SMM7 March 15: at the "China Tungsten Industry Market and Application Summit Forum and China cemented Carbide Market Application Symposium" held by SMM, Yang Xuanzeng, general manager of Shandong cemented Carbide Co., Ltd. sorted out in detail the cemented carbide industry chain, cemented carbide industry competition, the five levels and unknowns of the tungsten market.

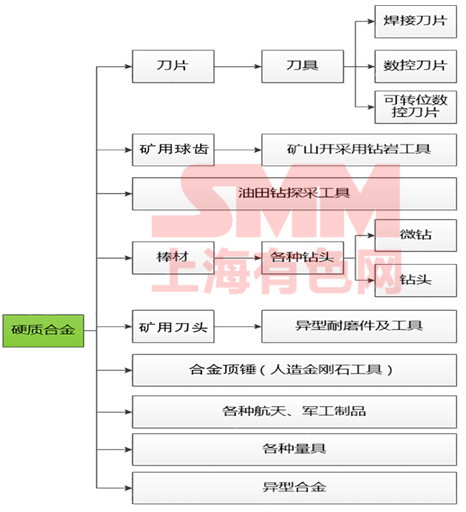

Cemented carbide industry chain

For the convenience of description, the related industries of the upstream and downstream of the cemented carbide industry chain are summarized in the tungsten market. As we all know, the cemented carbide industry consumes about 60% of tungsten resources. Tungsten is also the most non-ferrous metal with Chinese characteristics.

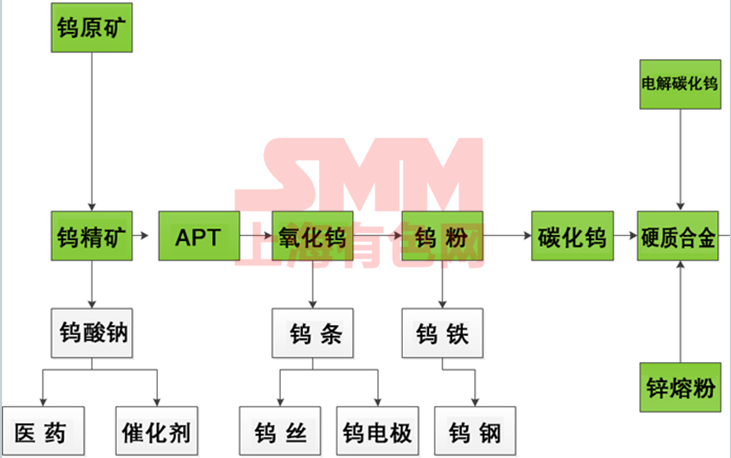

From the perspective of industrial value chain, cemented carbide industry chain covers upstream tungsten mining and gravity water separation tungsten concentrate. Smelting in the middle reaches of the powder plant, crystallization APT, calcined tungsten oxide, reduction of tungsten powder, high temperature tungsten carbide. Downstream cemented carbide plants use powder metallurgy to produce tungsten carbide-cobalt cemented carbide or other cemented carbide superhard materials containing tungsten carbide.

Tungsten resources are owned by the government, and the mining rights, management rights, environmental protection, total mining volume and export quotas of tungsten deposits are also strictly controlled and controlled by governments at all levels, so the upstream market of tungsten market is relatively closed, restricted and protected by relevant national policies. Even so, overmining is still very common.

Tungsten is produced in China and supplied all over the world. Downstream cemented carbide enterprises consume about 60% of tungsten resources. The mid-stream powder processing manufacturers and downstream cemented carbide manufacturers are open markets. If China's tungsten market is compared to a mahjong field, and the upstream enterprises have a lot of chips, then the cemented carbide players downstream are like playing mahjong, which are fair and open, and can be played if they want, only the difference between the size of the chips and the method of game. full of competition and unknown. The competition among cemented carbide enterprises is the competition of talent, technology, capital, product quality and service.

