ton, fluctuated along the horizontal market of 14785 yuan / ton above the daily moving average, and finally closed at 14775 yuan / ton, down 120 yuan / ton, or 0.81%. The position increased by 1556 to 19085, and the trading volume increased by 5647 to 17093. The main contract changed to 09 contract, the transaction is active, mainly for long positions. Shanghai lead newspaper closed down, supported by the 20-day moving average, but is still trapped in the gap during the Spring Festival this year, the KDJ index is still open downward, the 5-day moving average shows a trend of below the 10-day moving average, and the technical indicators have not yet shown signs of turning more. At the same time, as of last Friday, lead inventories in the previous five places had increased by more than 10,000 tons to more than 40,000 tons compared with the previous period, while the downstream trading was light and the fundamentals were weak, so it was necessary to pay attention to whether the bulls could maintain the 20-day moving average at night. It is expected that in the short term, the lead in Shanghai will still be adjusted at a low level.

Zinc:

Nickel:

Tin:

< updating >

"Click to sign up: 2020 Tin Industry chain Trading Summit

![The Most-Traded BC Copper Contract Closed Down 1.16%, Inflation Concerns Suppressed Expectations for Interest Rate Cuts [SMM BC Copper Commentary]](https://imgqn.smm.cn/usercenter/JnFuh20251217171711.jpg)