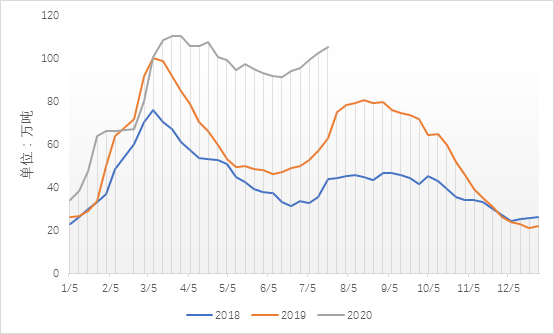

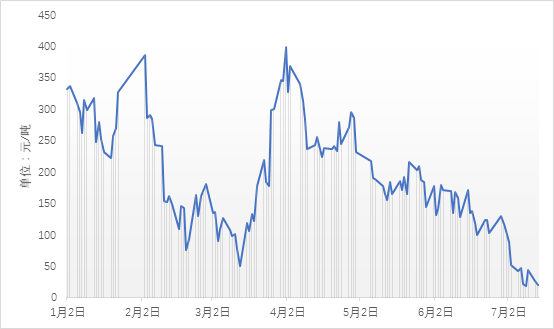

本周杭州螺纹库存108.5万吨,环比+1.9万吨,同比+43.9万吨。本周杭州延续累库,库存增幅环比上周扩大,当前杭州库存量已逼近年初峰值,更是在挑战杭州建材库容极限。近期,杭州螺纹库存高企引发了市场不少贸易商及终端的担忧,更是抑制杭州建材市场价格反弹的主因之一。

图一:杭州螺纹库存走势

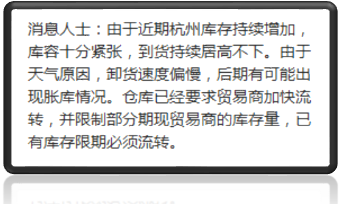

最近你可能看到这样的消息…

图二:市场传闻

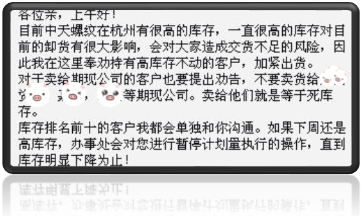

作为全国最大的建材贸易集散中心,杭州是如何成为全国库存压力最大的价格洼地的呢?据SMM了解,当前杭州库存中分别大约有:中天40万+,沙钢20W+,西城15W+,以及其他例如永钢、丹阳、桂鑫、丹阳、富鑫、桂鑫、缤鑫、亚新、彭钢、旋力、中新、鸿泰等几十家品牌资源,共同积累凝聚了高达近110万吨的“钢铁巨鳄”。

图三:杭州库存缩影

实际上,据SMM了解,近110万吨库存中,有一半左右的库存是期现公司用于期限套利操作的“僵尸库存”,想必你也看到过钢厂的“歇斯底里”…

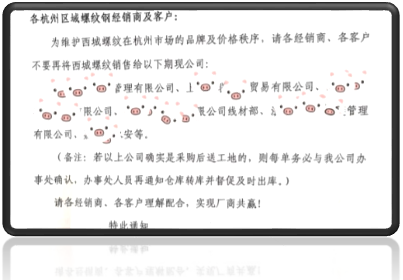

图四:市场传闻

图五:市场传闻

华东尤其是杭州市场,由于建材集散量大,且金融属性较强,螺纹价格和期货盘面相关性极强,孕育了大批期现公司在此“搅弄风云”,今年5月中旬以来,由于期螺盘面上涨快于杭州现货价格,致使基差不断收窄,且距离螺纹10合约的交割期还有较长时间,期现公司迎来了绝佳的“正套”套利机会。大批量以中天为主的螺纹资源被期现公司“套”入库中。然而至今为止,螺纹基差迟迟没有重新扩大,反而一再收窄,仅给期现公司继续开仓套利的机会,却未能给出盈利平仓的机会,致使“僵尸库存”不断提升,据SMM向部分期现公司及贸易商了解,当前杭州螺纹库存中大约有60万吨左右的属于期现公司,由于未能有盈利平仓的机会,这些库存仅少量轮库以防生锈,并未大量投向市场。

图六:2020年杭州建材基差走势

注:基差计算使用沙钢厂提过磅价格对比螺纹主力合约

So the question is, when will such a large amount of "zombie inventory" be put on the market? Will it bring pressure on the market price? First of all, the current thread basis situation in Hangzhou is not conducive to the closing and selling of cash companies, but because the basis has been narrowed again and again, the price raised by Shagang Plant is close to the level of thread 2010 contract, and the current basis situation has lower cost and more space than the previous period, so the cash company is more likely to receive goods in the spot market, and as far as SMM knows, the company is gradually collecting goods and building positions in Hangzhou market. There is a certain support for the short-term Hangzhou thread price. Secondly, from a cost point of view, the positive set of profits must reach at least 50 RMB60 / ton, the current company will have the possibility of selling spot positions, if the basis gradually widens, the market profit space appears, then the "zombie inventory" will gradually be put into the market, and under the premise of making a profit, the possibility of selling at a low price is also greater, at that time, there is a high probability that the price of Hangzhou thread will be suppressed. Of course, the high inventory is not the result of a "period". At present, the amount of resources in cities around Hangzhou and resources in Shayongzhong are relatively large in Hangzhou. At the same time, affected by factors such as the rainy season, the terminal demand in East China is relatively general. The difficulty of inventory digestion is also an important reason for the high inventory in Hangzhou market. Although it is more difficult to make a debut than to make a debut this year, the release of "zombie inventory" may cause a temporary crackdown on the spot market price in Hangzhou. However, looking at the transaction situation of building materials across the country, the northern market is not affected by the rainy season, and the demand continues to maintain a high degree of prosperity. On the other hand, the interference of the rainy season in southern China, such as Guangdong, has obviously decreased after late June, and the market transaction situation has also improved obviously. is there any reason for us not to be confident about the explosive demand after the end of the rainy season in Hangzhou? At the same time, considering the high probability of a slight decline in the current thread output, it is expected that the price of building materials in Hangzhou market will remain volatile from July to August. (note: the relevant inventory resources in Hangzhou and the inventory of the cash company all come from the estimation and integration of the market traders and the cash company, for reference only.)