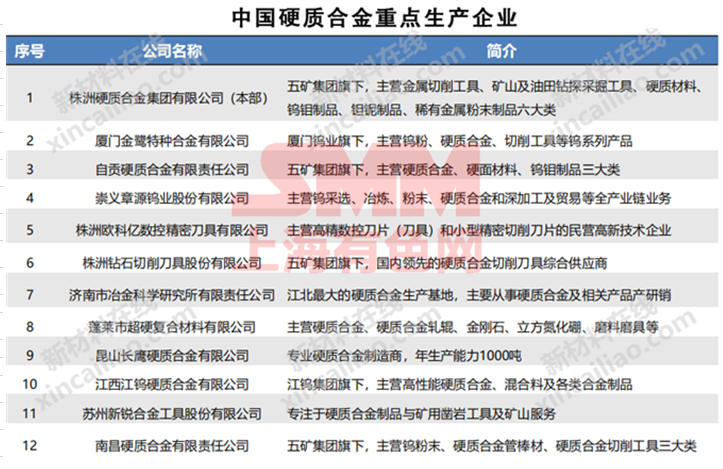

The four listed tungsten enterprises Xiamen tungsten industry, medium tungsten high-tech, Zhangyuan tungsten industry and Xianglu tungsten industry all have the advantages of complete cemented carbide industry chain, and they are all big players of "mining at home".

Analysis of key raw materials

The cost of cemented carbide raw materials accounts for about 85%, of which tungsten raw materials account for about 75%, and metal cobalt powder accounts for about 10%. Therefore, cemented carbide factories pay close attention to the price of tungsten raw materials upstream and are very sensitive to the price fluctuation of tungsten raw materials.

Rich tungsten resources provide an important resource guarantee for the development of cemented carbide industry in China. In 2018, the global tungsten reserves are 3.3 million tons, and China's reserves are 1.9 million tons, accounting for 58 percent of the world's total tungsten reserves.

Apart from China, tungsten resources are relatively scattered, and Russia, which has the second largest tungsten reserves in the world, also accounts for only 7% of the world's reserves.

In addition, we have to mention the waste tungsten market, which is a general term for waste cemented carbide or tungsten scrap. Qinghe in Hebei and Anhua in Hunan, Linqu in Shandong and Jingmen in Hubei are the four major recycling and processing bases of waste cemented carbide in China. The efficient recovery and recycling of waste tungsten is not only the inevitable way to save tungsten resources, but also the only way to reproduce the value of tungsten.

The recycled and recycled tungsten resources have continuously injected new chips into the cemented carbide market.

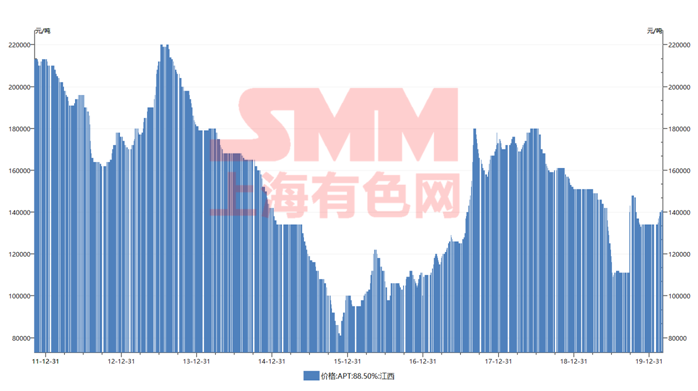

APT Market Price of Tungsten Raw material APT2011- in the Upper reaches of cemented Carbide in 2019

Competition Analysis of cemented Carbide Industry

Using Porter's five forces model, in the analysis of the competitive environment of the cemented carbide industry, we can see that some enterprises are both buyers and sellers, may be potential newcomers in the subdivided market, and the competition among cemented carbide industry chain-related enterprises is more fierce.

