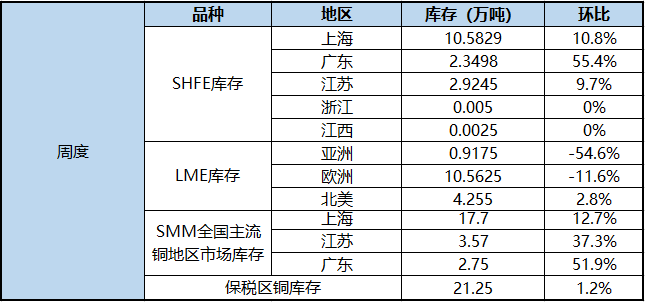

Copper:

The domestic money supply is adequate, liquidity continues to be loose, domestic economic expectations are improving, and the two major sectors of infrastructure and real estate continue to underpin the Chinese economy, bringing optimistic expectations of domestic copper consumption to the market. On the fundamental side, concerns about the supply of copper raw materials caused by the outbreak in South America have not dissipated and will continue to be positive for copper prices. Unwrought copper and copper materials announced this week totaled 656000 tons in June, an increase of about 25 percent over the same period last year, and imports of electrolytic copper are expected to reach more than 400000 tons in June. On the one hand, the sharp increase in copper imports was due to the concentration in Hong Kong after the resumption of overseas logistics in June, on the other hand, it confirmed that domestic consumption was strong in the second quarter and the supply and demand structure was healthy, attracting imported copper into the Chinese market. Recently, import parity has opened slightly, although there is a reduction in supply, it also proves that domestic demand is still stable and good, and downstream buying has improved significantly after copper prices fell this week. Due to the long-term positive support of copper fundamentals, copper prices will stabilize and rebound after financial market sentiment stabilizes. This week, Shanghai Copper is expected to run at 51000 won 52500 yuan per ton, while Lun Copper will run at 6350 won 6550 US dollars per ton.

Aluminum:

This week, the situation of electrolytic aluminum slowly de-stocking continued. According to SMM statistics, the weekly inventory of electrolytic aluminum in China decreased slightly by 4000 tons to 708000 tons. In terms of aluminum bars, the stock of aluminum bars has been reduced by 7200 tons to 65000 tons compared with last Thursday. Inventory in Foshan, Wuxi and Nanchang declined, inventory in Changzhou increased slightly, and inventory in Huzhou remained flat.

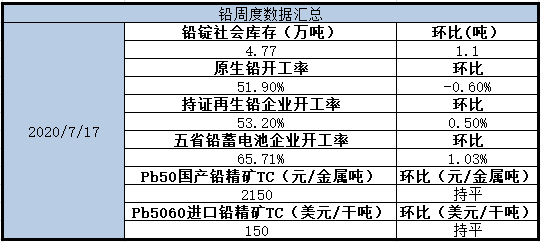

Lead:

With the end of this delivery, the domestic social inventory of lead ingots has returned to more than 40,000 tons, from the correlation between inventory and prices previously measured by SMM, lead is the relative fundamental pricing variety, we believe that this round of rise depends on the macro environment and funds, follow-up attention to the operation of funds after the selection of futures to receive goods, as well as changes in the overall macro environment, and another concern about the pace of recovery of domestic lead battery consumption after the flood season.

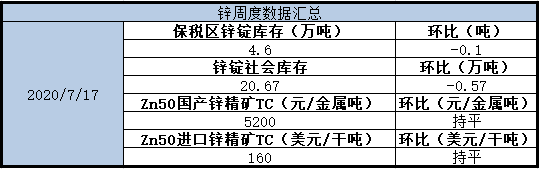

Zinc:

As far as Shanghai zinc is concerned, it has fallen after the general rise of non-ferrous metals this week, the positive mood in the market has dissipated, and Shanghai zinc has returned to the fundamentals. As far as next week is concerned, the supply side of the market is still under pressure from the increment of domestic zinc ingots. From next week, due to the enterprise target requirements, Shaanxi zinc industry and Hanzhong zinc industry two smelters will try their best to achieve full capacity production to meet the target. At the same time, domestic processing fees have stopped falling and rebounded, greatly boosting the production willingness of smelters, superimposed on the completion of maintenance of most smelters in the first half of the year, and it is expected that the follow-up supply may still increase month-on-month. On the import side, due to the less optimistic import price ratio and the slow appreciation of the superimposed RMB, it is expected that the import window will still be difficult to open in the short term. In addition to a small number of long single imported zinc inflows, it is expected that the amount of imported zinc will be limited next week. On the consumer side, due to the large increase in zinc prices since last week, until this week, downstream enterprises are still mainly wait-and-see, not just need to buy, mostly to consume the current inventory of raw materials and finished products, it is expected that there will be more purchases and replenishment next week. From a technical point of view, Shanghai zinc fell back to the upper track of Brin Road this week, and the KDJ index showed parallel, indicating that the movement of Shanghai zinc can be limited. Next week, Shanghai zinc is expected to maintain a range of finishing, supporting in the 10-day moving average operation. Overall, next week, Lun Zinc is expected to run at 2170 won 2240 US dollars / ton; Shanghai Zinc 2009 contract material is expected to run at 17500 Mel 18200 yuan / ton, the spot side is expected to rise water in August around 100 Mel 150 yuan / ton.

Nickel:

The recent market is greatly affected by the capital side, although there has been a sharp correction in metal prices affected by the stock market on Thursday, but it has still maintained more gains since last week, and metal prices are still in a strong state under financial stimulus. Due to the lack of positive fundamentals, the room for nickel to continue to rise is limited, and heavy rains in Sulawesi, Indonesia, do not seem to have a significant impact on smelters at present, but the recent bull market with financial stimulus also needs to be cautiously bearish. It is expected that the high price of nickel will fluctuate next week, with 108000 yuan / ton in Shanghai nickel and 13150mi US $13700 / ton in Lunni. In terms of social inventory, the inventory of the previous period this week increased by 2348 tons to 31843 tons, some new imports and spot warehouse sources were shipped to the delivery warehouse, and the number of warehouse receipts increased significantly. Hidden inventory in East China increased by 197t to 13005 t. Some electrolytic nickel was stored in Shanghai by smelters in Gansu and Jilin this week. After offsetting the difference, hidden inventory in East China this week increased slightly by 197t compared with last week. Guangdong Southern Reserve inventory increased to 290 tons. As for the Shanghai Free Trade Zone, it increased by 800 tons of nickel plates, and the inventory of pure nickel increased to 17300 tons.

Tin:

This week, the Shanghai tin 2009 contract rose sharply under the influence of the stock market at the beginning of the week, following the annual tin price of 144570 yuan / ton last week. Subsequently, Sino-US trade problems had an impact on domestic investment sentiment, coupled with profit-taking in the stock market, the CSI 300 index fell 336.7 points in a row in 3 days, a cumulative decline of 6.9%, and the metal almost turned green. In the general environment, it is difficult to support tin trees in Shanghai, and it has been overcast for three days. However, the disk and fundamentals have a certain support, three days have not yet fallen below the one-day increase at the beginning of the week. Friday night market high jump, and then first rise and then suppress, the center of gravity moved up. The center of gravity of the day was lower than that of the night, but it was still higher than the opening price of the night. It closed at 141200 yuan / ton, up 1280 yuan / ton, or 0.91%. The turnover was 45045 lots, and the position was 28635 lots, a decrease of 1090 lots. This week Lun Xicheng Xiaoyang line, the physical part of the lower part received a 5-day moving average support. Although there is a downward atmosphere in the entire metal market, since July, the imported tin ore volume has decreased again, the refined tin import window has been closed, the tin supply end has decreased again, and the superimposed Yunnan collection and storage policy has landed, which is expected to provide some support to tin prices. The upper pressure level is expected to be around 144500 yuan / ton.

The price of tin spot goods in Shanghai this week rose sharply following the stock market at the beginning of the week. Subsequently, the market went down, and spot prices also fell. On the whole, the spot price is in a high position, the willingness of manufacturers to sell goods is low, and the willingness of traders to receive goods is not very strong due to their own inventory and downstream demand. However, the sharp rise and fall in futures did provide a profit opportunity for traders, and some traders received a small amount of goods and shipped quickly. Friday trading pullback, there is a cloud word for the delivery of smooth discount quotation, but the duration is not long. As for the discount for Shanghai tin 2009 contract, compared with last weekend, there is no big change in Nei Yun tin premium, it is still around 750yuan / ton, some cloud words have changed from flat to small discount, and the small brand discount has been enlarged. Friday's discount is about 1750 yuan / ton.

Scan the QR code, apply for participation or join the SMM metal exchange group

![Sharp Decline in Copper Prices Prompted Some Downstream Enterprises to Operate at Full Capacity, and Spot Copper Turned to Premiums Across the Board [SMM South China Copper Cathode Spot Weekly Review]](https://imgqn.smm.cn/usercenter/IHqPw20251217171709.jpg)