Competition among existing enterprises (peer competition)

With the continuous improvement of the product quality of new enterprises, domestic traditional cemented carbide enterprises encounter increasingly fierce competition. Leading enterprises have the advantages of industrial chain through integration, fierce competition in the middle and low-end market, many small-scale enterprises, unreasonable industrial structure and product structure, backward technology and production equipment, and other problems, cemented carbide enterprises as a whole are facing transformation and upgrading.

Potential entrant analysis

While bringing new production capacity and new resources to the industry, new entrants will hope to win a place in the market that has been carved up by existing enterprises, which may compete for raw materials and market share with existing enterprises. it will eventually lead to a reduction in the profitability of existing enterprises in the industry, and in serious cases may endanger the survival of these enterprises.

With the development of China's economy, the demand for high-end products in the domestic market is increasingly exuberant, and domestic enterprises are still unable to meet the needs of customers for high-end products. Foreign cemented carbide enterprises accelerate the pace of entering the Chinese market, rely on technology and brand advantages to further consolidate their monopoly position in the high-end market, block the path of domestic enterprises to high-end products, and wait for aircraft to extend to middle-and low-end products, squeezing out the market share of domestic enterprises. At the same time, the competition for talents will be launched with domestic enterprises, and the phenomenon of excellent brain drain in domestic enterprises will be intensified.

Substitute threat analysis

Two enterprises in different industries may compete with each other because the products they produce are substitutes for each other. this competition derived from substitutes will affect the competitive strategies of existing enterprises in the industry in various forms.

With the progress of science and technology, a variety of high-performance materials have been developed, and some materials have partially replaced cemented carbide products. For example, the development and utilization of diamond PDC drilling tools (tools) will have a profound impact on the fields of oil field drilling and coalfield mining. Ceramic blades, especially CNC blades (including bars) made of lightweight cermets, will have a far-reaching impact on the future product development and structural adjustment of the cemented carbide industry.

Seller's bargaining power

With the deterioration of the export situation and the reduction of domestic terminal demand, the upstream tungsten resources are temporarily surplus. In particular, the progress of recycling technology of waste cemented carbide has greatly weakened the bargaining power of the seller against the buyer. With the help of the integration advantage of capital market funds, the downstream industrial chain enterprises have promoted the concentration of cemented carbide industry to leading enterprises. The upstream raw material market is scattered and there is no cohesion, which makes the bargaining power of the supplier become weak.

Buyer's bargaining power

As more competitors intervene in the cemented carbide industry, the supply of cemented carbide products increases, and there is overcapacity in many products, and buyers (downstream end customers using cemented carbide) can make a variety of choices. it increases the possibility of bargaining, which brings new threats and challenges to enterprises.

Five levels of tungsten market

The division of five levels of tungsten market

According to the annual output of cemented carbide enterprises (in tons), large, medium and small cemented carbide enterprises are divided into five levels.

Top 12 cemented carbide enterprises with an annual output of more than 800 tons.

Class B, with an annual output of 300 to 800 tons

Class C, with an annual output of 120 to 300 tons

Class D, with an annual output of 50 to 120 tons

Class E, with an annual output of less than 50 tons.

The unknowability of tungsten market

The interests of enterprises in most industries are closely related to each other. From the regional and regional performance of national competition, from the product structure, large factories face the competition of small factories. The overall profit level of the industry has declined. The competition of domestic cemented carbide enterprises is mainly concentrated in the middle and low-end market. as the industry as a whole enters a new period of structural adjustment, it will be one of the future development directions of the industry to promote the transformation of cemented carbide industry to resource-intensive development by increasing industrial concentration and improving the efficiency of tungsten resources development and utilization.

With the intensification of competition, the pace of integration of forward integration and backward integration of large enterprises is accelerated.

Any enterprise that cannot keep up with technological progress will face the risk of being eliminated.

Socialized division of labor is the inevitable result of social development, competition is not you but I live. Competition is to outperform the needs of customers, is to find their own unique channel.

As the industry competition has great uncertainty, it is meaningless to predict the outcome of the competition. We must be in awe of the market and respect the market. The development of the market is often independent of people's will.

Scan the code to apply to join the SMM industry communication group: